Nvidia News

-

Selling the less efficient, less powerful versions. China won't be stopped just slowed down so the US may as well profit from it. Profit = more money for innovation and taxes too

On the numbers, it looks, broadly speaking like we are now on a 60/70/80/90/100 rhythm . The margins are exceptional and in the future, software will continue to play a big part so I don't see margins falling any time soon. Not in a meaningful way.

AMDs PE is 35% higher than Nvidia on a Fwd basis and 100% higher on a trailing basis. AMD margins are 32% lower. AMDs problem is no Cuda and inability to scale out inside a data centre nor can they scale across data centres. Even based on what analysts think Nvidia EPS(earnings) growth over the next several years is 50% MORE than AMD. So whilst you could make a case for AMD as an investment with a PEG of approx 1.4 which is not expensive but at the same time not attractive, Nvidia has a PEG of about 0.7.

-

This is in regards to Blackwell chips

-

Jensen tells Su 'Hold my Beer'

AMD has been strategically designing its Instinct accelerators to close the gap with NVIDIA’s AI dominance, aiming to meet or exceed NVIDIA’s anticipated roadmap.

With the MI300X/MI325X, AMD leveraged chiplet-based designs on TSMC’s 5nm/6nm nodes, offering competitive FP8 performance for AI training and inference. The upcoming MI450 (Helios, Q4 2026), built on TSMC 3nm with CDNA 4, was positioned to challenge NVIDIA’s expected Rubin architecture by targeting up to 35x MI300X performance (sparse FP8), enhanced Infinity Fabric for better multi-GPU scaling, and superior power efficiency.

AMD’s roadmap, including the MI500 (2027, 256-GPU racks), aimed to scale to 50,000–100,000 GPUs(still below Nvidia's 1 million but it was a competitive effort), capitalising on chiplet cost advantages and TSMC CoWoS supply (with Broadcom) to erode NVIDIA’s 80–90% AI market share.

Reports suggest AMD’s strategy was to match NVIDIA’s 2026–2027 performance while undercutting on price and power, especially for hyperscale training and enterprise inference. (note it's always next year!).

However, NVIDIA’s Rubin CPX, announced on 9 September 2025, throws a spanner in the works. This GPU, optimised for AI inference “prefill” (context-building for million-token models), delivers 30 petaFLOPS of NVFP4 compute with 128GB GDDR7, four NVENC/NVDEC units, and 3x faster attention processing than Blackwell Ultra. Paired with standard Rubin GPUs (HBM4-equipped) in the NVL144 CPX(hybrid) rack (8 exaFLOPS, 144 GPUs), it offers a disaggregated approach that slashes inference costs by up to 4x while boosting TCO efficiency.

NVIDIA’s redesign of Rubin (upping power to 2,300W) directly counters MI450’s expected specs, suggesting NVIDIA anticipated AMD’s move. The CPX’s specialised inference focus disrupts AMD’s unified training/inference strategy, as MI450/MI500 lack a comparable disaggregated design. NVIDIA’s NVLink 5.0 and CUDA ecosystem further enable scaling to 1 million GPUs, far beyond AMD’s current 10,000–20,000 GPU ceiling.

In short, AMD’s chiplet-based roadmap was on track to challenge NVIDIA’s 2026 performance, but Rubin CPX’s inference optimisation and NVIDIA’s scaling prowess put AMD’s plans in tatters, forcing it to accelerate software (ROCm) and interconnect improvements to stay competitive. Both also being considerably inferior.

The take away is, Nvidia is the King, they clearly have many secret weapons to deploy as and when to counter any competitors claimed advancements. And I say claimed, because all AMD have is a slide deck-products they will produce in the future.

Industry experts hail NVIDIA’s Rubin CPX as a breakthrough for AI inference, praising its ability to handle massive context windows with lightning-fast throughput. Analysts call it a major leap for video, code generation and long-sequence tasks, suggesting it could reshape efficiency and unlock new AI capabilities across data-intensive applications.

-

Yang went on to say they don't have enough capacity as visibility of 'orders' is through 2027 'and it's massive'. The company is opening new factories to meet demand.

As noted previously, Nvidia will be limited by CoWoS-L capacity, which is expanding at a rate of approx 250k chips per Q give or take or 8-10 billion(per Q). We believe the inflexion point is here....60/70/80/90/100 quarterly revenues.

-

China tells technology companies to stop buying all nvda ai chipsets

Hmm hopefully a buying opportunity and not a change of trend direction in the stock

Eta -

Looking likely that the buying opportunity was short lived. Algos bought the dipOnwards and upwards Rodney

-

China’s directive is an escalation but not an outright ban on NVIDIA chips. It’s a strategic move in the U.S.-China tech rivalry, with limited immediate impact on NVIDIA’s valuation due to its reduced reliance on China. The “ploy” theory is plausible but secondary to China’s broader goal of domestic chip dominance.

It will be resolved in time and im sure even more powerful chips will continue to be sold into China, legally and otherwise. China will fall further behind without Team Green. Fact.

The valuation of Nvidia has zero China component baked in.

-

Breaking-Nvidia invest $5B into intel and sign deal to co develop chips. Intel up 30%. NVDA up $5 :). the details are coming in.

-

here is the news article:

Interesting-I guess TSM are so constrained this makes perfect sense. It also rescued intel from almost certain misery. It also broadens Nvidia reach, into the PC market-more growth vectors and will have AMD worried for sure

") And I just had a look at AMD and yes, the market is not liking it at all. Down 5%

And I just had a look at AMD and yes, the market is not liking it at all. Down 5%Nvidia (NASDAQ:NVDA) and Intel (NASDAQ:INTC) announced a major deal on Thursday to co-develop PC and data centre chips. Concurrently, Nvidia revealed it would take a $5B stake in Intel.Nvidia shares increased 2.2% in pre-market trading, while Intel’s jumped 32%. If Intel shares open at that level, it would be their highest in over a year.The partnership will utilise Nvidia’s NVLink, merging Nvidia’s artificial intelligence and accelerated computing expertise with Intel’s x86 architecture. Intel will produce Nvidia-custom x86 CPUs for data centres and supply x86 system-on-chips integrated into Nvidia’s RTX GPUs for the PC market.Additionally, Nvidia will invest $5B in Intel’s common stock at $23.28 per share, subject to standard closing conditions and regulatory approvals, the companies stated.

-

Nvidia continues to make moves.

NVDA has invested over $900M in a strategic deal with Enfabrica, a US-based AI hardware startup, securing key staff, including CEO Rochan Sankar, and licensing its cutting-edge networking technology. The transaction, finalised last week, involves cash and stock payments but is not a full acquisition.

Enfabrica’s Accelerated Compute Fabric (ACF) technology connects over 100,000 GPUs, enabling large-scale AI clusters to operate as a single system, reducing GPU idle time by up to 50% and slashing costs.

Nvidia aims to integrate this into its AI infrastructure, enhancing data centre efficiency for training large language models and supporting “AI factories” with partners like Microsoft. This strengthens Nvidia’s dominance in AI networking, giving it a competitive edge by optimising GPU-centric workloads. The deal, echoing Nvidia’s $7B Mellanox acquisition, avoids regulatory hurdles while bolstering its full-stack AI solutions for hyperscalers and enterprises.

-

More on the Intel deal.

Nvidia and Intel have unveiled a partnership to develop custom x86 CPUs for Nvidia’s AI infrastructure platforms, integrating Intel into Nvidia’s ecosystem.

This collaboration merges Nvidia’s AI and accelerated computing expertise with Intel’s CPUs, targeting a USD 50 billion opportunity in data centres and PCs. Nvidia’s GPU chiplets will enhance Intel’s offerings, bringing AI computing closer to users.

While Nvidia dominates AI-accelerated computing and GPUs, custom chip trends and competition are reshaping the semiconductor landscape. Supply chains are evolving dynamically, and the market is expanding and adapting!

This partnership is noteworthy in the context of advancing computing power and AI’s economic impact. Nvidia’s Jensen Huang emphasised, “Together, our companies will build custom Intel x86 CPUs for Nvidia’s AI infrastructure platforms, bringing x86 into Nvidia’s NVLink ecosystem.” Currently it is solely, Arm based.

Both CEOs expressed optimism, focusing on innovation rather than politics or competitors, describing the collaboration as “historic.”The Verge reported that Nvidia and Intel will connect their architectures via Nvidia’s NVLink system, used in data centres to link GPUs. Huang noted, “Intel will build Nvidia-custom x86 CPUs for integration into our AI platforms, offering greater optionality for advancing AI workloads.” And clearly advance NVLink making it even more pervasive! It also heads off any potential expansion of the Asics market (Broadcom). Great move by Huang and Co

This fusion targets the USD 30 billion CPU data centre market, aiming to create rack-scale AI supercomputers.The partnership also extends to the PC market, leveraging the annual 150 million notebook market. Huang highlighted the innovative use of TSMC’s foundry for Nvidia’s GPU chiplets, combined with Intel’s CPUs through multi-technology packaging. This “mix and match” approach enables rapid innovation and complex system development

-

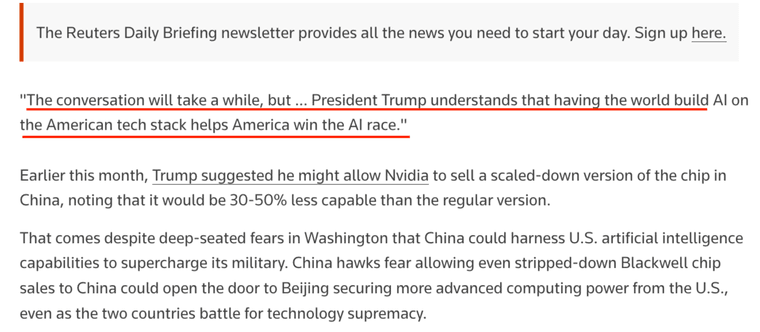

more news on allowing tier 1 silicon into China.......I think it's coming

David Sacks, White House AI & Crypto Czar, urged the U.S. to reassess its export control policies in light of China’s advancements in AI technology. In a post on X, Sacks highlighted Huawei’s launch of a new AI chip to compete with Nvidia and China’s directive to its companies to avoid purchasing certain Nvidia AI chips. He argued that China’s ability to produce its own chips shows it is not dependent on U.S. technology and aims to compete globally. Sacks warned that restrictive export controls could push countries towards China, risking America’s lead in the AI race. He noted Huawei’s strategy of clustering chips to compensate for weaker performance and criticised bureaucratic delays that benefit Huawei. Sacks advocated for allowing U.S. companies to sell technology abroad with security measures, particularly to allies, to maintain a competitive edge and prevent China from dominating the AI and semiconductor markets.

-

Breaking news

Nvidia just unleashed a massive $100 billion deal with OpenAI, announced 10 mins ago.

It’s not just a cash dump—think of it as a mega partnership where Nvidia’s pumping in up to $100 billion over time to power OpenAI’s huge AI setup, loaded with at least 10 gigawatts of Nvidia’s silicon.

Basically, OpenAI’s taking that money and pouring it right back into Nvidia’s GPUs, solidifying Nvidia’s grip on the AI compute game.Nvidia’s boss, Jensen Huang, called it “the next big leap,” hyping their decade-long collaboration vibe from the DGX days to ChatGPT blowing up. OpenAI’s Sam Altman is buzzing, saying, “It all starts with compute,” picturing this as the backbone for an AI-driven economy.

They’re talking proper game-changers—AI factories for next-gen models like GPT’s successors.

It’s a proper power move against AMD and big players like Google with their custom chips, while giving OpenAI a head start over Anthropic or xAI. Intel’s $5 billion deal looks like small fry next to this.

Batter up!

-

Details will emerge but yes Nvidia are buying a big piece of OpenAi

To build 10GW will require 7M Blackwell ultra equiv chips and cost $300 billion so one can only assume that the $100B is capital which will then be leveraged with debt. 7M chips is more than all life to date GPUs sold. it's 100k racks. Crazy

-

Nvidia's investment in OpenAI could be worth as much as $500B in revenue, BofA says, revising PT to $215. They read my post.

-

All time high on Nvidia today $187 as several analysts up their target to between $240-$250. Late to the realisation, again.

-

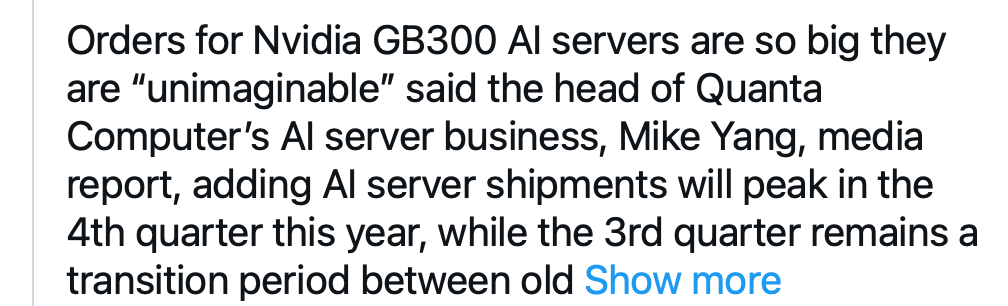

WiWynn, a major AI server original design manufacturer (ODM) partnered with NVIDIA, say they are grappling with an extraordinary surge in demand, with order visibility now stretching through 2027.

Despite operating facilities in Taiwan and a new U.S. plant set to nearly double production capacity by the end of this year, the company is still struggling to keep up. WiWynn is actively scouting new factory locations, with power supply capacity being a pivotal consideration. Key clients, including NVIDIA, OpenAI, Oracle, Google, and Meta, are aggressively scaling up investments in AI infrastructure, signalling that the AI arms race is intensifying. This robust demand underscores a vibrant and rapidly expanding AI server market.

So, they invest heavily a year ago to 2X output and now this is no where enough. Visibility through 2027 is impressive. BTW analysts currently have 2027 as flat for NVDA-sure it is

We said if before, POWER is the new constraint. Not just in the DC but also the factory that makes the servers-why, because these systems must be tested so hooking up a 'system' of X racks needs substantial juice

-

Wowsa

BREAKING: Nvidia, $NVDA, now represents 5.04% of the MSCI All Country World Index.

The MSCI ACWI Index captures ~85% of global equity markets, including large and mid-cap stocks.

Nvidia's weight now significantly surpasses Japan's 4.78% share, the world’s 3rd-largest stock market.

By comparison, China, the UK, and Canada account for 3.33%, 3.23%, and 2.92%, respectively.

Nvidia’s contribution to the index is now larger than France and Germany combined.https://x.com/KobeissiLetter/status/1975391629906485511#

A bit frothy, perhaps?

-

Someone on X making a statement (27k tweets(busy busy)) and calling it 'breaking news'. as though they are Reuters or similar.Someone who bashes 'equity' 24/7 but likes Gold. It's a very insightful observation ;). It's just envy they missed out. Remember, we paid $25.

It's about as useful as Pistonheads Mr Whippy 'Nvidia? They make gaming GPU, right' and another gem ' Nvidia at $40-LOL this will end well'. He was right-it did.

If Nvidia is the most profitable company in the world(fact) then why should it not also have the highest valuation? A valuation that is relatively, lower than KO, Starbucks, Unilever, CL and 1/10th the value of Palantir?

In other breaking news Nvidia now exceeds the combined GDP of all the world’s coffee shops.