Nvidia News

-

The Nvidia B40 (also known as the RTX Pro 6000D) is being positioned as the replacement for the H20 GPU in China, following U.S. export restrictions on advanced AI chips. It is based on Nvidia's Blackwell architecture and uses GDDR7 memory, allowing it to comply with trade controls.

Availability: Production began in June 2025, with general rollout expected in July and throughout Q3. Technically this will catch the current quarter((Q2) being May-July so potential for additional revenue.

Price: Estimated at $6,500–$8,000 USD per unit, making it more affordable than the H20, which exceeded $10,000 USD.

Sales potential: Analysts expect B40 shipments could reach $1–3 billion USD in revenue per quarter, depending on demand and licensing constraints. -

I see that AMD are giving it large at a conference in California….the report goes on and poses the question is it the end for Nvidia ….

-

AMD like many other companies in the sector like their marketing spin. Today AMD has somewhere between 3-5% market share in the DC.

Are their chips poor. No they are good. However what are we seeing out in the wild. A few chips, 100s? Try 200k and soon 1M in the data centre. AMD have no real networking ability. They can not scale out their clusters such that the DC acts as one giant GPU-all talking to one another. For small (a few nodes) they work just fine but giant systems, nope.Further, where are these chips. On a slide deck and in a lab. Nothing they have produced to date is remarkable. And remember one thing. AMD valuation is more expensive than Nvidia based on accepted metrics. They have lower growth and lower margins-so why buy the stock rather than buy Nvidia. AMD will grow and the stock will appreciate over time, I have no doubt but it's a follower-table scraps is my opinion.

Software Ecosystem (Most Important)

CUDA: Proprietary, mature, and widely adopted GPU computing platform.

Thousands of optimised libraries (cuDNN, cuBLAS, TensorRT, etc.).

Seamless support for AI frameworks (PyTorch, TensorFlow, JAX).

Massive developer community(millions who prefer CUDA because end customers want CUDA) and industry-standard tooling.

AMD ROCm is open-source but underdeveloped by comparison—missing features, poorer documentation, and inconsistent support across models and frameworks.Networking and Scaling

Nvidia supports hundreds of thousands of GPUs in a single cluster (e.g., Selene, Jupiter).

Uses NVLink, NVSwitch, and Infiniband (via Mellanox) for ultra-low latency, high-bandwidth scaling.

NCCL (communication library) scales efficiently and is deeply integrated into Nvidia's stack.

AMD supports a few thousand GPUs max per cluster. No NVLink equivalent. Infinity Fabric is decent within nodes, but poor between nodes.Tooling and Developer Support

Nvidia offers:

Nsight Systems & Compute for profiling

CUDA-GDB for debugging

Triton Inference Server for deployment

Mature support in all major ML and HPC stacks.

AMD tooling is basic and lacks the polish, breadth, and deep integration needed for industrial-scale projects.Vertical Integration

Nvidia offers:

THE FULL STACK

Omniverse, CUDA, and cuOpt for simulation and optimisation

Delivers full-stack solutions from chip to cloud, ready to deploy.

AMD offers EPYC + Instinct chips but no full-stack equivalent—relies heavily on partners and lacks an ecosystem play.Market Trust and Ecosystem Lock-in

Enterprises, research labs, and hyperscalers have built years of infrastructure on Nvidia.

Switching is costly—not just financially, but in engineering effort and risk.

Nvidia also provides enterprise-grade support, training, and long-term stability.

AMD’s competitive silicon is often overlooked due to software and ecosystem gaps.Conclusion: Nvidia is 5–7 Years Ahead

CUDA alone puts Nvidia 5+ years ahead in developer adoption and ecosystem maturity.

In networking, software, and scalability, AMD has only recently started catching up—but is still 5–7 years behind in real-world deployments.As we discussed a year ago-the DC is the land grab and Nvidia have put their stake in the ground-to displace them would need 'trillions' and a system that was much better. You will hear 'AMD are catching up' yes, to old Nvidia tech. Nvidia are not standing still are they. In fact I think the gap is getting bigger.

Unless AMD makes massive coordinated progress in software, interconnects, and cloud enablement, this gap will persist.

-

And taking all of that into account, AMD still need to make the chips. TSMC and MU seems pretty busy making everyone else's chips so AMD will be severely constrained for the next several years

")

Enough said. PE multiples are pretty much the same. Growth is not!

And for some insight into investment decisions. What should keep Nvidia out in front, assuming we take Huang out of the equation. A visionary leader who has not put a foot wrong. It's very easy to say we will take him on and win.

With all the money they make what are they doing with it? Spending more on R&D, partnering or buying the best complimentary tech(companies) and hiring the best talent. If you are top of your class at MIT would you rather work for Nvidia or AMD-Nvidia have the best toys and I doubt money is the primary motivator but they prob pay more too. I believe Nvidia offer employees very generous/discounted share incentives, 22 weeks maternity, free food in their offices, health benefits and industry leading salaries and a choice of very high end office furniture. Whatever helps to keep the tech-bros happy

The bigger picture is Nvidia is massive in so many segments, robotics, autonomous vehicles, omniverse, health and human sciences. Quantum. You rarely hear anything about AMD-well, apart from their self promotion. Im not worried about AMD in the slightest.

-

Hi A,

Micron is +30% over the last month alone. What we want to see is strong HBM growth-very strong. How the market reacts is unknown and largely unimportant for us investors.

As for Nvidia. It's well deserved imo. It is the most valuable company in the world by a long way

")

-

Yesterday Jensen Huang during the company's AGM, said the following:

Just beyond AI agents, the next wave is already coming. The next wave is physical AI—robots that see, reason, and interact with the physical world. Robots and all the AI infrastructure to train them will be the next multi-trillion-dollar industry. NVIDIA builds the AI factories to train them, the digital twin worlds to simulate them(Ominiverse), and the robotic computers deploy them. We give them intelligence in an AI factory, fine-tune their skills in a virtual gym(Omnivores), and eventually deploy them into factories, warehouses, and homes to increase the world's labour force.

Today, nearly 100 NVIDIA AI-powered AI factories and buildouts are underway around the world. That’s double what we saw a year ago, and they’re getting larger. The average number of GPUs per factory has also doubled. These breakthroughs drove strong performance. Revenue more than doubled to $130 billion. Operating income and EPS grew 147%.

We’re at the beginning of a decade-long AI infrastructure buildout. Demand for sovereign AI is growing around the world. We’re partnering with companies and governments across Europe, Japan, South Korea, Taiwan, Canada, Southeast Asia, the Middle East, Latin America, and Africa to build regional AI infrastructure.

AI factories, a new type of data centre, are being established across the globe to manufacture AI and empower these next-generation applications. AI factory projects require tens of gigawatts of AI infrastructure(how much is 10s? 25 = $1T). It’s set to be built in the coming years, and NVIDIA is uniquely positioned to capture this opportunity with our full-stack approach(we repeat this over and over-the stack not the chip, not the rack 'total solution), systems engineering expertise, and large ecosystem of technology partners.

-

This is clarification from OpenAi due to fake news being circulated a few days prior or maybe OpenAI were thinking about buying another product and Jensen called Sam :). And it also confirms what we believe. You can offer an alternative product but you still can't usurp the King for a number of reasons. Nvidia make no secret of the fact that you get allocation based on a number of criteria. Loyalty being one. Nvidia hold the cards, have a massive moat and stronghold on this entire industry. Right now I would think there are 10 buyers for every 1 chip and the demand supply imbalance will prevail for many many years imo because we know supply is limited to packaging scale up.

-

The first company in history to reach a valuation of $4T. What a legend, Jensen Huang.

-

Less, it was $20 in Jan 2023 and in June 2023 it popped to $40 ($1T). We paid $25.60.It's always interesting looking back. I save articles by so-called experts that I couldn't be more diametrically opposed and yes, get a kick out of them continuing to shout at the clouds. And a shout out to guy vert who posted against the herd on PH some time back saying he wasn't selling and why!. A lone voice on that thread of 'experts'.

Nothing goes up in a straight line and at every new high, some decide to cash in their chips. It matters not. I think the company has a lot left to offer, as do several others which also hit ATHs today-and for good reason.

Please, I dont need thanks-someone might come along and tell me 'no thanks from me'

-

Less, it was $20 in Jan 2023 and in June 2023 it popped to $40 ($1T). We paid $25.60.It's always interesting looking back. I save articles by so-called experts that I couldn't be more diametrically opposed and yes, get a kick out of them continuing to shout at the clouds. And a shout out to guy vert who posted against the herd on PH some time back saying he wasn't selling and why!. A lone voice on that thread of 'experts'.

Nothing goes up in a straight line and at every new high, some decide to cash in their chips. It matters not. I think the company has a lot left to offer, as do several others which also hit ATHs today-and for good reason.

Please, I dont need thanks-someone might come along and tell me 'no thanks from me'

@Adam-Kay said in Nvidia News:

Please, I dont need thanks-someone might come along and tell me 'no thanks from me'

Haha. It’s a tough crowd some nights!

-

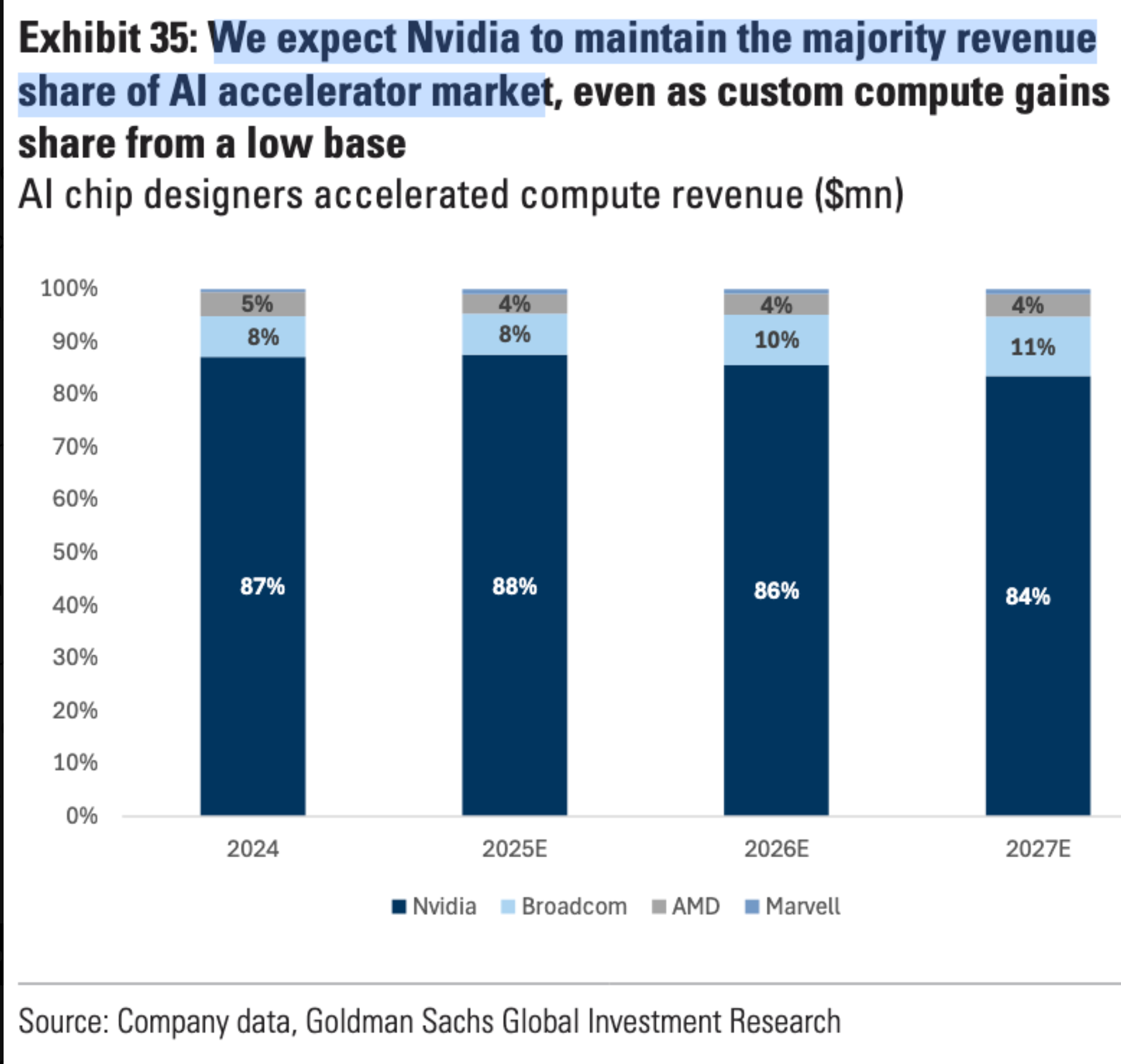

Grom GS today-nothing we don't already know. Obviously the TAM is growing at a large rate. In fact they are speculating on beyond 2025 but I can live with 84% market share

-

Nvidia CEO Jensen Huang will hold a media briefing in Beijing on July 16, Reuters reports, raising hopes a new China-focused chip may be unveiled that meets US export controls.

Looks like the B30 GPU, designed specifically to meet export controls, will be announced-availability set for September with several large customers in China having already placed preliminary orders worth billions. I would think around 2M chips per year @ $8k per chip is the size of the market-call it $4B/Q.

The export controls, limit two critical chip features. Bandwidth and Speed(operations/s). Bandwidth is nerfed vis DDR memory as opposed to HBM.

Useful insight. Why, if the B30 is significantly less powerful than local competing alternatives, namely the Ascend range from Huawei, proving to be in high demand? CUDA! The backbone of their moat now and for the next decade at least.

-

Almost certainly Nvidia based-Huang met Trump at the WH last Friday for one on one talks. Slowing down?

-

This is big.

Nvidia’s getting the green light to restart H20 chip sales to China after U.S. assurances on export licences, a big win after a $5.5 billion hit from unsold stock and potentially $15 billion in lost sales. This reverses a Trump-era ban , boosting Nvidia’s shares(almost certainly) and lifting tech stocks, a $17 billion market for Nvidia, can now access H20 chips for AI development, fuelling firms like Baidu, Tencent, Alibaba. Nvidia’s also launching the RTX Pro GPU, a cheaper, export-compliant chip for smart factories. It’s a massive deal for Nvidia’s bottom line and keeps them in China’s AI race.

-

And to remind everyone. Nvidia not only took a huge hit last Q(5.5B), they have about $5B in inventory just sitting around. The accounting will be a reversal of the inventory provision +$5B+ PLUS the revenue generated from renewed sales, +$5B, probably next quarter. Will we see a monster guide for Q2.Likely. Something like +$13B top line QoQ and a huge margin improvement from the provision. With the current quarterly cadence of +$8B excluding China we can expect actual Q2 revenue of circa $60B and earnings of at least $32B

-

And to remind everyone. Nvidia not only took a huge hit last Q(5.5B), they have about $5B in inventory just sitting around. The accounting will be a reversal of the inventory provision +$5B+ PLUS the revenue generated from renewed sales, +$5B, probably next quarter. Will we see a monster guide for Q2.Likely. Something like +$13B top line QoQ and a huge margin improvement from the provision. With the current quarterly cadence of +$8B excluding China we can expect actual Q2 revenue of circa $60B and earnings of at least $32B

@Adam-Kay said in Nvidia News:

And to remind everyone. Nvidia not only took a huge hit last Q(5.5B), they have about $5B in inventory just sitting around. The accounting will be a reversal of the inventory provision +$5B+ PLUS the revenue generated from renewed sales, +$5B, probably next quarter. Will we see a monster guide for Q2.Likely. Something like +$13B top line QoQ and a huge margin improvement from the provision. With the current quarterly cadence of +$8B excluding China we can expect actual Q2 revenue of circa $60B and earnings of at least $32B

Sorry to be fick but I thought that NVidia was selling every scrap of whatever they could make, and had a backfilled order book for 18 months or more? If that's the case then how can they have $5bn of inventory sitting around?

I expect I've missed something somewhere.

-

During the Biden tenure the US banned the Hopper-H100 if you recall. Enter the H20 which was a restricted version, produced to meet two core prescriptive limits (for china), bandwidth and operations per seconds. Approx 4 months ago Trump restricted the H20 leaving Nvidia holding $5B of unsold inventory and pretty much ejected them from the China market. Nvidia said at the time 'we are taking a $5.5B charge to our earnings' and would have guided $52B for Q1 if not for the restriction. Instead they guided $43B and made the decision not to include any china revenue in their guide-obviously there were and still are China sales however, immaterial to the mass market which was H20.

Today's news is fantastic. Whether this is a one off, clear the inventory or something else, we don't know.

Nvidia also has the further restricted B30 on deck.

I personally think it is the right thing to do, purely on the basis, China would have found a way to acquire the technology, it's good for relations and US business. It's narrow minded to hurt US business, less tax dollars, less dollars for R&D and force China to innovate faster. Let's remember the US has Blackwell which is 30X more powerful than H20. They ought to lead with this technology, right.