-

The company has confirmed this week:

-

Increased DLC monthly capacity to 3,000 racks. Up from 2,000 in December. It's worth noting these are currently $3-$4M racks and will soon be 5-6M with GB300.

-

By December they will have $50B revenue run rate (capacity).

But it's not enough! NB: A new Saudi facility is approved, clearly a strong signal of many more projects in the pipe line.

Plans.

Silicon Valley Green Computing Park (B20-B23)

Rack-scale integration with liquid coolingDatacentre BBS and cloud services-this part of SMCI 4.0 which will be discussed in detail next week at Computex.

APAC Science and Tech Centre (B62)

New land under negotiation for B63Supermicro Malaysia Campus with partners

High-volume subsystem and rack-scale production onlineFuture site plans

New Silicon Valley facilities in progress (B31, B32)New Silicon Valley facility in progress (#1081, Milpitas)

New BV (Netherlands) production facility in progress

New US site in plan – East Coast

New Saudi Arabia and other international sites in plan

-

-

The future is bright …the future is SMCI…looking exciting and good for the share price

-

clearly they are planning for way beyond $50B annual run rates.

Not speculation-they are Nr 1 in Generative AI systems and their AI side of the business grew 500% YoY.I want to see them return to a tax paid Net margin of 10% min. I think with scale and DCAAS (DC as a service) they will. But I work off of, say $50B = $5B net

-

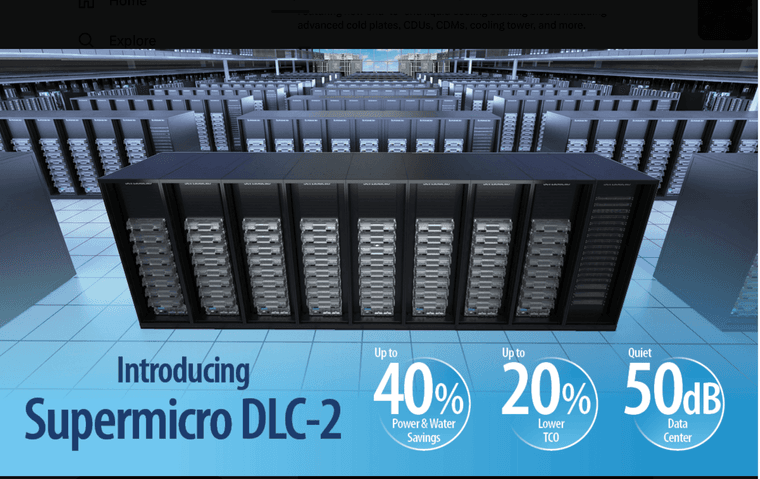

Supermicro Introduces DLC-2, the Next Generation of its Direct-to-Chip Liquid-Cooling Solution

Featuring new end-to-end liquid cooling building blocks including advanced cold plates, CDUs, CDMs, cooling tower, and more.

Acronyms:

CDU-Cooling Distribution Units

CDM-Cooling Distribution Manifold

Cooling Towers

and more")

50dB is quiet. A typical data centre is in the 92-96dB range. Irradiating noise is significant plus for employees and the neighbouring environment.

Details are starting to emerge and will peak next week when it is formally launch at Computex.

-

The company is touting this as revolutionary. We will see

Don’t miss , CEO and Founder of Supermicro, as he unveils our revolutionary Data Center Building Block Solutions

(DCBBS) at Supermicro Innovate!

(DCBBS) at Supermicro Innovate!

-

Good article here explaining whats new with SMCI DLC-2. Previously just the GPU/CPU had cold plates, the latest systems have cold plates on all the major components inc memory, power supplies, voltage regulators etc.

https://www.nextplatform.com/2025/05/15/pushing-ai-system-cooling-to-the-limits-without-immersion/

Nice to see SMCI lead the market with these developments

-

Supermicro (SMCI) Embarks on Major Recruitment Drive in Saudi Arabia Following a $20 Billion Agreement

Supermicro has been actively recruiting in Saudi Arabia for roughly the past month. The positions are quite varied, spanning roles such as Senior Service Engineer and Senior Sales Manager.

Notably, as previously highlighted, Supermicro began its hiring efforts in Saudi Arabia even before officially announcing its partnership with DataVolt. This reflects the strong trust that the global leader in liquid-cooled AI rack solutions has in its new Saudi collaborators.

In a further noteworthy update, Supermicro has unveiled its latest innovation, the DLC-2, a cutting-edge liquid-cooling system designed to cut water and energy use in data centres by up to 40 percent. The technology is also said to lower a data centre’s Total Cost of Ownership (TCO) by as much as 20 percent.

These reductions are made possible by expanding the cold plate coverage across server components, which enables fewer fans to operate at reduced speeds.

Moreover, Supermicro’s DLC-2 liquid-cooling system can reportedly capture 98 percent of the heat produced by a server rack, allowing for higher inlet liquid temperatures (up to 45 degrees Celsius). The company states:

This is, naturally, a significant benefit for data centres in Saudi Arabia’s desert environment, where high daytime temperatures and limited water availability pose challenges.SMCI has officially confirmed it is building a factory in Saudi. Clearly, they expect many more deals in the ME-and why not. They seem to have the best product for the job!

-

Nice. The Godfather of AI is joining Charles Liang which is a big endorsement 5pm GMT tomorrow.

-

Elon Musk commented on June 2, 2025, about the Colossus 2 supercomputer. According to a Washington Post article published on June 1, 2025, Musk told CNBC that Colossus 2, described as the world’s “first gigawatt-class training cluster,” is expected to come online “in about six months, maybe nine,” implying a timeline of approximately December 2025 to March 2026

What we know so far :

168 Tesla Mega packs are onsite as of May 2025. This will provide 700MW in back up power.

The project is for +800,000 B200 and B300 chips. All Blackwell and liquid cooled.

Worst case scenario the racks will start being installed July through March. This is Q1, Q2 and Q3 of SMCI FY 2026.

The total rack spend is $40-$44 billion.

Based on Dell's own public statements they have secured $5 billion-actually their exact comment was ' we are close to securing $5B'

At the end of May Dell stated their backlog was $12 Billion, throwing shade over their historical 50% share of Xai projects! 50% would be min $20 billion, coupled with the fact Dell have other customers.

Dell has never supplied Xai with any DLC.

SMCI have set up local operations to support Xai long term. A very good sign of material collaboration.

It is yet to be confirmed but I think SMCI have secured 35-39 billion or 88% of the Colossus-2 expansion.

If true they will very soon file an 8-K noting material additional funding via debt, convertibles and possibly equity to support this project.

Do they have the capacity to deliver 10,000+ racks over 9 months? Yes they do. Current capacity is somewhere north of 2,500 DLC racks per month with a plan to expand to 5,000 pm within the next 18 months. 3k by Dec......

Is the Q1 guide about to sing? Probably

-

Nvidia’s quantum computing alliance with Supermicro, Quanta, and Compal is seriously interesting stuff.

Blackwell GPUs, are at the heart of it, powering hybrid quantum-classical setups that crunch data for things like quantum simulations or cracking optimisation puzzles.

Rubin & Feynman, Nvidia’s next-gen architecture (whispered to drop around 2026), could take this further, maybe with bespoke quantum control tech for tighter integration.Supermicro’s job? Building racks that make this magic happen. They’re designing setups with cryogenic chambers to keep quantum chips frosty at near absolute zero, right next to liquid-cooled Blackwell GPUs. High-speed Ethernet or InfiniBand ties it all together, ensuring quantum and classical bits talk without lag. They’re also adding electromagnetic shielding to stop qubits throwing a wobbly. These modular racks let researchers swap parts as quantum tech grows, making it practical for real-world uses like drug discovery or super-secure networks. With Taiwan’s Quanta testing hardware and Compal running simulations, this isn’t just a small deal—it’s a bold step toward making quantum computing a reality

Nice to see Nvidia lean on Supermicros engineering leadership-confirming their close partnership

-

Jacob Yundt, CoreWeave’s Director of Compute Architecture, praised Super Micro Computer (SMCI) as an “incredible partner” for their collaborative approach, particularly in working on future products and implementing changes.

You don't say that unless you're currently buying their solutions. Corrweave have committed to spend $23 Billion this year on expanding their Data Centre reach. Following the crumb

-

From Elon Musk in an interview yesterday, he stated that currently he is sleeping at the Data Centre and the team are working in shifts 24/7. '110,000 GPU are just about to go in based on GB200).

In other news, whilst it's unverified, channel checks suggest SM has won a 2k rack order from Oracle which wouldn't surprise me as SM has a long history of working with ORCL.

-

I figured subscribing to the local papers would yield some info:

On Wednesday, June 18, a Daily Memphian reporter observed dozens of natural gas turbines and energy equipment stockpiled in a field at 2979 Stateline Road West in Southaven. None of the equipment appeared to be running, but it does seem to be multiplying. Two weeks ago, the reporter saw only six or seven turbines on the same lot.

Stateline Road is the address of Xai Colossus

-

Breaking: Supermicro Announces Proposed Offering of $2.0 Billion of Convertible Senior Notes

I wonder why they need $2B

Great news

-

News not well received thou…..is it a case of short sighted investors and not having a handle on what the $2B is for

-

Foxconn’s order visibility for AI servers extends into 2027, media report, citing spokesman James Wu, who added orders continue to outpace capacity. A few weeks ago, Foxconn said it rented factory space in Houston, Texas to help meet demand.

Foxconn also made the comment that they are working on two super-massive projects, both exceeding $100B each and one of them was originally thought to be $100B is now anticipated to be in the range $300-$500B. I would expect that to be Stargate. It is also worth noting that businesses like to publicise big numbers. Working on a $300B project doesn't mean they are the sole supplier, more the lead supplier. Still it's a headline Nr which is indicative of the scale and speed of this secular transition to accelerated computing and it bodes well for all participants.

- SMCI convertible debt has been priced and I would speculate they are paying very low interest rates, if any. We knew the debt raise was coming, it is a clear sign of very strong growth and grow they will.

The medium term stock price is largely irrelevant. it is dominated by short-sellers. If the company surprises with upside guidance, that short position will get obliterated.

If we look at the companies pre raise working capital and inventory /receivables conversion rates I believe they can now support up to $9B/Q in revenue.

Key considerations near term being margin expansion. Revenue is most definitely on the rise (XAi and Coreweave known mega customers). Every 1% margin expansion going forward is worth $80M per quarter(with a 15-20% QoQ growth rate) with scope for plus 3-400bps over the next 12 months. I believe, given their clear competitive advantages in custom DLC/DCBBS coupled with the now mature Blackwell architecture, their capacity which up until now has not been anywhere near fully utilised, margins will expand.

There is no way around capital raising when growth is so steep. Unless of course you have a gigantic margin(like Nvidia). SM could have just issued vanilla debt however the interest to service it would have been high. That too would be dilutive(to earnings) I don't think they are finished raising money because there is considerable growth to come.

Their quarter(Q4 fiscal 25) end is Wednesday next week. It's impossible to say how the current Q4 played out suffice to say it should be at the higher end of their guide for quite clear reasons. I'm more interested in their Q1 fiscal 26 guide which can only be a record imo. Large numbers of racks are being installed in Colossus-2 (imminently), Coreweave is cranking their DC builds. I believe they are working with Apple, Oracle and Meta and the more throughput they can achieve, their utilisation rates go up and therefore their cost per unit goes down which translates to margin expansion. The company may reaffirm their fiscal 26 guide of $40B, something I think they will achieve. This would represent a 65% revenue growth rate over 2025.

It is worth pointing out that Dell has net margins almost 50% lower than SM, a lot of debt and is laying off staff. SM sell more Ai racks than Dell. And Dell, despite their claims, do not make any Ai racks, they buy them from Quanta and Foxconn and adhere a Dell logo-and this is why their margins are so low.

-

Fujitsu is using TSMC(2nm) to manufacture a new AI CPU called MONAKA.

Super Micro Computer, Inc. (SMCI) is collaborating with Fujitsu to develop a green AI computing platform that incorporates Fujitsu’s Arm-based “FUJITSU-MONAKA” processor, targeted for release in 2027. This partnership focuses on creating energy-efficient, high-performance solutions for AI, high-performance computing (HPC), cloud, and edge computing environments.

Fujitsu’s claims of doubling performance and efficiency are bold but speculative, as competitors like AMD’s EPYC Venice (256 cores, 2nm) and Intel’s Xeon (with big-little core strategies) will also advance by 2027.

-

SMCI Convertible notes 'close'

SM announced the completion of a $2.3 billion total principal amount of convertible senior notes due in 2030 , inclusive of the full exercise of the option granted to the initial purchasers to acquire up to $300.0 million in additional notes.

“We’re grateful to our investors who align with our vision,” said Charles Liang, Chief Executive Officer and Founder. “With increasing demand for next-generation GPU platforms, this was a timely capital raise that reinforces our balance sheet with minimal dilution, enabling ongoing support for our customers’ ambitious growth strategies around AI-enabled DCBBS solutions as they scale up their operations.” Minimal dilution will be achieved by entering into a capped call contract which is a contract with the right to buy stock at a set priced (capped), in other words if the stock goes up they profit from the delta between the strike price and then market price subject to the cap(limit).

The convertible note issuance was structured with a highly favourable 0.00% interest rate (we figured zero interest), a five-year maturity term, and an initial conversion price of $55.20 per share—reflecting a conversion premium of approximately 35.0% over the Company’s closing share price of $40.89 on 23 June 2025. Combined with a simultaneous share repurchase(200M) and capped call arrangement, this structure aims to minimise the effect on existing shareholders.

As part of the transaction, Supermicro entered into a capped call hedge to increase the effective conversion premium to 100% of Supermicro’s share price as of 23 June 2025. Consequently, the impact of any dilution or cash liability from future conversions of the notes is expected to be mitigated, as the effective conversion price rises to $81.78 per share—double the Company’s closing price of $40.89 on that date.

Additionally, Supermicro repurchased approximately $200 million worth of its ordinary shares from note purchasers, in an effort to offset the potential effects of related hedging activities linked to the offering.

Supermicro retains the flexibility to settle any conversions in cash, shares, or a mix of both, allowing the Company to manage any prospective dilution or cash commitments stemming from future note conversions.