PHE and PHT

-

All YTD and net of fees:

Cobens Tech +34.5%

Lifestyle +22.24%Fundsmith -4.14%

Nest Sharia +8.26%

ARK Innovation (Cathy Wood) -0.96%

FTSE +5.4% -

Adam, stellar performance thanks again.

On Cobens Tech, what are your long term views as there continue to be such divergent views on tech and valuations. Ive seen your rationale for your investments and they all are sound, but as we've seen this year in particular markets seem more driven by emotions, sentiment, rumours and orange tan (latter having a limited lifespan of influence).

Do you think CTech has a defined end date before its perhaps not as strong a proposition, or will it be a permanent strategy?

-

Hi V,

When we launched in 2022 (and the forum is a good record for this) I said something along the lines:

I argued that technology was transitioning into a dominant innovation cycle likely to deliver sustained alpha and above-market earnings growth over the coming decade.

I havent changed my mind. The mandate for the portfolio is pure tech and businesses that benefit from its heavy use.

New opportunities present themselves along the way and we have been very active, moving away from some names and investing in others. Bio tech as well which has been a good investment also.

One should try and ignore geo political noise-yes it can be quick and profound at times but good companies correct just as quickly.

At the end of the day, investors conflate 'tech is a bubble' with some companies are a bubble. Look at AMD. The also-ran which gets some good news and it doubles-why? It's not rational but we get back to psychology. The 3 legged dog which wins 1 race and all of a sudden it's the champ. Crowdstrike is trading at a multiple of 150, so is Palantir. I can't tell you why, it makes no sense to me. But I can be sure that one wrong move and the stock will get battered-again.

The market is a pool of undervalued and overvalued companies. I have my own measures to gauge what a good investment is and im very happy with what we hold.

-

Hi Adam if I were to transfer some of my funds to Lifestyle from Global growth to hopefully give a better return with similar risk which one would you recommend. Thanks Jason

-

I think that would constitute advice, which Adam can't do. That said, to my knowledge you've only got the choice of Lifestyle for Withdrawal and Lifestyle for Income. Difference being whether you want to withdraw it as one lump sum at the target date, or leave it invested and draw down regular smaller amounts. The funds will then differ in terms of when they go into 'safer' investments, with the withdrawal one going into those a bit sooner, whereas the income one will remain invested to give it the best chance of sustained growth.

-

I think that is well put, Steve: Adam won’t be offering suggestions that could be constituted as advice on here.

We have a large chunk of ours in the Lifestyle for Income. More than happy with performance to date.

Might be handy if Adam can confirm the differences: what you wrote is my understanding, but it might also be useful to see how the two funds have performed over the past YTD, plus perhaps 1-3 years.

-

Thanks for explanations, maybe Lifestyle for income but starts paying income in maybe five years so I can keep adding money yearly. Hope that makes sense none of this is my area of expertise so I like thing explained in simple terms. Thanks Jason.

-

Hi Jason,

Thanks for your question. What I can do is provide the Lifestyle Factsheet. The main difference between Optimum GG and the > 10 years model of Lifestyle is Lifestyle is a 100% (98+2 cash) Equity portfolio cf GG contains some fixed income and other asset types. In strong market environments you will see Equity outperforming.

I can provide the information to you (any Direct Client) and after due consideration, you would make the decision which best meets your needs.

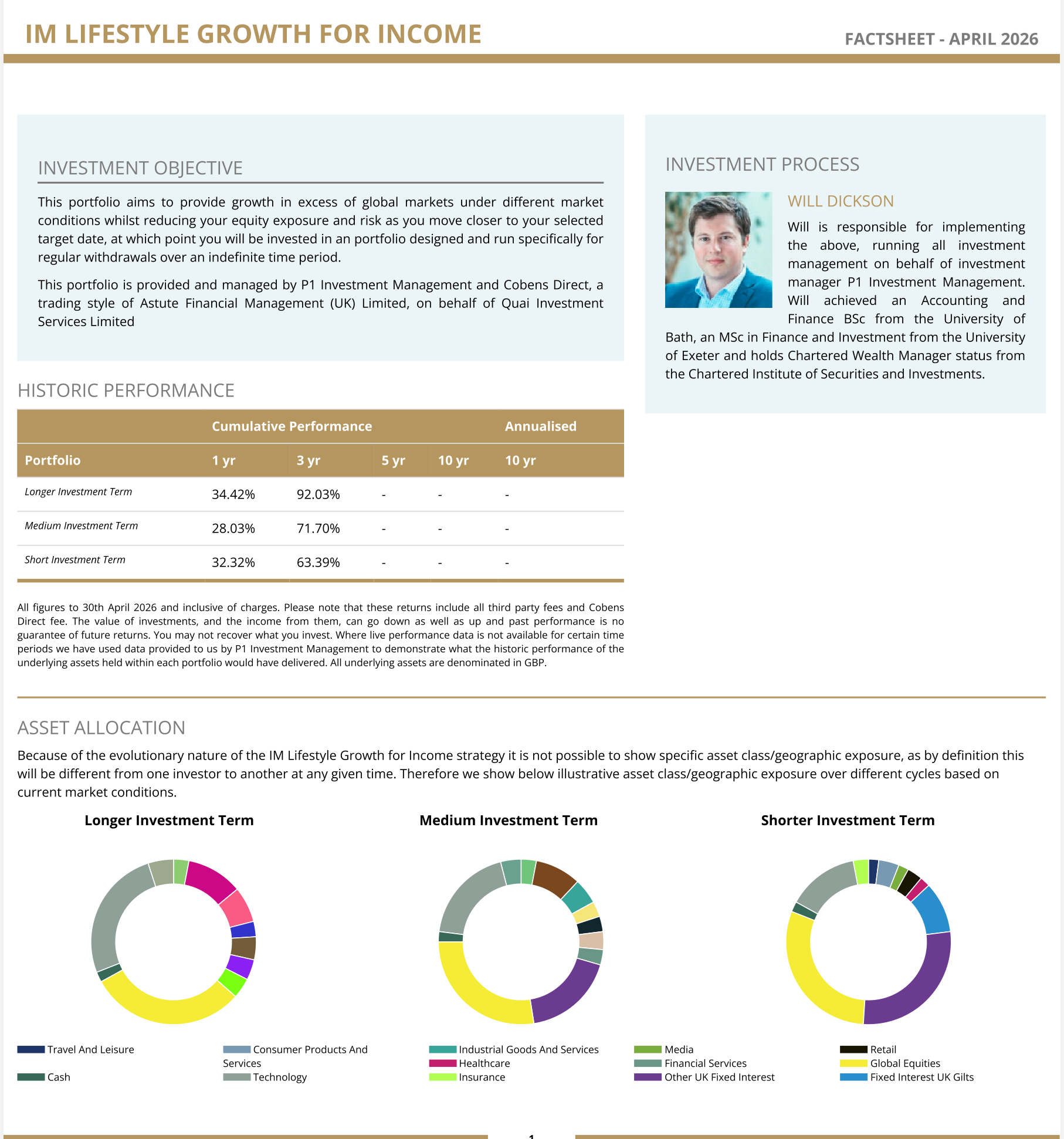

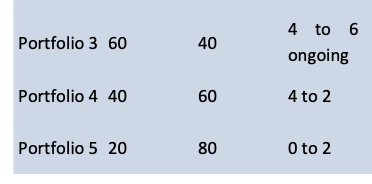

There are 5 Lifestyle models(100/80/60/40/20 Equity) and these are Long, Medium and Short, term.

Any performance mentioned recently is the > 10 years Long term. This is not an investment term lock in rather it is meant to indicate a time to retirement or target date and as such, maps to 100% equity and as one gets closer to retirement the models de-risk, addition fixed income products to avoid price shock closer to the target date.

The name income is not indicative of an income stream. It means as you get closer to your target date you would ultimately end up in the 60/40 'Income model of Lifestyle.

Here is the official objective:

IM Lifestyle (IML) also known as Target Date Portfolio's (TDP) comprise several Portfolio's designed

IML is a set it and forget it model of long term investment where individual investor asset allocation is rebalanced automatically as defined by their target date or default date of birth for SIPP wrappers but user defined for other wrappers.IML is designed for investors with a 10+ years’ time horizon and a preference for investment allocation to follow a well-defined path, taking on greater risk during the capital growth phase while the investor is younger and transition to more conservative investments for income generation as they get closer to target date.

-

Any questions just ask-alternatively I can talk through it if required

-

Thanks for the reply Adam, im basically 60 now so maybe looking at this as a 10 year plan for me wouldn't be the best.

As you know im fairly heavily into your tech and GG funds, I was just thinking how I could spread my money more evenly into another fund that may outperform GG with similar risk but in other areas of industry.

Hope that makes sense.

Thanks Jason -

You've got the option of setting the target date to be 15 years in the future as an example, then it would remain in the 100% equity for 5 years, before starting to slowly de-risk after that point.

-

Thanks for reply Steve, so do you think that is similar to just putting money into the IM 100 portfolio as that appears to be basically equity based.

Thanks. -

They are both 100% Equity however '100' is global equity whereas Lifestyle is chosen based our analysis

-

Hi Adam are YTD for both Lifestyle portfolios very similar.

As Steve said if I invested for 15 years would the first 5 years be at the highest risk, and also I assume if im not happy I can move my money out if I wish.

Thanks Jason -

the 5 models are identical for 'Income' and 'Withdrawal' the only difference is in their application. The Glide path(1 through 5 and 100% through 20%), with Income stopping at 3(60/40) and Withdrawal continuing on its path to model 1.

15 years would place you in the exact same portfolio, irrespective of which strategy you took. At year 11, withdrawal would move into 4 and Income would remain in 3.

-

Thanks Adam all becoming a little clearer now to me how it works.

-

To be fair it isn't that clear and that will change after the migration (web content wise)

-

Thanks Adam just another couple of points before I make a decision, can I still add and remove funds if I wish.

Thanks -

yes of course. The Target Date only maps the portfolio. Thereafter it's up to 'you'. Add, withdraw subject to wrapper of course(SIPP), switch to something else. To be clear you are not locked-in in anyway