PHE and PHT

-

Thanks for the reply Adam, im basically 60 now so maybe looking at this as a 10 year plan for me wouldn't be the best.

As you know im fairly heavily into your tech and GG funds, I was just thinking how I could spread my money more evenly into another fund that may outperform GG with similar risk but in other areas of industry.

Hope that makes sense.

Thanks Jason -

You've got the option of setting the target date to be 15 years in the future as an example, then it would remain in the 100% equity for 5 years, before starting to slowly de-risk after that point.

-

Thanks for reply Steve, so do you think that is similar to just putting money into the IM 100 portfolio as that appears to be basically equity based.

Thanks. -

They are both 100% Equity however '100' is global equity whereas Lifestyle is chosen based our analysis

-

Hi Adam are YTD for both Lifestyle portfolios very similar.

As Steve said if I invested for 15 years would the first 5 years be at the highest risk, and also I assume if im not happy I can move my money out if I wish.

Thanks Jason -

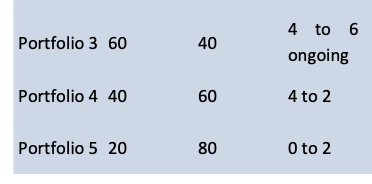

the 5 models are identical for 'Income' and 'Withdrawal' the only difference is in their application. The Glide path(1 through 5 and 100% through 20%), with Income stopping at 3(60/40) and Withdrawal continuing on its path to model 1.

15 years would place you in the exact same portfolio, irrespective of which strategy you took. At year 11, withdrawal would move into 4 and Income would remain in 3.

-

Thanks Adam all becoming a little clearer now to me how it works.

-

To be fair it isn't that clear and that will change after the migration (web content wise)

-

Thanks Adam just another couple of points before I make a decision, can I still add and remove funds if I wish.

Thanks -

yes of course. The Target Date only maps the portfolio. Thereafter it's up to 'you'. Add, withdraw subject to wrapper of course(SIPP), switch to something else. To be clear you are not locked-in in anyway