Micron Technology

-

Micron’s “monster” Q3 guidance, issued in mid-March 2026, projected revenue of approximately $33.5 billion with an 81% gross margin. At the time, this was beyond strong. The guide is the strongest growth in corporate history-but it just got even better.

Analysts and consensus models likely incorporated more conservative server DRAM contract price assumptions of around 10–15% QoQ for Q2 2026 (April–June calendar, microns quarter 3 covers March through May). Why, because Trendforce provide market data on what customers are paying/bidding.

Yesterday TrendForce revisions have dramatically upgraded that outlook to roughly +45% QoQ for server DRAM prices. This meaningful positive surprise implies higher average selling prices (ASPs) than previously modelled, particularly as new contracts roll into Micron’s fiscal Q3/Q4 2026 and Q1 2027.The impact could be substantial: elevated server and HBM pricing would lift revenue beyond current forecasts while expanding already-record margins further, thanks to the favourable product mix and limited near-term supply growth. Operating expenses are largely fixed whether they deliver $33B or $40B for that matter.

Modelling that ASP change we are looking at $38B revenue and $25 eps. This is one quarter not a year with a stock now at $357!

Worst case scenario-prices stabilise, best case they keep rising for the next year. They aren't going to fall and will likely rise a bit more but if we model flat ASP and just look at MUs bit growth of 25% thats a base of $100 EPS for 12 months and a 25% growth rate going fwd. With a PE of about 3.

-

Official Nr's on memory for the April-June Q

Q2 2026

Quarter on Quarter(not annual changes) ASP-

PC DRAM prices: revised up from +10~15% to +40~45%

-

Server DRAM prices: revised up from +10~15% to +43~48% The big one

-

Mobile DRAM (LP5X) prices: revised up from +13~18% to +58~63%

-

eSSD prices: revised up from +15~20% to +68~73% The big one

-

TLC/QLC NAND prices: revised up from +15~20% to +60~65% The big one

-

Overall NAND Blended ASP: revised up from +18~23% to +70~75%

so when I said +45% above- it looks like it's actually a lot more-nice!

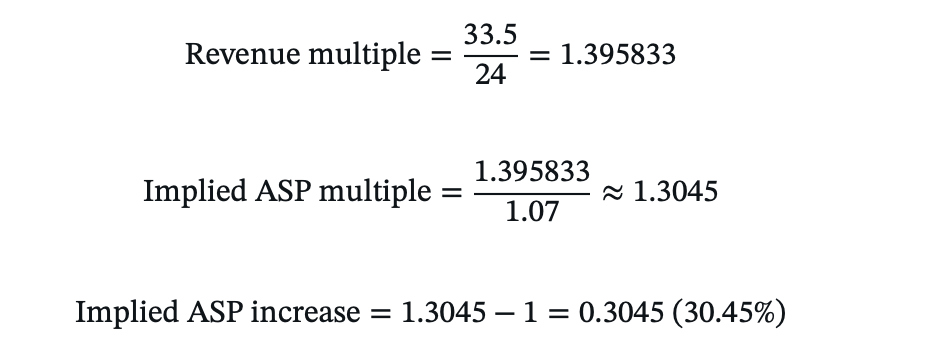

Looking at last Q, $24B and a $33.5B guide. We know bit growth is limited to +7% QoQ maybe a bit more but that is still a lot so to get to 33.5B we can infer the assumed ASP rise built into their model notwithstanding any change in mix.

Given prices are up a lot more than 30.45% a massive beat is a given. It wouldn't surprise me if they report close to $40B this quarter and $24-$25 eps. Last years Q3 revenue was $9.7B. $1.62 eps.

-

-

Micron taking a bit of a bloody nose again today ….

-

It's frustrating for sure, C. However it's the same pattern of behaviour with 'AI' at the moment-disbelief.

What you have here is the business and its management (at the coal face) taking new business, signing unprecedented 3-5 year supply deals, committing vast sums in Capex and now doubling down on that investment. Two camps, believers and non believers. There is also a lot of foul play and FUD.

Everyone is forgetting that GOOG themselves is one of the biggest 'memory' buyers and they have the biggest 2026 Capex ($175B)-they too are constrained by memory.I noticed yesterday that Nvidia is now trading at multiples below the S&P average yet its growth rate is the highest. When you look at the situation, holding stocks that are thriving but beaten down it's quite clear when the fear lifts we will see a profound correction.

I think the market is wrong and not just slightly so.

-

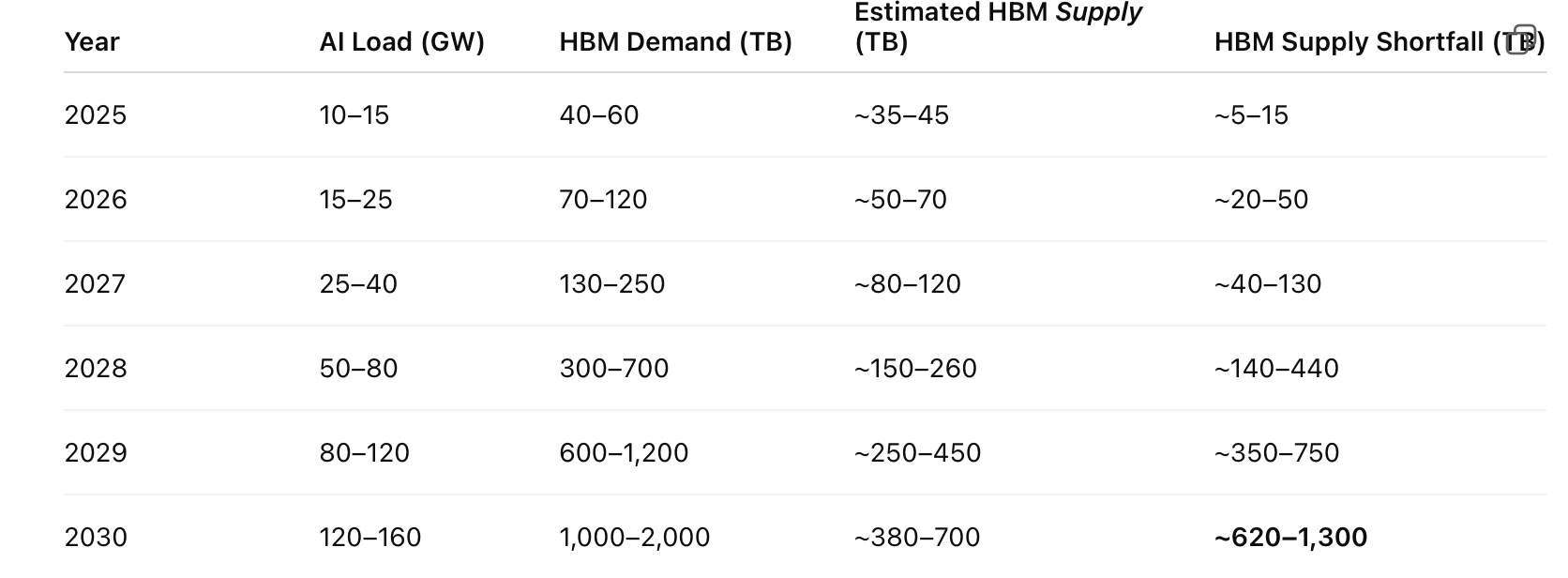

This is based on known committed data centre alone. It does not include edge cases. This additional annual GW (the only smart way to look at the build out). And yes 2025 was a big year but compare 15GW of built to 25 in 2026 and 40 in 2027.

Reiterating-algo's and compression make no difference to the HBM required at the server(hardware) level. It just makes inference cheaper. As it gets cheaper, consumption increases.

Shortage is measured is millions of TB. 2025 up to 50M TB shortage and growing to 1 billion TB shortage in 2030. Or looking at it another way 2026 demand is 120M TB but the shortage could approach 1B TB in 5 years. Even if wrong by a huge margin, demand exceeds supply. This is based on all Capex committed today-even if Capex increases next year and beyond, it will have minimal impact on the demand supply landscape to 2030 due to build duration.

-

I’m sure you’ve seen the note re Citi noting that DRAM spot prices have dropped by 6%. …. But they still give a higher price than today of $425 from $510

-

I have ;). Spot prices havnt fallen-oh 0.26%. Big firms hug the stock price. They never want to be an outlier. Im not aligned to 510 either

.

. -

These so called professional people etc …are never held accountable for what they write etc …

-

it's more a case of knowing how analysts work in reality. There is now supposed to be a 'Chinese wall' between sales and research. Is there in reality. Compliance wise yes(the appearance) but does it work?

What you find is big companies, the mega caps are always raising money, buying other businesses, planning etc and guess who they use. Citi, JPM, MS, Goldman. It's a billion dollar business. They court the companies/management so there is potential for conflicts of interest. It would be very rare for a big bank to underwrite a new capital raise and then have one of their analysts write an opinion rating the stock a SELL. It's bad for business. So, be very wary of analysts opinions. Further, you won't ever see a target too far from the spot price. If company X had a price of $100 an analyst might think it's worth $300 but there is no real benefit in sticking your neck out and stating it.

Wallstreet can be a swamp for the uninitiated. That is why, when it's noisy you sit back and do nothing. And the ME situation is nothing more than a blip in the journey. Yes it's tragic but it's been this way for 5 decades and it will have no lasting impact on what we are investing in.

The Middle East unrest has allowed all the lunatics to spring forth and spout everything imaginable to drive good stocks down, it works, that's why they do it. Things ive read this past week. Helium is running out-TSMC in trouble. Not true, yes Qatar produces a lot but the biggest supplier is the US-no shortage. Nvidia is redesigning Feynman, it's 2 years away and it's just a rumour(and where from). Feynman redisign = less HBM. Not true. Spot prices falling. Not true. Well, citing one website showing 0.29% is not proof of anything. As has been discussed countless times, fear causes irrational behaviour but it also presents opportunities.

We listen to management, after all they know what's going on, and assuming they aren't crooks we can rely on them far more than a guy on X. The biggest hang-over for anything tech related is capital spending. The markets kryptonite (capX). I see the polar opposite. GOOG aren't spending $170B on a hunch, Meta isn't spending $100B on a coin flip.

It won't stop the talking heads spouting the same falsehoods which is basically AI is not making money-that is 100% false. And in any case it's common sense that if you build a trillion dollar piece of infrastructure time is needed to turn that into a profitable business. You either believe in it or you don't. That is the bottom line. We are not blindly barreling down a runway heading for a brick wall with our eyes shut, we are fully engaged, watching, listening and reevaluating, daily. And what I see is the business keeps getting better and lately the values have only become more attractive.

The biggest mistake investors make is looking at the stock price and correlate(solely) that with the companies health.

-

Micron gave a business update today at cantor Fitzgerald.

Iran war has no impact on their business

Their raw material supply chain is in a far better position than their competitors.

Management expect material surplus cashflows to be employed buying back stock in the back end of 2026 (acquisitions and Capex commit current cashflows)-which tells more more to come.

ASPs will increase per bandwidth so memory being reframed as $ per performance not $ per bit. Very interesting and fits with the margin up narrative.Cantors raise price target to $700 based on what they have been told. Nice.

-

Here are the notes from the investor meeting today:

-

Fundamental Shift: From Price-per-Bit to Price-per-Bandwidth. This was the standout insight shared by Micron’s management.The memory industry is moving away from the traditional focus on price-per-bit (how many bits are sold and whether the price per bit rises or falls).

In the AI era, especially with HBM (High Bandwidth Memory) and high-performance DRAM, customers now evaluate memory primarily on price-per-bandwidth — i.e., how much data per second can be delivered to the GPU.

While price-per-bit may rise in 2026, price-per-bandwidth is expected to decline because newer products deliver significantly higher performance.

This allows Micron to increase average selling prices (ASPs) while customers perceive better price-performance and improved total cost of ownership (TCO).

Implication: Stronger pricing power, structurally higher gross margins, and a break from the old cyclical pattern where rising bit supply led to margin collapse. HBM and AI DRAM are now integral to overall GPU system performance rather than just capacity. -

Multi-Year AI Memory Supercycle Cantor Fitzgerald reiterated its Overweight rating on Micron and maintained it as a Top Pick, with a price target of $700.

Strong conviction in a multi-year AI-driven memory supercycle, despite broader market skepticism.

Key drivers include explosive HBM demand linked to NVIDIA platforms (including mass production of HBM4 for the upcoming Vera Rubin GPU)(remember the rumour they were excluded), rising memory content per server, and scaling AI inference workloads (more users and tokens require more bandwidth). Today and transitioning 198-288GB/GPU. Feynman is 1TB per GPU. Demand will grow 2X more than all available supply. -

Supply and Capacity Outlook-Micron’s 2026 capacity is fully sold out.

DRAM supply is expected to remain tight through at least calendar year 2027, with the first meaningful market balance not anticipated until 2028. And speculating, what markets will expand over the next 18-24 months-Robotics, edge cases? I think so!

Micron is well positioned to gain share as a credible dual-source supplier (alongside dominant SK Hynix) for high-value HBM. -

Capital Returns Management expects very aggressive share buybacks to commence in December 2026, supported by strong cash flow generation.

-

Geopolitical and Supply Chain Resilience-No material impact is expected from the war in Iran or related disruptions.

Micron’s supply chain for critical inputs (helium, LNG, and other raw materials) is more domestic/U.S.-centric than that of its Korean competitors, providing a relative advantage.

Overall Tone from Management emphasised the secular and durable(we said this 6 months ago) nature of AI-driven memory demand, evolving customer relationships (including more structured supply agreements), and how its high-value memory roadmaps directly enable more advanced AI capabilities. The company is positioning itself as moving beyond a traditional cyclical memory player toward a key AI infrastructure enabler with sustainably higher margins.(and why not, if Nvidia command 75+ gm so can Micron).

It sounds extremely positive to me. Management will always err on the conservative side but what they are saying is blue sky for 2 years-as far as they can see with everything sold out despite aggressive Capex and growing supply as fast as humanly possible.

The stock is up 20% from yesterday's lows. I wonder how those sellers feel today

-

-

That’s great information and yes nice to see the share price getting back to normal…hopefully a long way up from here

-

A line by line analysis of update commentary. All super positive.

HBM as a Major Driver-HBM remains a key driver for innovation, industry growth, and product differentiation. Micron previously set a goal to reach similar HBM bit share levels to its overall DRAM bit share (achieved in 3Q25).

As Samsung gains incremental share in CY26, Micron is expected to maintain or grow its position into CY27.

Next-generation HBM products will incorporate custom logic base dies, with initial adoption in HBM4E and broader uptake in HBM5.

Hybrid bonding is planned (not expected before HBM5 in 2028-2029):Why it matters:

hybrid bonding fuses surfaces almost atom-by-atom, allowing much tighter and denser connections.

Old method = stacking LEGO blocks with little connectors between them

Hybrid bonding = melting the blocks together so signals flow almost seamlessly

That leads to:

Faster data transfer between chips

Lower power consumption

Smaller designs (more compact stacking)

Higher performance overall

Customisation and complexity in HBM are expected to drive higher profitability industry-wide.Micron highlighted HBM as representing a high-teens percentage of wafers, with strong expectations for continued growth to meet future demand.

Dare One Say the Cycle Is Different This Time? (we think it is with a high degree of conviction) and it is not just because of AI although AI will allowed the market segment to proliferate (Edge cases). Management views the current cycle as structurally different due to:AI and data centre demand making memory a more strategic asset.

Greater customer collaboration on roadmaps.

Significant innovation (LPDDR5/6, SOCAMM, High Capacity DIMMs, GDDR6, HBM4/4E).

Multi-year lead times for supply additions (3+ years from shovels to equipment). No quick fix to meeting unmet demandWorsening trade ratios for HBM and potential imbalances (moving to 4-to-1 and higher in the HBM4/5 transition) further support a tight environment. This is a positive and refers to allocating HBM over other DRAM- the trade ratio is the trade-off which means other types of memory experiencing more supply constraint vs demand as a shift to HBM continues (Wafers being the common real estate). And remember, Wafers or WFE are limited, so allocation to various types of memory matters, causing potential imbalance elsewhere. More WFE starts = more equipment-ASML/KLAC, more raw materials, copper, interconnects, foundries and so on.

Strategic Customer Agreements (SCA)Micron recently initiated Strategic Customer Agreements (SCA), offering 5-year terms with “durable/sustainable” commitments and a critical focus on appropriate ROI for Capex.

Investors are awaiting more details, but management sees these as potentially providing greater durability to the business.Gross Margins and Path Forward-Micron guided May quarter gross margins of 81%.The firm does not view 45% as a “normalised” level (despite current market(stock) pricing implying it). The multiple is 3.X times. Ridiculously cheap.

Management remains positive on gross margins beyond May and highlighted a market shift toward pricing on a bandwidth basis (beneficial for customers and the pricing environment).Capex Outlook-Micron announced a substantial increase in Net Capex for FY26 to $25B (from prior ~$20B).

Further meaningful step-up expected in FY27 (construction-related Capex +$10B+ YoY; WFE spend also rising).

Expected FY27 Capex: $37B+.

Focus on expeditiously building clean room space, then equipping as needed, with a disciplined approach.

All manufacturing remains focused on becoming EUV-capable to support advanced HBM and leading-edge DRAM (layer counts moving from 1-2 to 3-5). This is stacking layers.Today Micron is only able to meet customer orders at between 50-63% customer variable/mix. The demand supply imbalance is getting worse-the vibe is the imbalance will last into 2030 maybe beyond. Management feel that high gross margins are the new norm. My takeaway is $20-$25 quarterly EPS is the new base line.

As you know many tech stocks are still trading at bubbly levels, Palantir 180X, Crowdstrike 70X. In my opinion that is as ridiculous as Micron trading at 3.5. In fact Micron generates as much revenue in 2 weeks as Palantir does in an entire year and generates 60X more profit. Their valuations are very close. Which would you rather own?

-

Just in from Semi Analysis-

DRAM prices are expected to more than double in CY26, with another double-digit ASP increase in CY27

LPDDR5 contract pricing up over 3x since 1Q25. Price likely exceeds $10/GB in 1Q26 on the open market

HBM remains structurally undersupplied through CY27. AI-based servers already see significant % BOM costs from HBM, before price hikes

We know B200 server prices(Blackwell) are going up 15–20% by year-endMemory is a massive % of the $250B in incremental hyperscaler spend this calendar year. (2/4)I think the $33.5B revenue and $19.5 EPS guide is far too low!

-

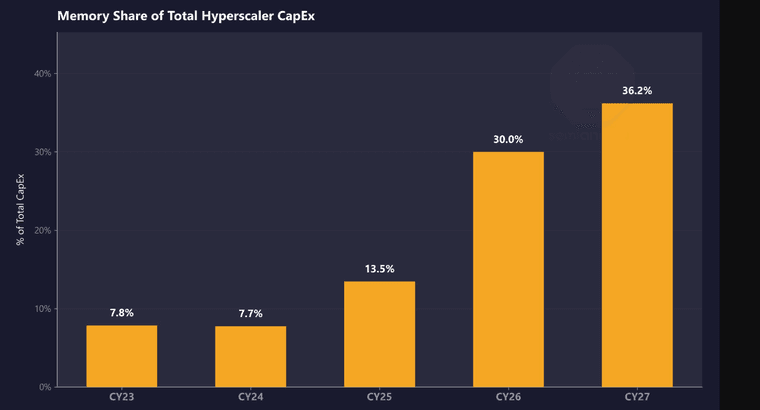

Quite incredible graphic showing 'memory' share of total Capex. It's gigantic. Recall we speculated some time ago that memory will be as important if not more important than the GPU. We need to pause and think about this for a moment. A $5M Rubin rack containing over $1M in memory. And the forecast is for 2027 to be even more. That GOOG Turbo algo sure killed the memory hype

-

And some guy …seeking Alpha reckons that Micron is a value trap ….dont buy the shares it’s worthless

-

There's always 'some guy' on the internet with an opinion.

")

The author compared the HBM market to 'Timmy's lemonade stand and some guy comes along with a lemon processing machine and 100Xs the supply'. I won't bother unpicking that analogy as it's moronically (tropic thunder).

All we need to know is management(who actually know what's going on) see blue sky as far as they could possibly see, are investing more(10s of billions) to meet the unmet demand they know they will not be able to meet. They think this will persist for years. They think existing 80%+ margins are the new norm. And the icing on the cake is the next 12 months will see min $100 and likely more EPS, it's not like this 300% growth comes with a high stock price, PEs in the 80-100 or more. It's 3.5. I like the math.

Further that article is factually wrong with the math. ROE stated at 50%(it's not), it's well over 100% and as a number-articles with a narrative always pluck/insert dubious figures with no basis and that's exactly what you have here. Lists the next years ROE, without any source or basis. I don't use ROE because it is deeply flawed. It's historical and the big one, it's an accounting concept not a business concept. It's taught in academic circles and imo useless in this case. EG if management paid out a huge dividend, Equity is reduced and the ROE looks far worse. But is the company valuation worse-of course not.

-

Given Samsungs +750% profit surge being all about memory, it's a reasonable assumption that Micron will move back over $400 today.

-

Analyst note today:

"Beyond Micron management’s statement that its 2026 HBM capacity is already sold out, the company’s HBM, DDR5, and LPDDR5 production capacity has now been fully reserved through 2027. We raise our target price to $825

With 2027 allocation now complete, Micron is currently in discussions with key customers regarding 2028 supply volumes and pricing terms."