Micron Technology

-

It was a Trig moment, calling Rodders 'AL'

-

Dan Ives(analyst) said today...The increasing demand and tight supply of memory for artificial intelligence infrastructure buildouts will prompt prices of some memory types to surge by more than 100%, according to Wedbush.

"Not surprisingly, pricing for memory continues to lift aggressively, with DRAM and NAND likely to see 1H (means first half 2026) pricing increases well into the triple digits from CQ4'25 levels, with gains for the former likely approaching 130% - 150% and the latter nearly as robust," said Wedbush analysts in a Monday investor report.

This should bode well for memory makers such as Micron Technology (MU), Seagate Technology (STX), and Western Digital (WDC).

"No one should be surprised by an improvement in memory," Wedbush said. "However, the magnitude of the spike highlights how much markets have continued to improve as Q1 has progressed and certainly fits our recent positive checks around memory and MU's robust results and guidance."

"And we believe, given both this backdrop as well as further shortfalls in supply vs. demand, that HDD vendors are looking to price their future contracts more aggressively than they have previously suggested," Wedbush noted.

-

The next 4 quarters look something like

$20

$25 range

$30 range

$35 rangeSafe to say that our speculated $100 TTM EPS is highly likely. NB analysts until 4 weeks ago pegged their Nrs at $56 at the high end and sub $40 at the low end. It is not just ASP driving the growth but obviously it helps significantly. Bit growth is around 25% annualised and this is all the industry can produce until at least 2028. The demand/supply imbalance will persist for years imo given 2 quarters ago Demand over supply was circa 60% and today it is closer to 80%-the gap is widening and that is why prices are rising.

Today MU 1 yr Fwd PE is 4 with a growth rate exceeding 100% (closer to 200%) and conservatively a 5 yr CAGR of 65%.

What I find very interesting is planned Capex in calendar 26, confirmed last Q was an aggressive $25B and today they've upped this to $35B and more next year-it's clear to me they see something the market is ignoring. And what it might see as a negative (Capex) I see as a positive.

The biggest miss imo is as the data centre goggles up all this memory we have nascent markets building momentum. The edge is where the real fun begins. Robotics and mobile devices(Robots and cars)-everthing that moves will proliferate once the 'AIs' are at stage where their use becomes ubiquitous-and it will within the next 1-2 years.

-

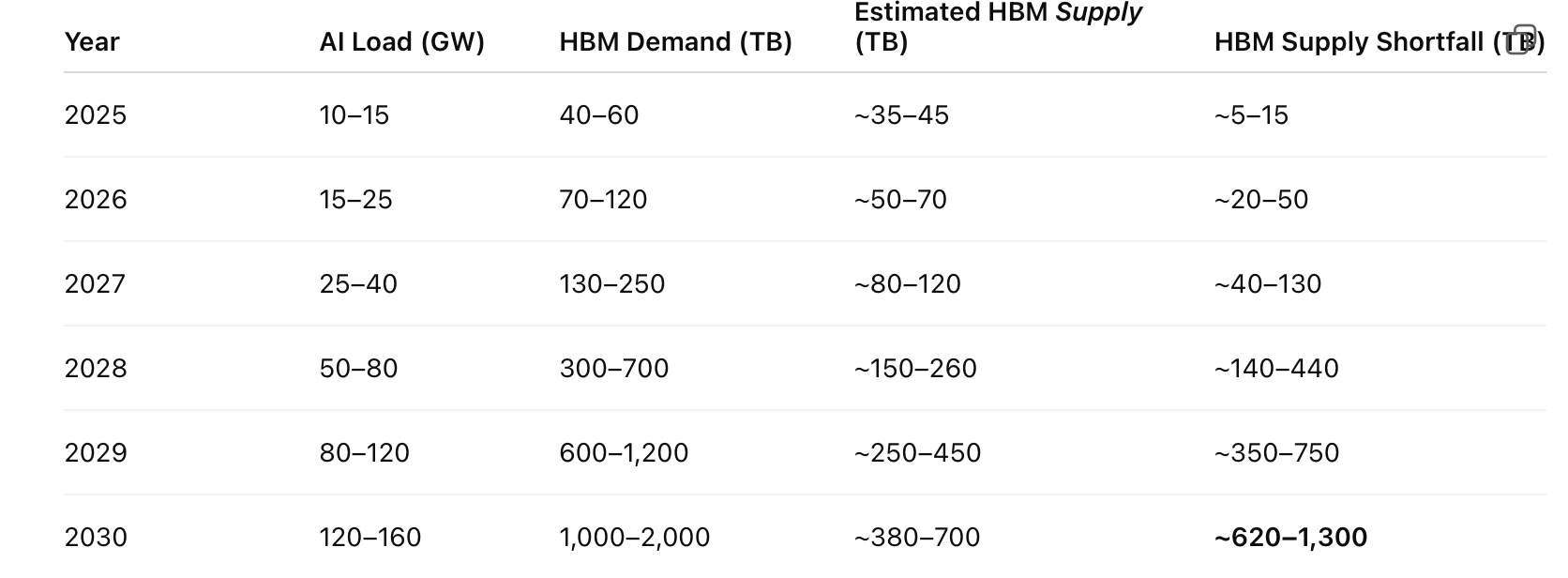

By 2030, edge AI is projected to dominate total memory demand, far surpassing datacenter use. Even with conservative assumptions, billions of devices running sophisticated AI locally could consume 5–7 EB(exobyytes) of high-bandwidth memory (5–7 million TB), compared with roughly 1 EB in datacenter. Autonomous vehicles alone (not just cars, drones robots, tablets, phones)—potentially 100 million units worldwide—could carry 32–48 GB HBM-equivalent per car, while industrial and service robots, numbering perhaps 50 million, might each need 24–32 GB.

Consumer devices like AR/VR headsets, tablets, and smart home devices add billions more, though individual HBM demand is smaller, collectively accounting for several exabytes.

Annual additions will be substantial: roughly 10–20 million cars and 5–10 million robots per year, each increment consuming hundreds of petabytes of high-speed memory. Even with edge memory adoption tempered by cheaper stacked DRAM and LPDDR alternatives, the rate of growth is staggering, exceeding the production scaling plans of current HBM fabs. I would use the term 'forever constrained'The wedge of demand is steep: memory requirements increase not just linearly with new devices but also with the growing sophistication of AI models, which push per-device memory higher. As a result, planned memory fabrication capacity is unlikely to keep up, creating a structural bottleneck for ubiquitous, high-performance edge AI. Which, if correct would drive prices up for years as demand continues to exceed supply.

This is my take. Whilst today the market worries about the memory party to be over soon and im thinking even MUs planned $200B expansion plans will not be enough. This plan covers 10 years. I will speculate now that by the end of next year this 200B plan becomes $400B or more.

-

Micron Technology’s decision today to repurchase up to $5.4B of its senior notes is a clear positive signal about its financial strength and discipline. Using cash rather than issuing stock shows the company is generating solid cash flow and prioritising long-term balance sheet health over short-term optics.

By reducing higher-interest debt in the 5–6% range, Micron effectively locks in a risk-free return and lowers future interest expenses, which will support margins over time.

-

Just seen a report re Google developing chips that need less memory ..

The report indicated that this was behind the drops in Micron this week -

Hi C,

It's an algorithm not a chip and it's a nothing-burger. It has no impact on memory requirements whatsoever and it shows you just how ignorant the participants in the market are.

Google’s “Turbo” narrative is intellectually lazy. The leap from “better AI efficiency” to “less memory demand” ignores how technology adoption actually works. Efficiency lowers costs, which expands usage—basic economics. Dumping Micron Technology on that headline assumes AI growth is fragile and linear, when it’s explosive and compounding. It’s a textbook case of headline-chasing algos and shallow thinking masquerading as insight. No serious analysis, no nuance—just reflexive selling. If this is the market’s level of reasoning, it’s not pricing risk; it’s broadcasting confusion.

And if you want to get technical....

First, the “post rack-scale GPU” reality: once you’re deploying clusters at that level, memory bandwidth and capacity (HBM, interconnect efficiency, etc.) are hard constraints, not optional luxuries.

Software improvements don’t remove that—they just let you push the hardware harder. That typically increases utilisation, not reduces demand.

Second, the token growth point is the killer. If total tokens processed have exploded ~2500×, then a 6× efficiency gain is statistical noise. You’re still looking at orders-of-magnitude net growth in compute and memory demand. The denominator is moving way faster than the numerator.

Third, these optimisations aren’t new. Google and others have been shipping incremental efficiency gains for years—compiler improvements, sparsity tricks, better routing, quantisation, etc. The so-called “Turbo” angle isn’t some step-function event; it’s part of a continuous curve.

So the sell-off in Micron Technology assumes:

efficiency gains suddenly matter more than demand growth

and that this time is different from every prior cycle

That’s a weak assumption. In practice, efficiency gains + exploding demand = more total infrastructure, not less.Micron is so worried it's just about to buy another plant and repurpose it( 4 million sq feet) to accelerate its roadmap. And customers are signing 5 year supply agreements, scrambling to secure their supply chain, including Google who is a major customer. Rather than listen to the FUD look at the evidence. The company can only supply 50% of orders and > 80% margins and that imbalance is getting worse. It also completely ignores the edge device market which will be orders of magnitude bigger than data centre.

It's like the Deep-Seek moment we dont need these GPUs...oh wait.

-

Thanks Adam ….as always appreciate your insights

-

and right on cue. Morgan Stanley today said ...

Morgan Stanley, in a client note reiterated their over weight rating and $520 price target on MU.

-

They must be on this Forum

-

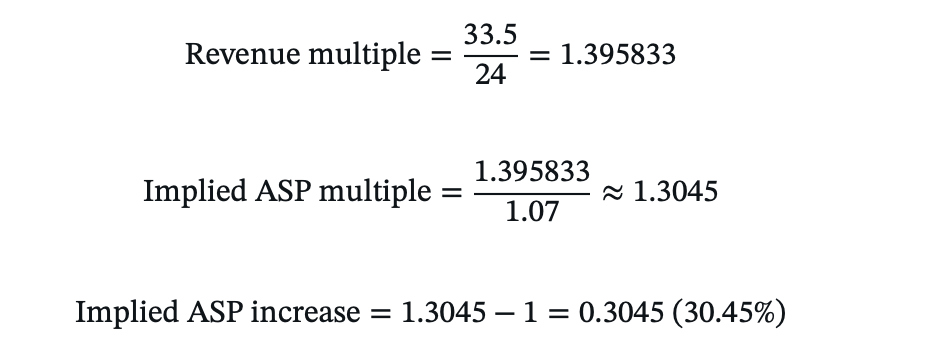

Micron’s “monster” Q3 guidance, issued in mid-March 2026, projected revenue of approximately $33.5 billion with an 81% gross margin. At the time, this was beyond strong. The guide is the strongest growth in corporate history-but it just got even better.

Analysts and consensus models likely incorporated more conservative server DRAM contract price assumptions of around 10–15% QoQ for Q2 2026 (April–June calendar, microns quarter 3 covers March through May). Why, because Trendforce provide market data on what customers are paying/bidding.

Yesterday TrendForce revisions have dramatically upgraded that outlook to roughly +45% QoQ for server DRAM prices. This meaningful positive surprise implies higher average selling prices (ASPs) than previously modelled, particularly as new contracts roll into Micron’s fiscal Q3/Q4 2026 and Q1 2027.The impact could be substantial: elevated server and HBM pricing would lift revenue beyond current forecasts while expanding already-record margins further, thanks to the favourable product mix and limited near-term supply growth. Operating expenses are largely fixed whether they deliver $33B or $40B for that matter.

Modelling that ASP change we are looking at $38B revenue and $25 eps. This is one quarter not a year with a stock now at $357!

Worst case scenario-prices stabilise, best case they keep rising for the next year. They aren't going to fall and will likely rise a bit more but if we model flat ASP and just look at MUs bit growth of 25% thats a base of $100 EPS for 12 months and a 25% growth rate going fwd. With a PE of about 3.

-

Official Nr's on memory for the April-June Q

Q2 2026

Quarter on Quarter(not annual changes) ASP-

PC DRAM prices: revised up from +10~15% to +40~45%

-

Server DRAM prices: revised up from +10~15% to +43~48% The big one

-

Mobile DRAM (LP5X) prices: revised up from +13~18% to +58~63%

-

eSSD prices: revised up from +15~20% to +68~73% The big one

-

TLC/QLC NAND prices: revised up from +15~20% to +60~65% The big one

-

Overall NAND Blended ASP: revised up from +18~23% to +70~75%

so when I said +45% above- it looks like it's actually a lot more-nice!

Looking at last Q, $24B and a $33.5B guide. We know bit growth is limited to +7% QoQ maybe a bit more but that is still a lot so to get to 33.5B we can infer the assumed ASP rise built into their model notwithstanding any change in mix.

Given prices are up a lot more than 30.45% a massive beat is a given. It wouldn't surprise me if they report close to $40B this quarter and $24-$25 eps. Last years Q3 revenue was $9.7B. $1.62 eps.

-

-

Micron taking a bit of a bloody nose again today ….

-

It's frustrating for sure, C. However it's the same pattern of behaviour with 'AI' at the moment-disbelief.

What you have here is the business and its management (at the coal face) taking new business, signing unprecedented 3-5 year supply deals, committing vast sums in Capex and now doubling down on that investment. Two camps, believers and non believers. There is also a lot of foul play and FUD.

Everyone is forgetting that GOOG themselves is one of the biggest 'memory' buyers and they have the biggest 2026 Capex ($175B)-they too are constrained by memory.I noticed yesterday that Nvidia is now trading at multiples below the S&P average yet its growth rate is the highest. When you look at the situation, holding stocks that are thriving but beaten down it's quite clear when the fear lifts we will see a profound correction.

I think the market is wrong and not just slightly so.

-

This is based on known committed data centre alone. It does not include edge cases. This additional annual GW (the only smart way to look at the build out). And yes 2025 was a big year but compare 15GW of built to 25 in 2026 and 40 in 2027.

Reiterating-algo's and compression make no difference to the HBM required at the server(hardware) level. It just makes inference cheaper. As it gets cheaper, consumption increases.

Shortage is measured is millions of TB. 2025 up to 50M TB shortage and growing to 1 billion TB shortage in 2030. Or looking at it another way 2026 demand is 120M TB but the shortage could approach 1B TB in 5 years. Even if wrong by a huge margin, demand exceeds supply. This is based on all Capex committed today-even if Capex increases next year and beyond, it will have minimal impact on the demand supply landscape to 2030 due to build duration.

-

I’m sure you’ve seen the note re Citi noting that DRAM spot prices have dropped by 6%. …. But they still give a higher price than today of $425 from $510

-

I have ;). Spot prices havnt fallen-oh 0.26%. Big firms hug the stock price. They never want to be an outlier. Im not aligned to 510 either

.

. -

These so called professional people etc …are never held accountable for what they write etc …