Micron Technology

-

'Since our earnings (where they had a Nvidia esq guide) our financial position has strengthened somewhat. I like this guy a lot

")

-

We are only meeting 50% of some customers memory needs-I liked this comment, 'we are sweating our assets to grow production'.

-

On the demand side-token generation is increasing, that is demanding more memory and storage, more of it and higher performance. In time the edge will become increasingly important (robotics). Agentic AI will place even higher demands. The market is very broad, very strong and getting stronger. We are toiling to get incremental bits out. Node transitions to supply additional bits until new Greenfield sites come on line.

Brilliant presentation and a shot in the arm

-

For those interested here are they key points from the investor conference:

Extraordinary business trajectory and strengthened outlook —

Since the last earnings call, Micron’s financial outlook has improved further, driven by robust demand outpacing supply significantly (both for Micron and the industry overall). The setup is described as the best competitive position in the company’s history(47 years) at an ideal time.

Sustained tight supply-demand balance —

Demand remains significantly higher than available supply, with tightness expected to persist beyond 2026. This creates a favourable pricing environment, contributing to the improved outlook (though specifics on price changes were not quantified).

Strong AI-driven demand across products —

AI advancements (larger models, longer context windows, intensive reasoning) are driving needs for higher-performance memory and storage. This includes proliferation of high-performance memory in data centre architectures, growth in server demand (from single digits to mid-teens percentages in 2025, with continuation expected), and spillover to edge devices (e.g., smartphones, PCs, future autonomous/robotics applications). Hyperscaler CapEx has surged dramatically (approaching USD 800 billion in 2026 vs. under USD 200 billion a few years ago). The key takeaway here being longer context windows, zero shot inference and next gen models having the ability to remember/retain content for 'years', all means more memory.

HBM leadership and progress —

Micron rebutted recent inaccurate reports by confirming it is already in high-volume production of HBM4, with customer shipments commenced and volumes ramping successfully in calendar Q1 2026 (a quarter ahead of prior guidance from the December earnings call). HBM4 delivers over 11 Gbps speeds,(it didn't escape me this is Nvidia's revised target) with yields on track and high confidence in performance, quality, and reliability. Calendar 2026 HBM supply is fully sold out, underscoring strong positioning in this high-value AI segment.

Supply constraints support pricing and margins —

Broad-based shortages affect large and smaller customers (some meeting only 50–67% of needs). Micron is maximising existing assets, ramping the 1-gamma node for incremental bits in 2026(more bits = more supply), and investing in greenfield capacity (new sites) (e.g., new DRAM fab in New York, NAND fab in Singapore with first wafers in H2 2028, Tongluo site acquisition in Taiwan for DRAM support closing in Q2 2026). HBM’s higher silicon intensity further tightens overall DRAM supply.

Progress on multiyear customer agreements —

Customers are seeking longer-term deals with firm commitments (beyond traditional quarterly negotiations) due to memory’s critical role in AI systems, supply assurance needs, and Micron’s technology leadership (e.g., 30% lower power in HBM3E vs. competition, LPDRAM enabling 60% power savings in servers, strong NAND read-to-watt performance). These provide Micron with better visibility and commitment as it invests heavily in capacity and R&D. How long before management signal 'sold out through 2027? Not long imo.Innovation and portfolio strength —

Micron emphasised value delivery through products like LPDRAM for server “warm tier” (with a recent white paper highlighting tripled content potential and major inference improvements) and leading NAND in data centre SSDs (gaining share in performance TLC and capacity QLC, reaching >USD 1 billion run rate). This positions the company well for tiered memory/storage architectures in AI systems.

Margin and financial positivity — Gross margins guided to 68%(up from mid 50s), with expectations for expansion in the current quarter (Q3). How high will Q2 be? 75?Cost control, volume absorption, mix benefits (premium tech flexibility-selling what is at a premium), and pricing support further upside. NAND outlook has improved with market tightening, though it is a smaller segment.

Sustainability confidence —

Both demand (AI evolution, including agentic activities and edge proliferation) and supply factors (limited/fast supply additions via greenfield over node transitions) support a prolonged positive cycle, unlike typical past cycles. Micron is investing disciplinedly while reassessing the market continuously.

Overall, the tone was highly optimistic, portraying Micron as a technology and manufacturing leader perfectly aligned with the AI boom, with limited near-term supply relief and strong pricing/margin tailwinds. This aligns with positive market reactions (e.g., stock gains post-conference on HBM4 clarity and tightness outlook).

Some context. Imo Micron will earn $150 per share in the next 24 months. Think about that. It's a staggering number. What's it worth? I would argue a lot more than $400. Of course the market thinks the music might stop in 18 months yet TSM and Nvidia are both planning for a 7 year super cycle build out and then a trillion dollar maintenance programme. Who's right? We don't have to believe Mehrotra in isolation, but collectively Huang, CC Wei. The A Team, a lot of credibility there and this is before you look at the roadmap. The memory needs and this is the DC not the edge, pc, phone etc etc(cars)

-

“I’m back.” — The Matrix Reloaded (2003) – Agent Smith

-

Micron leading the industry. Contributing $1B in 2025 last Q (one product)and expected to grow to $15B in 2026! That's some growth. Physically the size of a deck of cards, this SSD can cost upwards of $15,000 each!

The Micron 9650 NVMe SSD is a groundbreaking enterprise-grade storage solution, marking the world's first PCIe Gen6 data centre SSD now in mass production as of early 2026.

Leveraging Micron's advanced 9th-generation (G9) NAND technology, it delivers unparalleled performance with sequential read speeds up to 28 GB/s—double that of leading Gen5 drives— Available in PRO (read-intensive, up to 30.72 TB) and MAX (mixed-use, up to 25.6 TB) variants, it supports E1.S and E3.S form factors with air or liquid cooling options, offering superior energy efficiency (up to 67% better for certain workloads compared to prior generations).

This makes it ideal for AI training, inference, vector databases, and KV cache tiering in hyperscale data centres, where high throughput and low latency eliminate bottlenecks in GPU-fed architectures.This product is undeniably cutting-edge and a big deal in the industry. As the sole Gen6 SSD currently available, it positions Micron as a first-mover in premium AI-optimised storage amid explosive demand from cloud providers and AI infrastructure buildouts.

Early qualifications with major OEMs and data centre customers underscore its rapid traction, contributing to Micron's record data centre NAND momentum.Regarding revenue potential: Exact figures for the 9650 are not broken out publicly, as Micron reports aggregated NAND/SSD results. However, with data centre NAND already exceeding $1 billion quarterly in late 2025 and analysts forecasting full fiscal 2026 NAND revenue around $15 billion (up ~79% year-over-year), the 9650—as a flagship high-margin product—stands to drive meaningful growth. In calendar 2026 (the first full ramp year), it could contribute several billion USD in sales, assuming scaling to hundreds of thousands or low millions of units at premium pricing ($5,000–$15,000+ per high-capacity drive).

-

Renaissance Technologies-the most successful hedge fund in the world has increased its Micron holding by $500M to almost $1B in their latest 13F filing.

This is not just another fund. It’s one of the most data-driven, disciplined, and historically successful quantitative hedge funds ever built.

We are in good company.

-

What are your expectations for the next earnings call .

As always your information is great for us to read and digest -

I can only speculate because there are too many moving parts. But here are the previous couple of quarters. It started with Blackwell and is only getting more intense (memory hungry applications and special kinds at that). The Q1 fiscal is in 2025. Fiscal meaning the year end in this case 2026 October. It's not a case of wow big beat. Q2 due to be reported in March and guided last Q was expected to be $4.50-70. $8+! I thought it a misprint. Achieved because Micron operating expenses are largely fixed so any meaningful ASP increase is pure profit. Massive operating leverage. If it had been some 'dot com' stock it would have popped 150% on that beat. Beats like that happen very rarely.

Now to what they will report. Who knows but it's going to be a lot more than $8.42+/- 20c. The market expects a beat -9.50 or $10. But it has not rewarded the stock properly, yet imo. If I had to guess I expect well over $10 and probably $11+. Including this Q they have 3 left in the fiscal year and I expect over $50 and up to $60. If they have reported $4.78 that leaves somewhere between $45-$55 for 3 quarters so there is likely a $20 quarter coming in the next 7 months.

Bit growth is going to start really kicking in for Q3 and Q4 and into 2027.

1Y node DRAM and G9 for NAND doing all the heavy lifting before new Greenfield sites come on line.

It's possible the current price represents only 4X 2027 earnings. It's one to watch!

-

That’s great …appreciate the insight

-

A good way to gauge Microns future prospects if we assume they know what they are doing and can execute(they can) is to look at the landscape. Demand drivers. It doesnt matter if it's a GPU server or a TPU, Tranium , basics server. Today it's all about the cloud(the DC) but this will shift to the edge. And robots nor autonomous cars factor quite yet but clearly will. If we are constrained now my view is we can only get more constrained before we even hope to balance supply/demand. So, whilst the experts are debating what will happen in 1 year, im leaning towards a decade. As Ive mentioned before, listen to what TSM are doing and everything else cascades from there.

-

Some broadband facts that ive been pondering recently.

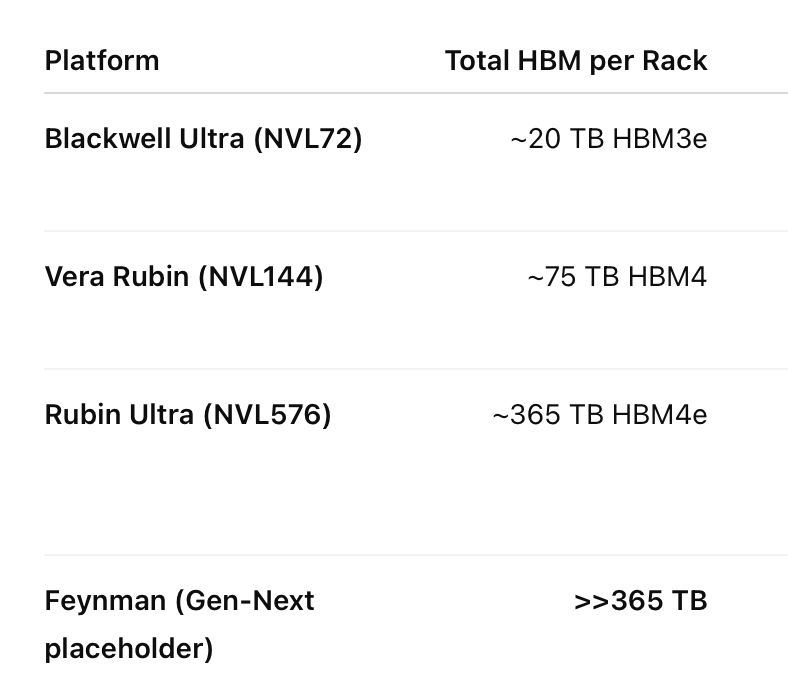

Over the next 7-10 years we are quite certain that if CC.Wei, Huang and Su are even remotely right, we will see rack scale growth of 50% per annum and each generation of rack consumes 20-25% more HBM. This is roughly 87% annual growth in demand. Global supply growth is limited to max 25% annually even with today's planned fab builds.

HBM3e and HBM4/4e demand is skyrocketing across server generations—Blackwell → Ultra → Feynman—driven by hyperscaler AI growth. GW-class deployments illustrate the scale: ~50% annual server growth and 20–25% memory density increase per node compounds into roughly 87–90% annual HBM capacity demand.

Supply simply can’t keep up. Even with aggressive greenfield fabs, wafer throughput, yield, and equipment constraints make matching demand impossible for many years, likely a decade. Prices are structurally set to rise.

Micron, Samsung, and Hynix dominate this niche, giving them extraordinary pricing power. HBM’s unique combination of bandwidth, latency, and power efficiency makes alternatives—DDR, GDDR, or CXL-attached memory—unable to replace it for high-performance compute. This creates a durable bottleneck, and the market rewards longevity; investors may expand multiples due to sustained, predictable growth, reinforcing upside. With growth rate certain come multiple expansion

In this environment, Micron could see a near-decade “renaissance”: multi-year high margins, rapid revenue growth, and favorable market perception. If demand persists and supply remains constrained, revenue could multiply several-fold, and with multiple expansion. The combination of exponential demand, scarce supply, and technological moat creates a structural HBM market imbalance that will shape AI server economics for the foreseeable future.

Even if my math is way off demand it's a fact that demand growth will exceed supply growth for a very long time. It's one to watch

-

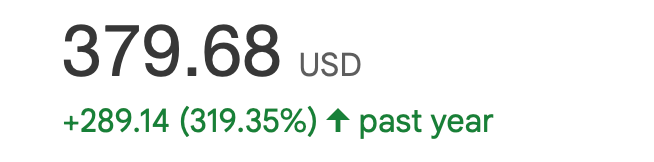

The fact it was $90 a year ago. It's as simple as the parabolic short duration being pre disposed to a bigger than avg move down when investors(I use that term loosely) get nervous. They report 2 weeks tomorrow.

The expectation is about $8.36 EPS. I think they'll deliver $11-earnings not expected for 3 more quarters. Fwd PE of about 7 with growth TTM 100%, at least 50% CAGR 5 years(PEG =0.14) OR you too can buy Crowdstrike with a Fwd PE of 60 and 15% growth (PEG=4). On this metric the stock is over 50X more expensive than Micron.

The expectation is about $8.36 EPS. I think they'll deliver $11-earnings not expected for 3 more quarters. Fwd PE of about 7 with growth TTM 100%, at least 50% CAGR 5 years(PEG =0.14) OR you too can buy Crowdstrike with a Fwd PE of 60 and 15% growth (PEG=4). On this metric the stock is over 50X more expensive than Micron.If you look at Micron it traded sideways from feb through May moved to $120 sold offa. bit (what happened), well it got stronger but people sold, thinking it was done and all stocks encounter selling at new levels because that's what people do. The problem is those same people just look at a price and make a decision. It was only 10 months ago that Nvidia fell from $125 to $89 on nothing but great news and 2 days later it was $115 over 25% in 2 days. We have seen this sort of thing countless times-it's human nature. When stressed some people do foolish things and more rational investors take advantage of the situation.

The only risk for Micron is they fail to execute on their roadmap and 50 years experience suggests that risk is tiny. Demand is growing 70% per annum for their products(lets call it 50%) and is expected to be the same for at least 5 years and probably 7+ (so says people I trust Wei/Huang). Bit growth(supply) can not keep up and will not because you can not magic up a fab in months. It take years, so it is obvious the imbalance will persist for years and prices for memory will keep rising. I say obvious, obvious to me.

The earliest time frame for some sort of balanced supply.demand imo is 2029/30

What you see with a company like Micron, is the old classic 'but it's risen 300% in a year' it cant do it again or it must be time to sell. I would say, tell me why you think that. The price appreciate is influencing ones decision making when in fact it's not of much relevance at all other than some thinking(?) they can cash in and rotate into something else. Good luck with that when the evidence strongly supports continued material undervaluation. Often the best investment is the one you already hold, and personally I like to get overly familiar with my holdings.

All I can say is, in all history companies with 50% annual growth and PEs below 10 don't exist. So on that basis alone I am very happy holding and waiting. And given we paid circa 1X next years earnings, maybe 1.5, we have a comfortable margin of safety.

-

If you believe nvidia will sell more racks next year than this year and Vera Rubin uses much more than blackwell. A top tier blackwell rack uses 192GB of memory, a Vera Rubin rack uses 300GB+ and Feyman will use > 500GB. And more racks will be sold so demand is:

TrendForce's 70% YoY demand growth in 2026; Goldman Sachs' 77% in 2026 and 68% in 2027), demand is indeed "a lot higher" supply-focused estimates—potentially 70-100% YoY bit growth (demand) through 2027, driven by GPUs (NVIDIA/AMD) and ASICs (e.g., Google TPUs, custom chips). Bit growth(supply) is estimated 35% in 26, 50% in 27 and 45% in 28. That is a very big imbalance which can only mean prices go up and there is a fight over who gets the silicon

The racks will get built but someone is going to be left without any supply and it won't be Nvidia imo because they have all the money to advance purchase whatever they need. AMD don't.

I've alluded to it before-HBM is the most critical component and the most scarce. I won't say what I think the stock is worth but I think a PE of 25 is not unreasonable, I also think the market is under estimating the EPS figure materially. Only months ago the experts thought it would earn $17 in 2026 total and it's closer to $50 this year and $75+ (maybe much more in 27).

-

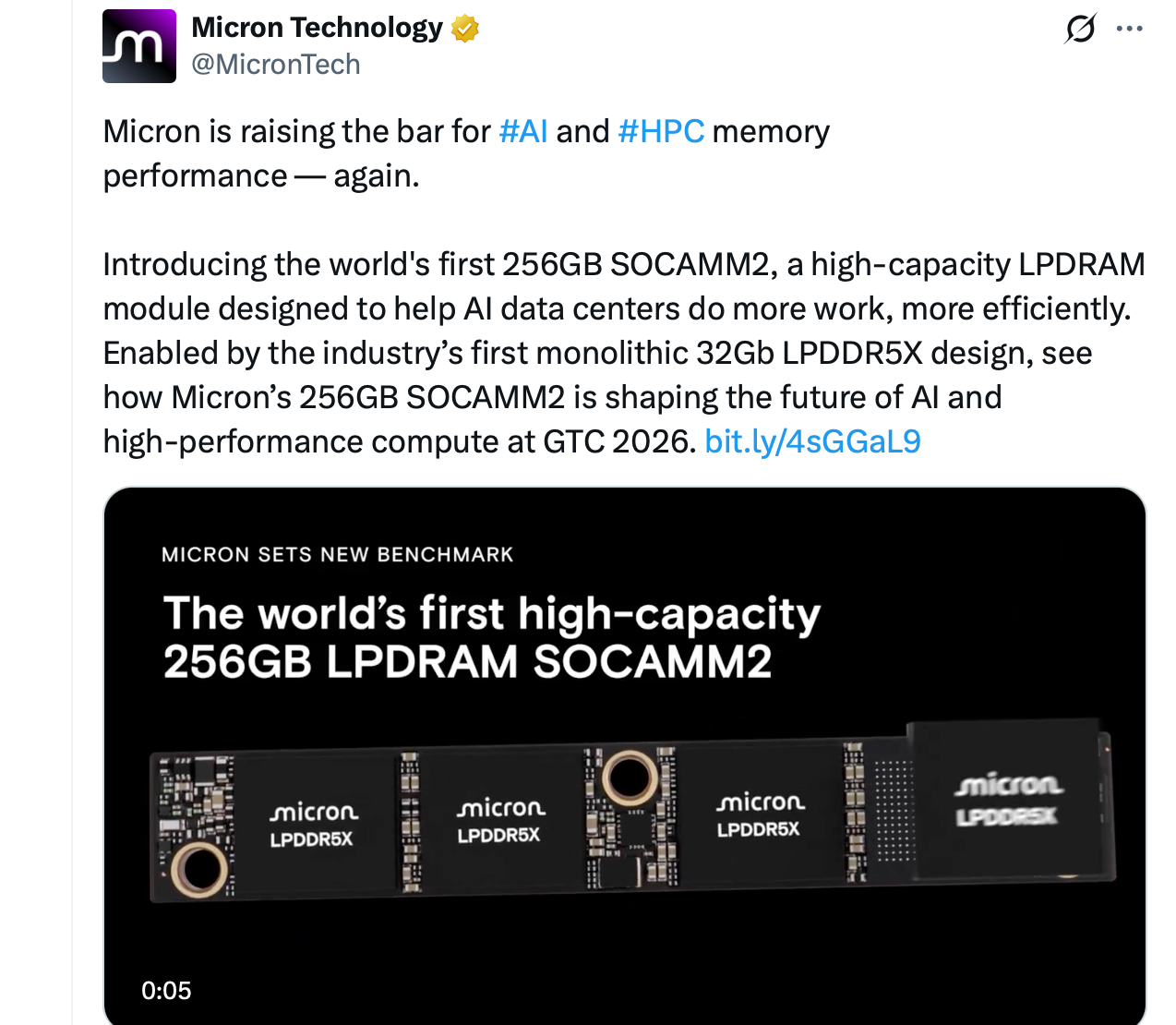

And just in. A new product and worth double digit billions-every one sold

-

What a difference a day makes-almost back. Must have read my post

-

@Adam-Kay said in Micron Technology:

What a difference a day makes-almost back. Must have read my post

I don't think I could ask for a better response to my eMail of yesterday!

Thanks for the explanation, and for tweaking the share price up as you did. (

)

) -

Micron Technology received two bullish analyst updates today, reinforcing positive sentiment around the memory chip cycle.

Citigroup, led by analyst Atif Malik, maintained a Buy rating and raised its price target to $430 from $385. The firm expects continued strength in memory pricing, driven largely by accelerating demand for AI infrastructure.

Meanwhile Susquehanna, through analyst Mehdi Hosseini, reiterated a Positive rating and lifted its price target sharply to $525 from $345 — a significant increase reflecting stronger long-term expectations for memory demand.

Analysts broadly believe the AI boom is tightening supply of advanced memory such as high-bandwidth memory (HBM), which is essential for training and running large AI models. This demand is supporting forecasts for rising DRAM prices over the next year.