Micron Technology

-

Micron hits an all time high today on the back of Citi analyst Buy opinion. Are we surprised-No, we saw this coming 6 months ago. The only surprise is their target of $230 puts their multiple on 10. I think it deserves a lot more than 10.

From the client note:Micron Technology shares rose +6.5% to $204 after Citi raised its price target from $200 to $240, while maintaining a Buy rating.

Key points from Citi analyst Christopher Danely:

Believes DRAM demand will be “unprecedented” owing to AI growth.

Expects DRAM to secure long-term contracts within the AI supply chain — similar to NVIDIA (NVDA), AMD, and Broadcom (AVGO).

Predicts higher and more sustainable DRAM pricing, enabling Micron’s gross margins to return to around 60%, with peak earnings per share (EPS) above $23 (nearly double the previous high of $12.26).

Updated financial forecasts:

FY2026 revenue: $62.5 billion (up from $56 billion)

FY2026 EPS: $21.05 (up from $16.93)

Estimates for FY2027 and FY2028 were also raised.

Context:

The optimism reflects a growing sentiment in the market that Micron will be a major beneficiary of the AI hardware boom, not just GPU manufacturers, as memory demand surges to support AI model training and inference workloads. -

MU management commented today that constraints will persist despite building material capacity.

An interesting fact. HBM memory is the largest cost component when looking at a GPU BOM (Bill of materials). Everything is on target in regards HBM4 and Microns solutions are the most power efficient in the industry.

Still trading at a PE of 10!

The stock hit an all time high today of $214 and change.

Looks like another beat and raise coming. -

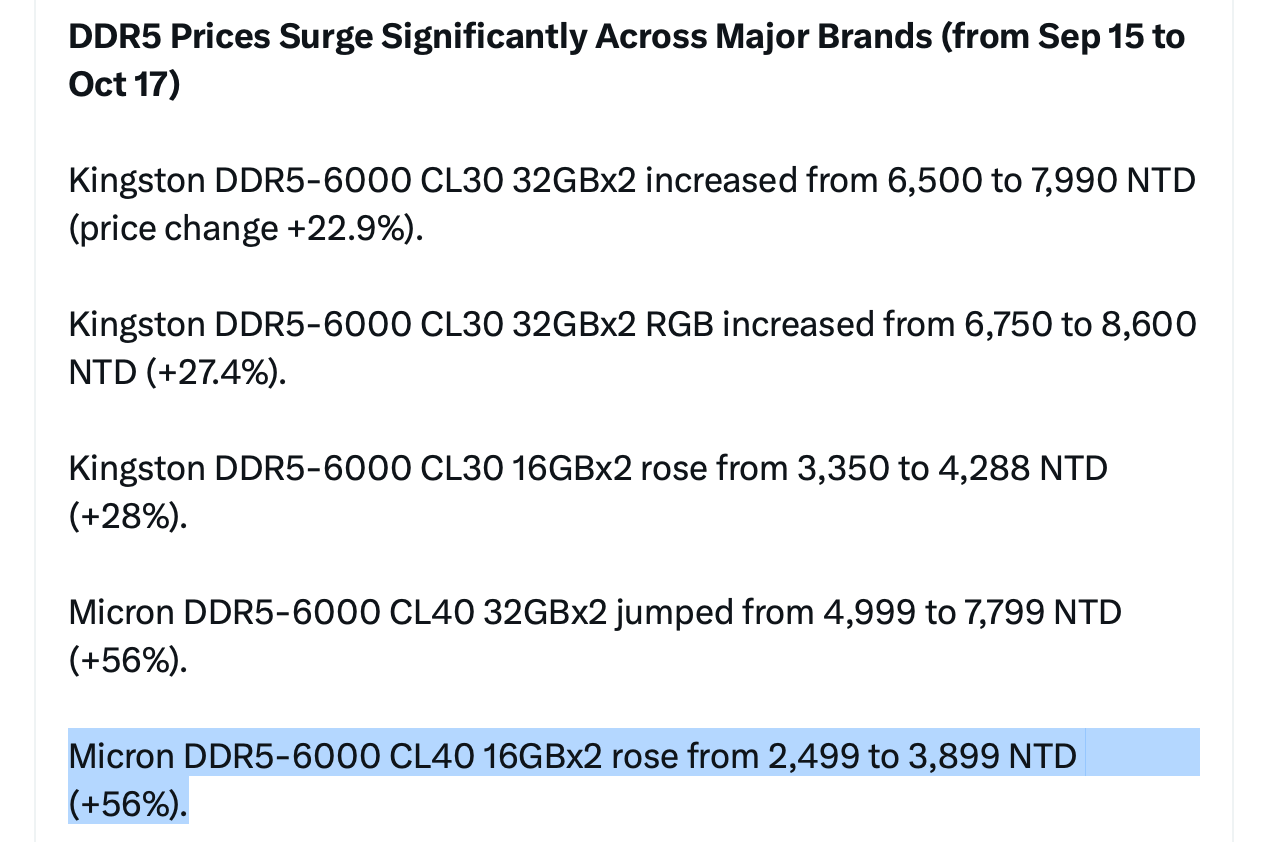

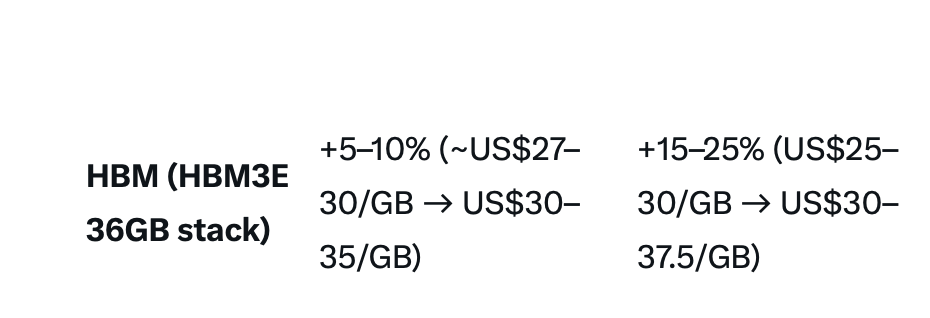

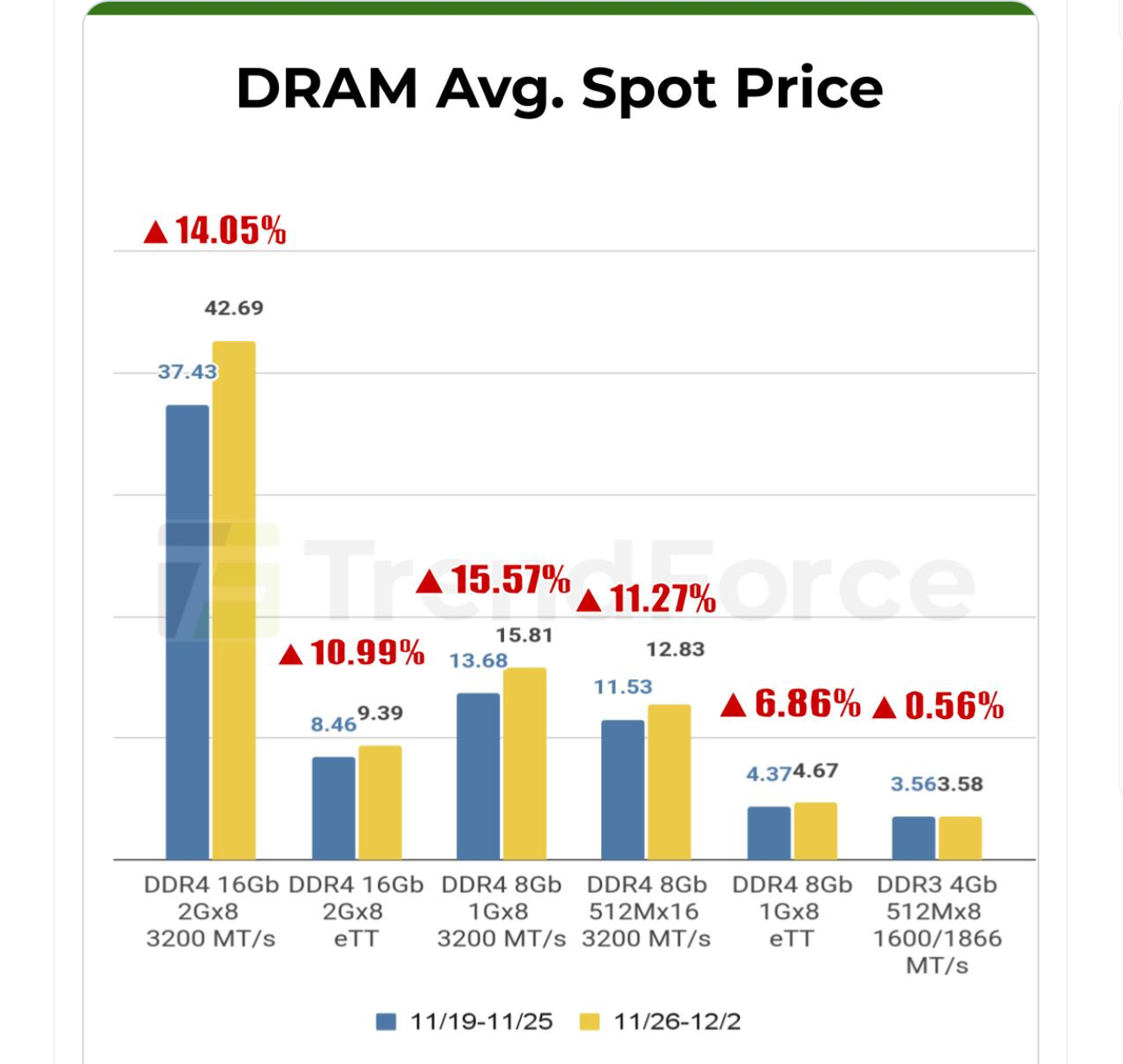

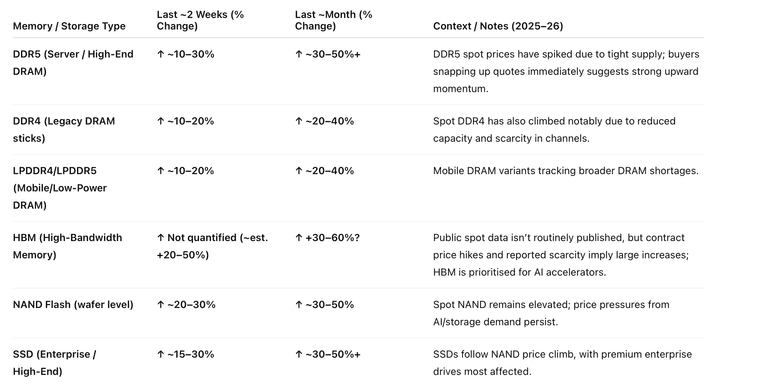

some monthly memory spot price info:

Critical weekly and monthly price changes AI HBM

Setting up another beat and raise.

-

Micron surged > 8% today to an ATH, spurred on by reports that a competitor has increased their HBM4 prices by 50% over HBM3. HBM4 will debut in the new Rubin racks scheduled for release early next year(ish) and Micron is currently negotiating prices on this bleeding edge tech.

It's a great example to reference the previous post about yesterday being painful and was it the catalyst for a correction. Micron fell 6% yesterday on zero news.

-

Samsung raises prices of memory chips by up to 60% amid supply shortage

Micron pops.

-

Micron released statement 'Winning':

sold out until 2027

Ahead of the competition in speed due to patented IP

Brilliant

Call out Taiwan for spreading FUD -

Good for Micron - looking for $16+ EPS next year

")

PC giants Lenovo, Dell and HP all warned the AI boom is using up memory chips, leading to tight global supplies next year, media report, citing Lenovo’s CFO saying the cost surge is “unprecedented” and confirming Lenovo is stockpiling memory chips, while Dell’s COO said he’s never seen memory costs “escalate at this pace” and HP’s CEO said the 2nd half of next year will be “particularly challenging” and HP will raise PC prices if necessary. The three PC giants all held quarterly earnings conferences recently

-

Bodes well for Micron

-

What are the thoughts on the upcoming earnings report

-

They will beat and raise. The company has a captive market and the wind at its back. What I see(and saw when we invested) is a secular shift in their key memory segments. Next year we are looking at $20 eps. It's multiple is very low and it should rerate when the shift is confirmed.

-

A lot to be said about this result and its wider positive flow on effect. But for now:

Micron Technology has just delivered an absolutely stellar fiscal Q1 2026 performance, shattering records and fuelling explosive growth driven by insatiable AI demand.

The company posted record-breaking revenue of $13.64 billion, a massive leap from $8.71 billion in the same quarter last year, whilst non-GAAP earnings per share soared to $4.78, trouncing analyst consensus of around $3.95.

But the real showstopper? Micron's jaw-dropping Q2 guidance: revenue guided to approximately $18.7 billion (± $400 million) – that's a staggering nearly 32% above the Wall Street consensus of about $14.2 billion – with adjusted EPS at $8.42 (± $0.20), almost double what analysts were expecting. Think about that. The expected guide was $4.xx and they said 'hold my beer-how about $8 bucks .Gross margins are projected to hit an astonishing 68% which is 30 whole points higher than last year, underscoring phenomenal pricing power in HBM and DRAM amid tight supply.

This is a proper drop-the-mic moment for Micron: HBM supply sold out for all of 2026 (including cutting-edge HBM4), data centre revenue at all-time highs, and CEO Sanjay Mehrotra signalling continued strength through fiscal 2026 on booming AI infrastructure spend. He also said demand is so great that the TAM, thought to be 100b by 2030 will now be that big by 2028. Now think about what that means for the wider GPU, rack scale demand cf the noise. Happy days.

-

Nice summary to get some perspective on just how big these results and this is a great set up for 2026 across the board.

Micron just delivered a gross margin of 56.8%, up from 45.7% last quarter, and is guiding to 68% next quarter, with further expansion expected in FY26.

For the quarter, management reported gross margin expansion of 1,110 basis points to 56.8% and is guiding to 68% next quarter—another 1,120 basis points of improvement.What Morgan Stanley is saying:

“This earnings result is the biggest surprise in U.S. semiconductor history, excluding Nvidia.”

Translation:

Micron’s earnings beat was exceptional, on a scale rarely seen in semiconductors.

Only Nvidia’s AI-driven blowouts over the past two years were larger.

Morgan Stanley is explicitly putting Nvidia in its own historical category.

This wording is deliberate. Analysts do not use phrases like “biggest in history” lightly.

Why Micron’s blowout matters for Nvidia (and not negatively)

Micron’s results confirm three structural tailwinds that directly support Nvidia:- AI memory demand is real and accelerating

HBM (high-bandwidth memory) demand is surging.

Every Nvidia GPU requires large amounts of HBM.

Strong Micron results mean Nvidia’s supply chain is tightening, not weakening.

GPUs do not ship without memory. Micron just confirmed the constraint is supply, not inventory. To address that the company is going 'further and faster' re it's fab build out and have committed $20B - Data-centre capex is expanding, not peaking

Micron guided to multiple quarters of sustained strength.

That implies hyperscalers are still increasing spend.

Nvidia remains the primary beneficiary of that capex.

This directly undermines the “AI digestion” or “capex pause” narrative—again. - Pricing power is returning across the stack

Micron demonstrated both margin expansion and pricing leverage.

When upstream suppliers regain pricing power, it usually means:

– Customers are less price-sensitive

– Demand urgency outweighs cost concerns

That is exactly the environment in which Nvidia performs best.

- AI memory demand is real and accelerating

-

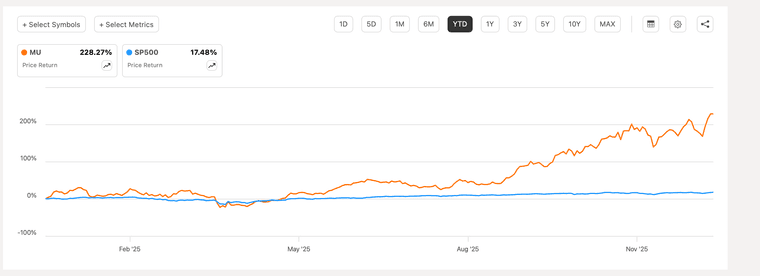

And the winner for the Year goes to: MICRON

And given its 1 yr Fwd PE is a mere 7 (base on $40 eps), it's still looking very cheap.

-

I would say:

I think Nvidia's stock price has treaded water for the past 6 months, all the while getting stronger. The doom merchants have tried every tactic to drive the price down, from fake stories about supply, to blatant lies about their superiority(re AMD and Asics), it failed. The company is at the centre of everything technology and is years ahead of its closest competitor. There are 39 analysts 'following' the company. Their average target price is $259 and the top price target is $352. Whilst I don't put much stock into what analysts have to say I do think the company is worth considerably more than today's price and 2026 is when we might see a break out.

As to Micron, we still haven't seen an expansion of their multiple, in fact it's fallen-it wasn't that long ago(2 months) that wall street was expecting $22 eps next year and now it's $40! The average target is $300 and the top target is $500. And at $500 its PE would be 12.5, so I think there is scope for plenty more upside. The market still thinks the business is cyclical, which it is to a point but the changes of late are structural/secular and Micron imo will continue to grow their business for many, many years.

-

Some spot price updates. Memory prices are up strongly.

This is a great environment for Micron, full stop.

Memory pricing is rising across DRAM, HBM, and NAND at the same time that AI demand is structurally stronger than past cycles. That combination is rare. Supply is tight, not just because demand is high, but because manufacturers are disciplined and prioritising high-margin products.Micron directly benefits from that discipline through higher ASPs, better mix, and operating leverage. AI servers are memory-hungry, and Micron is selling into the exact parts of the stack where customers care more about availability and performance than price.

That translates into real pricing power, not promotional volume. Unlike previous upcycles driven by PCs or phones, this one is anchored in data centre capex, which is larger, longer-lived, and stickier. Margins expand faster than costs, inventories remain lean, and earnings rebound strongly.

-

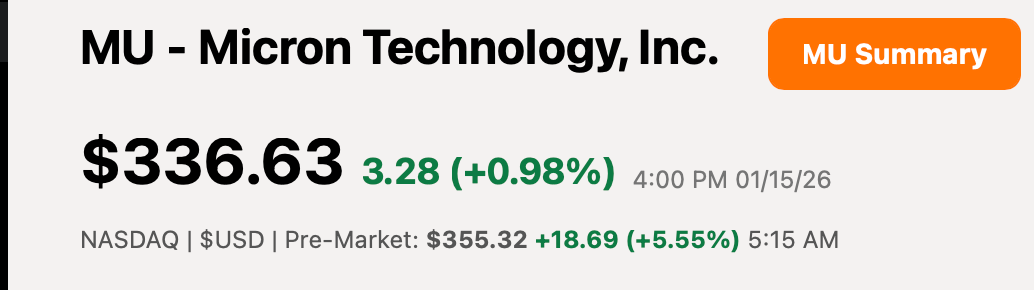

Insiders sell for all sorts of reasons but buying at ALT and with conviction sends a much stronger message.

—Shares rose after the company disclosed that its director, Teyin Liu, bought 23.2K shares of common stock in a total transaction size of $7.8M. The purchases were made at prices ranging from $336.63 to $337.50 per share.

-

Micron will buy Powerchip’s Tongluo fab in Taiwan for US$1.8 billion, giving it cleanroom space of 300,000 square feet in a 12-inch (300mm) fab, to boost capacity amid growing global memory chip demand, Micron said. The firms inked a letter of intent and will close the deal by the 2nd quarter this year, and Micron expects the acquisition to contribute meaningful DRAM output in 2nd half-2027

-

Investing in the future

Today, Micron broke ground on our $100 billion leading‑edge memory manufacturing complex in Onondaga County, NY! With up to 4 fabs, it will be the largest U.S. semiconductor facility, generating 50,000 jobs in New York.

Made possible by strong partnership across government, industry, academia, and our local community, this project will be home to the most advanced memory manufacturing in the world