Nvidia News

-

Abridged earnings call highlights and points to note.

Record financial performance: Revenue reached $68 billion in Q4 (+73% year-on-year), with record operating income and free cash flow. Full-year data centre revenue was $194 billion (+68%). Free cash flow totalled $97 billion for fiscal 2026 (period ending jan 2026)

Data centre dominance: Q4 data centre revenue was $62 billion (+75% YoY, +22% sequentially), driven by strong demand for the Blackwell architecture and Blackwell Ultra ramp. Nearly 9 gigawatts of Blackwell infrastructure are deployed. Note AMD crowing about 6GW over 5 years with Meta. Nvidia will deploy > 20GW this year alone.

Sustained growth outlook: Q1 revenue is expected to be $78 billion ±2%, mainly from data centres. (I think I stated 74 early but it's +$10B without china-aligns with our expectation of +$10B each Q). Sequential revenue growth is expected throughout calendar 2026, with visibility into 2027. No China data centre compute revenue is assumed. Looks like our 80/90/100/110 prediction aligns. And could be low. Translates TTM fwd of $380M and earnings of $220B over the next 12 months. Soon approaching twice the earnings of the worlds second most profitable company. Think about that!

Networking surge: Networking generated $11 billion in Q4 (+3.5x YoY which is 250%). Nvidia is now the biggest network company in the world. Full-year networking revenue exceeded $31 billion (over 10x since the Mellanox acquisition). They paid buttons for Mellanox-what an acquisition. NVLink, Spectrum-X Ethernet and InfiniBand adoption hit record levels.

Performance leadership**: GB300 NVL72 delivers up to 50x performance per watt and 35x lower cost per token versus Hopper.** Continuous CUDA optimisation improved GB200 NVL72 performance by up to 5x in four months. NVIDIA positions itself as delivering the lowest cost per token. Right there is why they are Nr1. Monetising AI is ALL about token generation at lowest cost. AMD can't even match Hopper today! Asics, TPU are not even close.

AI demand inflection: Agentic AI has reached a turning point. Inference equals revenue, as token generation drives customer monetisation. Hyperscaler 2026 CapEx expectations are approaching $700 billion, up nearly $120 billion since the start of the year.

Sovereign AI expansion: Sovereign AI revenue more than tripled YoY to over $30 billion, led by Canada, France, the Netherlands, Singapore and the UK. China revenue remains uncertain despite limited H200 approvals. NB- nice to have it back but irrelevant for the next year or so. Ignore the noise. I do think it will get resolved. I don't buy the 'China might catch up' They could have very competitive models but who is going to buy it. Not the West. Would you rent a Chinese AI agent? Will any S&P companies use Chinese AI. So imo it's an irrelevance. China will consume it, which is fine. And it would appear Deepseek is using Blackwell anyway so no china sales is not the case. The Wall Street Journal claims Deepseek is a fraud-all their work is stolen (distilled) from OpenAI et al, big surprise.

New platform – Rubin: Unveiled at CES, Rubin includes six new chips (Vera CPU, Rubin GPU and new networking components). It will train models using one-quarter the GPUs and reduce inference token costs by up to 10x versus Blackwell. Production shipments begin in H2. The math says Rubin will be 500X lower token cost than Hopper. Just incredible.

Gaming and other segments:

Gaming revenue: $3.7 billion (+47% YoY), though supply constraints are expected to weigh on Q1 and beyond.Professional Visualisation: $1.3 billion (+159% YoY).

Automotive: $604 million (+6% YoY), driven by self-driving demand. Physical AI contributed over $6 billion in FY2026.Gross margins remain strong: Q4 GAAP gross margin was 75%. Full-year margins are expected in the mid-70s. Management argues sustainability depends on delivering generational leaps in performance per watt and per dollar. And precisely what they are doing. Every year, a new leap fwd.

Capital allocation: Returned $41 billion (43% of free cash flow) to shareholders via buybacks and dividends, while increasing inventory and purchase commitments to secure future supply.

Strategic ecosystem expansion: Deepened partnerships with OpenAI, Meta and Anthropic (including a $10 billion investment in Anthropic). NVIDIA emphasises CUDA ecosystem breadth, full-stack AI infrastructure, and extreme co-design as competitive advantages.Long-term thesis: Computing has shifted to AI token generation. “Compute equals revenue.” Agentic AI is the current growth driver; physical AI (robotics, manufacturing, autonomous systems) is the next major wave. NB-we know this is going to be huge. Data centre CapEx could reach multi-trillion USD levels by 2030 if AI adoption continues accelerating. The question is now, when not if Nvidia generate $1T in a fiscal year.

-

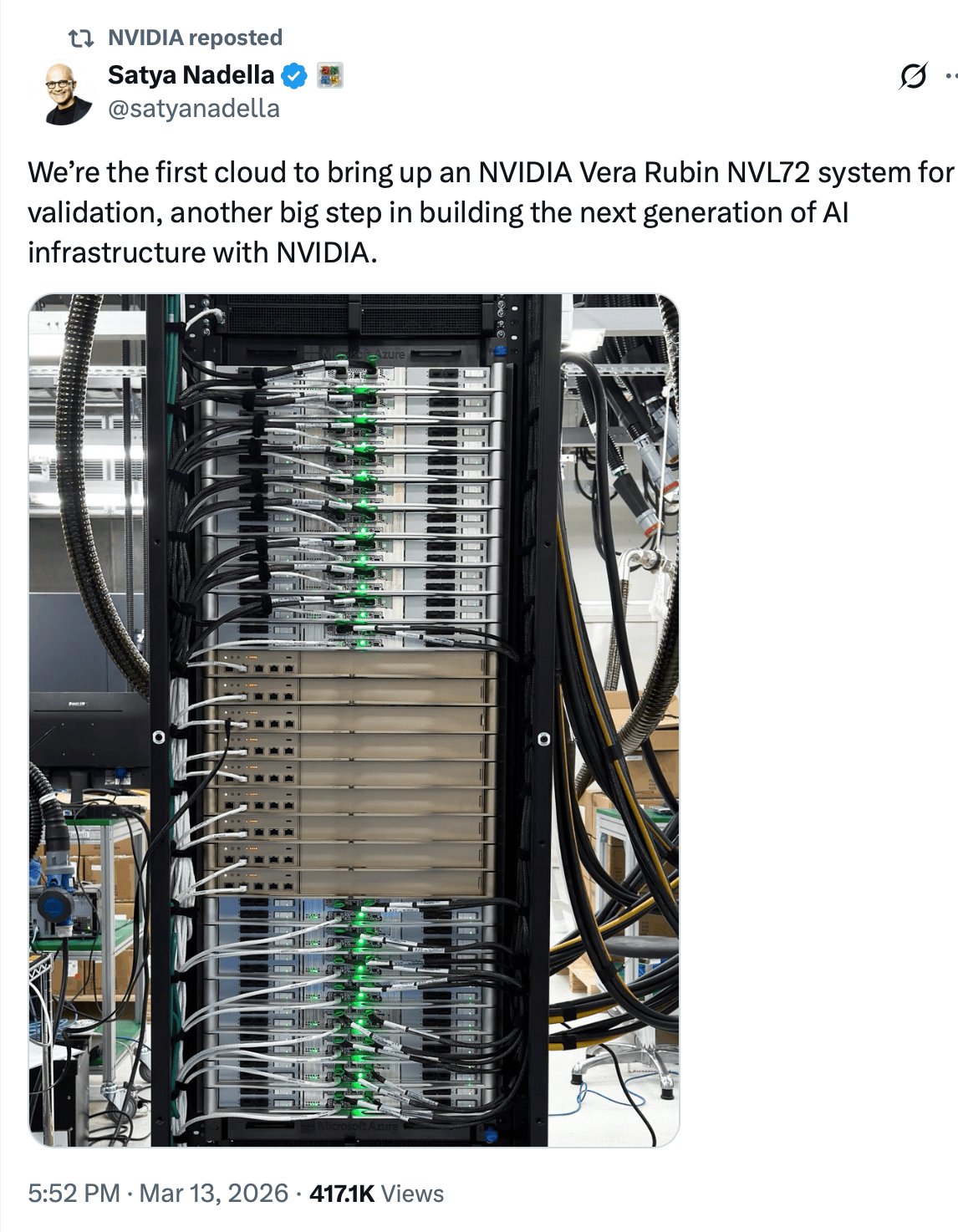

Validation Milestone

Microsoft Azure became the first major cloud provider to power on and begin validating a Vera Rubin NVL72 rack (announced by Satya Nadella on 13 March 2026). This is a significant engineering win: the full rack (72 Rubin GPUs + 36 Vera CPUs, NVLink-6 fabric, liquid cooling) is integrated and undergoing qualification in Azure datacentres. It positions Microsoft ahead for early deployments, with broad availability still guided for the second half of 2026 (H2 2026, i.e., July–December).Rack Cost Estimate

A Vera Rubin NVL72 rack is likely priced in the $3.5 million to $5 million range (most analyst estimates cluster around $3–4 million, with some supply-chain views up to $5–5.7 million). This represents a premium over Blackwell GB200/GB300 NVL72 racks (around $3 million).

The uplift stems from advanced components: HBM4 memory, denser NVLink-6, Vera CPUs, and enhanced liquid cooling (cooling alone rises from ~$50,000 on Blackwell to ~$55–56,000 on Rubin).

NVIDIA doesn't publish official prices, but the economics favour rapid payback through vastly higher efficiency.Performance Improvements

Rubin delivers massive leaps, especially for inference (the dominant AI workload now): Vs. Blackwell (GB200/GB300 NVL72): Up to 5x higher inference performance per rack (e.g., 3.6 exaFLOPS FP4 vs. ~0.7–0.8 exaFLOPS equivalents). Per-GPU gains include ~50 PFLOPS NVFP4 inference (5x vs. Blackwell), plus better power efficiency and features for agentic/long-context models. Training MoE models needs ~4x fewer GPUs.Cost per Token Shrinking

This is where Rubin crushes economics—driving the cost of intelligence off a cliff for inference-heavy workloads (e.g., agentic AI, reasoning, MoE models): Vs. Blackwell: NVIDIA states 10x lower cost per million tokens (official claim on specific MoE/reasoning benchmarks like Kimi-K2-Thinking).

Vs. Hopper: Blackwell cut costs by up to 10x (real deployments saw drops from $0.20/million tokens to $0.05 or lower with NVFP4). Rubin stacks another 10x reduction → potentially 100x lower effective cost per token over Hopper in optimised cases.

Providers already realised 4x–10x drops moving Hopper → Blackwell (e.g., 20¢ → 5¢/million tokens for MoE). Rubin positions sub-1¢/million at scale once volumes ramp in H2 2026.

The upfront rack cost ($4M average) is offset by far more useful compute per dollar, lower power/token, and fewer units needed—making massive AI scaling dramatically cheaper.In short: Validation is a big early win for Microsoft/NVIDIA, racks cost a hefty $3.5–5M each (premium justified), performance jumps 5x over Blackwell (20–25x over Hopper), and token costs plummet another 10x vs. Blackwell—paving the way for agentic AI at unprecedented scale and affordability.

-

Nvidia now hold approved Purchase Orders from China customers and intend to restart H200 production. Quote from Jensen Huang. Interesting as the company holds 400K chips in stock so one can only assume the orders are for more than this. Analysts expect teh Chinese market to be worth at least $25B so another nice earner which is not accounted for, presently.

-

Shares in Corning jumped more than 14% in premarket trading after it announced a major long-term partnership with Nvidia aimed at massively scaling optical connectivity. The deal is pretty significant, with plans to boost capacity tenfold, which says a lot about just how fast demand for AI infrastructure is growing.

As part of the agreement, the companies will build three new manufacturing plants in the US, creating over 3,000 well-paid jobs. Corning will also expand its fibre production capacity by more than 50%, helping meet the needs of hyperscale data centres that rely on fast, efficient connectivity to run Nvidia’s advanced computing systems.

Jensen Huang framed the move as part of a broader shift, calling AI the biggest infrastructure buildout of our time. Meanwhile, Corning boss Wendell Weeks highlighted the manufacturing angle, stressing that this isn’t just about tech innovation but also about rebuilding industrial capacity.

In simplistic terms-Optical fibre sends data as light, allowing far higher bandwidth and much lower signal loss than copper. It carries more data over longer distances with minimal interference. Latency is lower in practice, and scaling is easier. Copper is fine short-range, but optics handles massive, high-speed data loads far better.

-

A post from the past-Nov 2025-we speculated that their revenue tempo QoQ would be close to +$10B (and +$15 when Rubin starts ramping H2)

Last Q $68B (our bull case was $70B)

Citi today re Q1

"We model ~$1.4B upside in the Apr-Q with sales reaching $80B versus the Street's $78.6B on stronger-than-expected B300 ramp," Citi analysts said in a Tuesday investor note. "Looking into the Jul-Q, we expect an 11% Q/Q sales uptick to $89B versus the Street's $87B on continued ramp of B300 as reflected by the faster-than-expected 1.6T transceiver shipments."Nvidia is trading at a PE of 22 ish and a PEG of 0.5. AMD is trading at a PE of 60 and a PEG of 2. Imo, one is undervalued and one is over valued.

-

Just my opinion but I do expect some concrete movement on China's ability to use American silicon, coming out of the trade summit-today is the second day of negotiations.

-

Worth a watch if you have X. https://x.com/elonmusk/status/2056179413901877551?s=20

And for context, Citadel is one of the world’s largest and most influential financial firms. Its hedge fund business manages more than US$60 billion in assets under management, making it among the biggest alternative investment managers globally.

-

Nvidia report tonight. My call:

$80B+ and $45B net income which equates circa $1.80 EPS. I think the guide will be close to $90B for next quarter(May through July).

We will receive updates on Rubin/Vera Rubin

-

Those are normal operational numbers. Non gaap including exceptional etc was 58b. There was a $15b revaluation (upwards) which would be related to one of their investments-listed I would think, prob Coreweave.

Operating cashflow +$50B

-

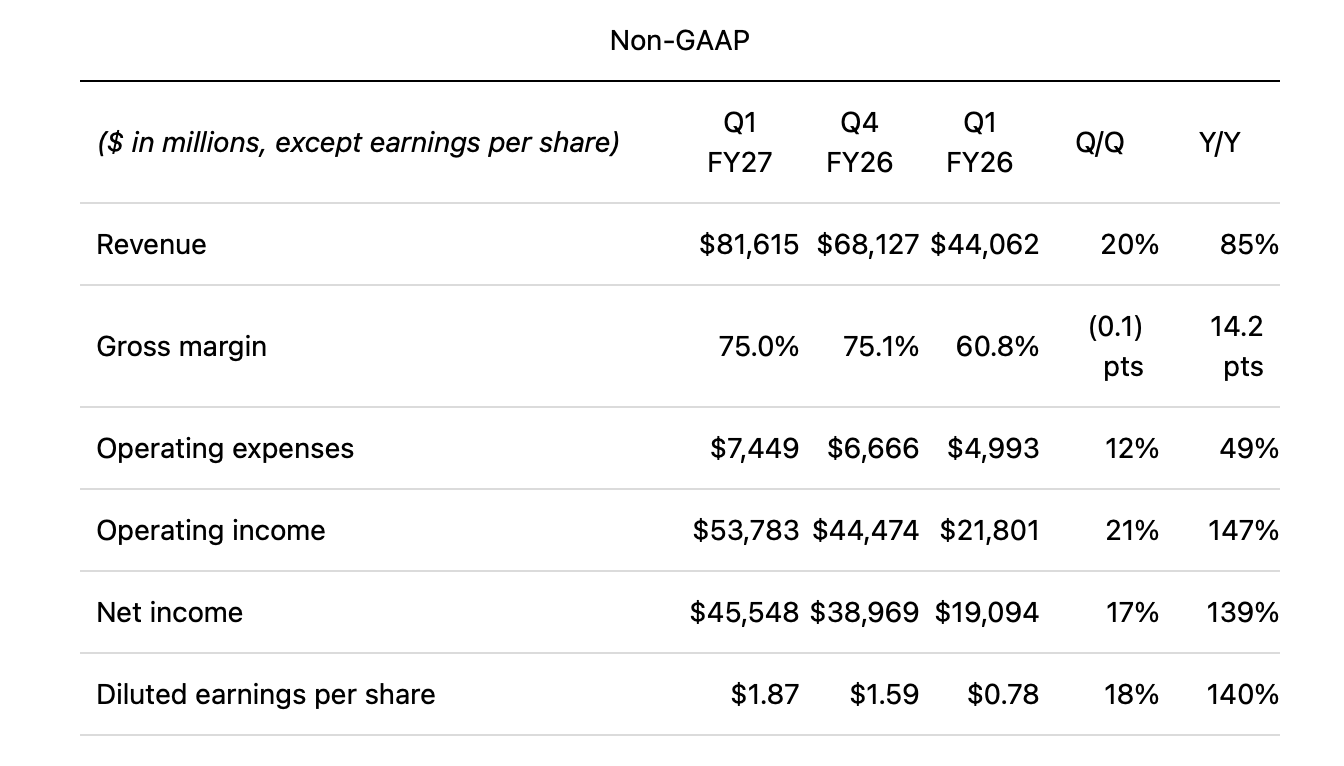

NVIDIA just delivered numbers that barely seem real. Revenue hit roughly $81.6b for the quarter, up 85% year-on-year, with data centre revenue alone at $75.2bn. Guidance for next quarter came in at around $91bn — comfortably ahead of expectations. Gross margins are still sitting around 75%, which at this scale is almost absurd.

This is arguably the most staggering earnings print corporate America has ever seen in absolute dollar creation. The key point is not just the growth rate — it is the combination of hypergrowth and elite profitability.

Most companies can do one or the other. NVIDIA is doing both simultaneously at a scale previously associated with oil majors or sovereign economies.

The market was worried margins would crack as Blackwell ramps and competition intensifies. Instead, management effectively said margins around the mid-70s are sustainable even while revenue accelerates towards a $350b+ annualised run rate. That changes the entire valuation debate.

Jensen Huang’s framing was telling: this is no longer about selling chips; it is about building “AI factories” and becoming the infrastructure layer for the next computing era. Hyperscalers are still spending aggressively, inference demand is exploding, and sovereign AI buildouts are only starting.

At this point the bear case is no longer “AI demand collapses”. The only credible concerns are geopolitical restrictions, customer concentration, or eventually the law of large numbers. But right now, the numbers keep overwhelming every attempt to call the peak.Management approved an additional $80b share buy back, which now totally $140b. The dividend was also raised 2,400% to 25c

NB-Look at the growth. 85% on revenue and 140% on EPS. Massive operating leverage too. JA sub 20 Fwd PE. Perhaps 18.

Earnings call highlights:

Main Takeaways From NVIDIA Earnings

Revenue growth was massive — again

NVIDIA posted another record quarter:

Revenue reached $82B, up 85% year-over-year and 20% sequentially

This was the company’s 14th consecutive quarter of sequential growth

Free cash flow came in at $49B

Data Centre revenue alone was $75B

Management said demand for AI infrastructure continues to accelerate globally.

Blackwell demand is exploding

The dominant theme of the call:

Demand for Blackwell systems has gone effectively vertical.

Management stated:

Blackwell is the fastest product ramp in company history

Hyperscalers and frontier model companies are deploying hundreds of thousands of GPUs

GB300 demand is exceptionally strong

Blackwell now powers or supports nearly every major frontier AI lab

They repeatedly stressed that inference demand — not only training — is now driving enormous spending.

NVIDIA says “AI factories” are the new data centres

A major change in positioning:

NVIDIA no longer frames GPUs as standalone chips.Instead:

Customers are building “AI factories”

The important metric is no longer GPU purchase price

It is:

token throughput

token cost

utilisation

energy efficiency

lifetime economics

Jensen Huang essentially argued that compute capacity is now directly linked to revenue generation.

Their thesis:More compute = more AI output = more customer revenue.

They believe AI infrastructure becomes a multi-trillion-dollar market

One of the boldest claims:

Hyperscaler CapEx could exceed $1T annually by 2027

Total AI infrastructure spending could reach $3T–$4T per year by the end of the decade

Management believes AI is shifting from optional software enhancement to essential infrastructure across nearly every industry.

NVIDIA is changing how it reports the business

The company reorganised reporting into:- Hyperscale

Public cloud giants and major consumer internet firms. - ACIE

(AI cloud, industrial, enterprise)

This includes:

sovereign AI projects

AI-native clouds

enterprise deployments

industrial AI systems

Management strongly implied this second category could eventually surpass hyperscalers in size.

Jensen’s central argument: NVIDIA wins because it owns the whole stack

Huang spent a large portion of the call reinforcing this point.

NVIDIA claims its advantage is not merely GPUs, but:chips

networking

software

CUDA ecosystem

system integration

rack-scale infrastructure

deployment tooling

He described NVIDIA as the only company delivering a fully integrated AI platform across hyperscale, enterprise, sovereign AI, robotics, and edge computing.

Vera CPU was a major surprise

Possibly the most underappreciated part of the call.

NVIDIA now believes CPUs become critical in agentic AI systems.Why?

Because:

agents orchestrate tasks on CPUs

tools, browsers, memory systems, and workflows run on CPUs

GPUs still perform the “thinking”, but CPUs coordinate everything

They introduced:

Vera CPU

A custom ARM-based CPU tightly integrated with Rubin GPUs.

Claims included:1.5x faster per core

2x performance per watt

4x rack density versus x86 alternatives

Most striking statement:

NVIDIA sees nearly $20B in standalone CPU revenue this year.

That represents a substantial expansion beyond GPUs.

Rubin is arriving quickly

Rubin shipments begin in Q3.NVIDIA says Rubin could deliver:

up to 35x higher inference throughput

up to 10x greater AI factory revenue versus Blackwell

Huang also claimed:

every major frontier AI lab is expected to adopt Rubin

Rubin adoption could exceed Blackwell adoption

Inference is now the centre of the AI race

Another major shift in messaging.

The company repeatedly stated:AI has evolved from:

one-shot inference

→ reasoning

→ agentic AI

They now view inference as the dominant long-term compute market.

Jensen specifically said NVIDIA is rapidly gaining inference market share.Physical AI and robotics are becoming meaningful businesses

Edge computing revenue reached $6.4B.

They highlighted:robotics

autonomous vehicles

AI-powered telecoms networks

industrial systems

robotaxis

The company said physical AI generated more than $9B in revenue over the last 12 months.

China remains largely absent

Important detail:

NVIDIA said it is not including China data centre revenue in guidance because export restrictions remain uncertain.So current forecasts exclude potential China upside.

Capital returns increased sharply

NVIDIA announced:

dividend increase from $0.01 to $0.25

new $80B buyback authorisation

target to return roughly 50% of free cash flow to shareholders

That is a major signal of confidence.

Guidance exceeded expectations

Next quarter guidance:

Revenue: $91B ±2%

Gross margins around 75%

Management also reiterated confidence in:

$1 trillion of Blackwell + Rubin revenue between 2025–2027.

That figure clearly surprised analysts.

Jensen’s underlying message

The entire call essentially boiled down to this-NVIDIA no longer sees itself as:**a GPU company

or even simply a semiconductor companyIt sees itself as:

the operating system of the AI economy

the infrastructure layer beneath agentic AI

the default platform for frontier AI models

And Jensen clearly believes AI compute demand is still in the early stages — not near the peak.

That is why the tone of the call was unusually aggressive, even by NVIDIA standards. - Hyperscale

-

Did Nvidia suggest they alone would buy all the memory?

On today’s conference call, NVIDIA stated that it expects the standalone Vera CPU market to reach $20 billion in FY2027.

The unit price of Grace CPU is estimated at around $3,000–$5,000. Since Vera is the successor to Grace and is optimised for AI agentic workloads, we expect Vera to carry a higher ASP of roughly $5,000–$8,000 per unit.

Assuming a Vera CPU ASP of $8,000, a $20 billion market would imply 2.5 million CPUs.

It remains unclear whether standalone Vera CPU sales will include the same SoCAMM capacity as NVL72. However, assuming the same capacity is applied, each Vera CPU would have 8 SoCAMM slots. Assuming 192GB per module, SoCAMM capacity per Vera CPU would be 1,536GB.

Therefore, FY2027 SoCAMM demand for Vera CPU would be:

2.5 million CPUs × 1,536GB = 3.84 billion GB, or 30.72 billion Gb.

CY2026, which broadly overlaps with NVIDIA’s FY2027, SoCAMM supply from the three major DRAM makers is estimated at 30 billion Gb. Therefore, combined SoCAMM demand from NVIDIA’s standalone Vera CPU sales and VR NVL72 sales already appears likely to exceed the annual (global)supply capacity of 30 billion Gb.

Assuming CY2027 VR NVL72 shipments of 100,000 servers, we estimated the SoCAMM TAM at 44 billion Gb based on 192GB modules. If additional SoCAMM demand from standalone Vera CPU sales is added, the CY2027 SoCAMM TAM could exceed 80 billion Gb.

An annual 80 billion Gb of LPDDR5 would be nearly equivalent to the annual LPDDR5 TAM used for smartphones.

The shortage of LPDDR5 — and of DRAM overall — is likely to intensify further over time.

-

Beyond the precious. Price $7-$8M which includes circa $1.3M in 'memory'. It's early! Each rack requires 20.7 TB of HBM4. Micron is in 'mass production' phase-all sold out until 2028 at least

-

Uber, Autobrains, and NVIDIA are teaming up to launch a robotaxi pilot in Munich (pending approval).

Uber brings the ride-hailing platform, Autobrains provides the self-driving software, and NVIDIA supplies the DRIVE Hyperion hardware that supports Level 4 autonomous driving.

Level 4 basically means the car can handle all driving within a defined area without human input, but it still operates within limits like mapped regions or specific conditions. No driver needed in those zones, but it’s not fully “anywhere, anytime” autonomy yet.

The big idea here is scale: instead of one company building a closed system, they’re pushing an OEM-agnostic setup where different car manufacturers can plug into the same stack and join Uber’s network.

-

Headline-Cathie Wood loads up on Nvidia, cuts AMD across flagship ARK funds.

Cathie sold out of Nvidia before the run in 2023 and spent the next 2.5 years calling it over valued -she sold at between $14-$20 and now she 'loads up'.

-

Nokia (NOK) said it has developed the telecom industry's first commercial artificial intelligence-powered radio access network (AI-RAN) platform in collaboration with Nvidia (NVDA), a move aimed at significantly increasing the amount of data mobile operators can transmit over their existing network infrastructure.

The development comes less than 10 months after the two companies announced a strategic partnership, which also included Nvidia taking an equity stake in the Finnish telecom equipment maker.

Built on Nokia's AI-native anyRAN software and Nvidia's Aerial AI-RAN platform, the new system is expected to deliver more than a 100% improvement in spectral efficiency by 2028, effectively doubling the capacity of existing spectrum assets without requiring operators to acquire additional spectrum licences. The platform has already demonstrated more than 20% gains in spectral efficiency through AI-driven radio innovations, Nokia said in a statement on Wednesday.

Nokia's AI-RAN solutions will enter pilot deployments later this year before becoming commercially available in 2027, with a roadmap built around Nvidia's programmable silicon platforms.

"Telecommunications is entering the AI era — the radio access network is the next AI infrastructure," said Nvidia founder and CEO Jensen Huang. "Together with Nokia, we are bringing NVIDIA CUDA and AI into the baseband, transforming RAN into a planet-scale AI computer. This is a generational shift for operators — unlocking more capacity and efficiency from today's spectrum while creating the foundation for new AI services and the 6G era."

The announcement positions Nokia at the forefront of one of the telecom industry's biggest technological shifts. If the promised efficiency gains are achieved in commercial networks, operators could dramatically increase network capacity while reducing the need for costly infrastructure upgrades and additional spectrum purchases.