General News

-

Applied Materials (AMAT) reported last night and whilst we don't hold the stock, they added some nice commentary/weight to the Accelerator growth story. The evidence from operators at the coal face are all saying the same thing. Executives who have direct contact with their customers and suppliers-everyone in the supply chain. Consistent, planning and executing for massive growth.

Takeaway-while the market is focussed on inflation and the CPI the greatest infrastructure project in history is being built under its nose. We will take the evidence based approach all day long.

-

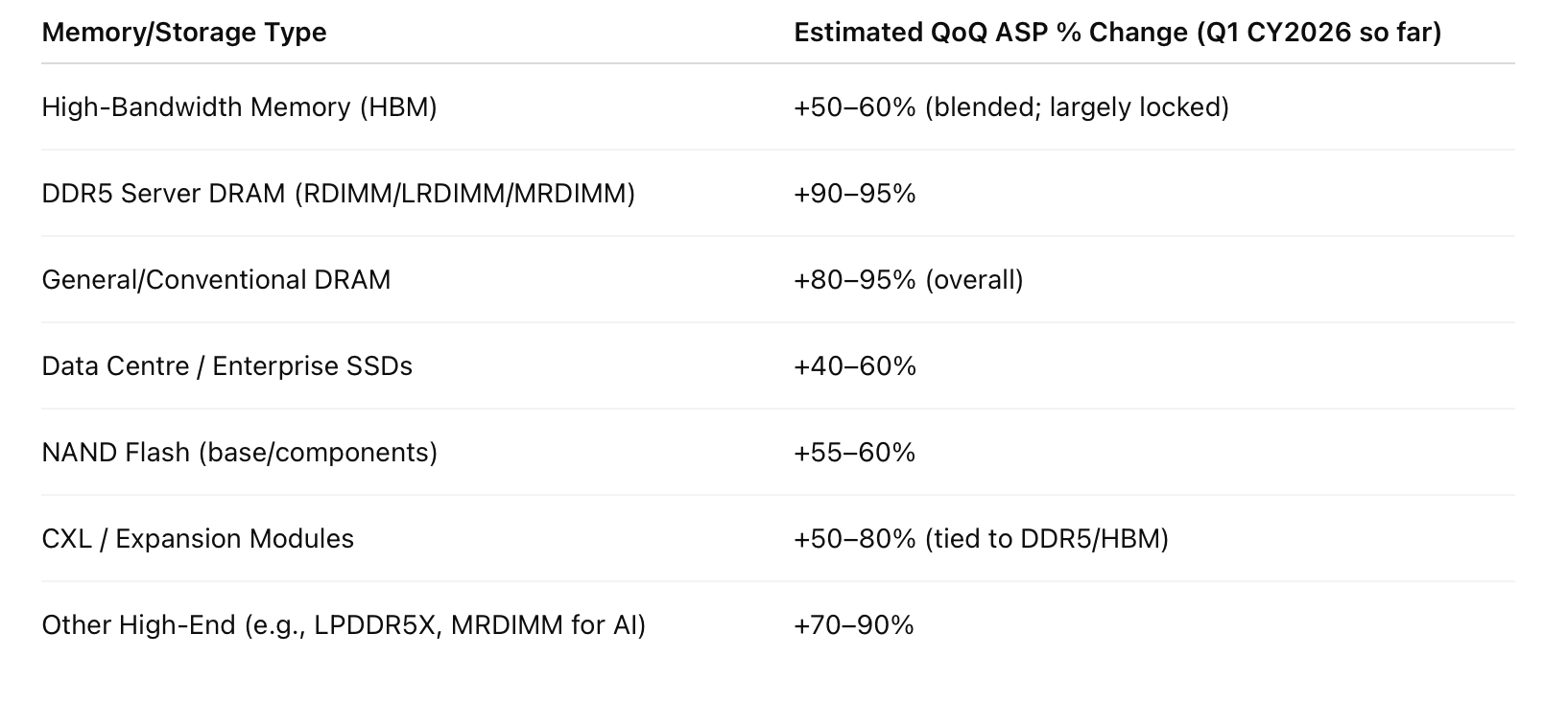

some memory pricing changes(ASP). NB-this is the approx change(increase) since the end of 2025! The impact on gross margins and revenue will be profound. Too many moving parts and their timing to even remotely estimate Microns current quarter. Suffice to say they did not factor in 'this much'. Exciting times and Micron is the one to watch in 2026!

And one more thought-if customer demand is this great, what does that say for the end product(Racks) that this memory is used in? It can only be super-massive. Who else might be the main beneficiaries? Broadcom, Nvidia being the big suppliers.

-

But everyone keeps telling us about this AI bubble…

-

There probably is a bubble for the hundreds of "AI" companies that have sprung up doing anything AI related and getting crazy valuations ....and many of them will not be around in a few years. Its hard to argue with the facts that hundreds of billions is being invested by the industry giants in the biggest datacentre build out in history. The race between China and USA for global dominance in AI continues at an increasing pace

")

-

100%-many names that are not really moving the needle but 'AI' so speculators bid them up-very fast burn and fizzle out.

All you need to do is step back and ask yourself why GOOG/MSFT CEOs who are seasoned professionals at the top of their game, have suddenly stepped on the gas. Are they gambling OR have they seen a step change in LLM ability? Does anyone believe they are risking a trillion dollars on FOMO. Does anyone believe they will share their skunk-works latest break throughs with Jim Cramer. I trust these executives to make the right decisions because they have been executing at an elite level for 20 years. I believe they know the progress is profound and they realise that a once in a lifetime opportunity is upon them. And in this game, you snooze you will lose. Game on!

-

But everyone keeps telling us about this AI bubble…

@Ducati996R said in General News:

But everyone keeps telling us about this AI bubble…

I think they meant an AI Buble (Michael)

-

You do read some really stupid comments along the way. 'Expert A' said, all AI is, is all the information ever created by humans so it cant create anything new, just repeat it. That's all I needed to read(Bin!). Just a thought, can any human or 100k humans digest all that knowledge and infer anything new?

AI doesn't need to reach super human levels to be immensely useful, close to humans will be good enough to change the way we live and generate many many trillions for those that control it.

And as an aside I think memory defines the species, without which you're lost. So silicon memory imo will be more important that the GPU as we progress because without it AI can not function. I expect most of us to own or rent our own agent which will retain everything you allow it too, for life and continuously learn how to serve your needs. It will need a lot of memory for that!

-

News on inflation- imagine the tsunami if it had been 0.00001% higher

Happy Friday

Happy FridayThe U.S. Consumer Price Index crept up 0.2% M/M in January, a cooler pace than the +0.3% consensus and slowing from +0.3% in December, according to data released by the Bureau of Labor Statistics on Friday.

On a Y/Y basis, that amounts to a 2.4% increase in January, also lower than the +2.5% consensus and +2.7% in December.

Excluding volatile food and energy prices, core CPI increased 0.3% M/M, in line with the +0.3% consensus and slightly hotter than the +0.2% pace in December. On a Y/Y basis, that comes to 2.5%, in line with consensus and down from 2.6% in December.

Overall, the numbers indicate that inflation appears to be edging closer to the Federal Reserve's 2% inflation target.

-

For anyone interested, here is an interview with the Anthropic CEO, Dario Amodei. It discusses AI diffusion and the time line to AGI-a lot sooner than you think (1-2 years away) 'a country of geniuses in the DC'. Fascinating. Do we have enough tech

What he is saying supports the conclusions/ideas we have discussed very recently, that the hyperscalers know a break through is imminent and they're stepping on the gas.

https://www.youtube.com/watch?v=n1E9IZfvGMA

version on X. https://x.com/dwarkesh_sp/status/2022357801276690455?s=20

-

It's Presidents' Day today-markets in teh US will be closed, reopening, Tuesday. Still, the news will be flowing.

-

Hopefully those Presidents can spend their day off giving the markets a damned good talking to. Those numbers have been sliding in the wrong direction recently.

ETA: Apologies if this sounds grumpy. It's because it's grumpy. It's Monday morning and we all know what Oscar Wilde said about mornings.

-

I think given the broader market we are doing well and if we ignore what the score board has to say(this month-although it looks fine to me) im the happiest in some time as to the execution of our bigger holdings. And what I mean by that is, how the companies are operating and making progress. I'm not aware of any tech portfolios which are positive in 2026 with the exception of ours.

What would you prefer. The hypothetical, stocks go on a 15% run in 4 weeks when the fundamentals don't support it(too fast, limited basis), or tread water all the while multiples contract and the fundamentals improve. One scenario suggests short term exuberance and the other long term growth. I believe we are squarely in the latter camp.

I don't make predictions generally but 2026 is an inflexion point. The daily/monthly moves don't matter, it's their worth when you get to your destination that matters. And that isn't some frivolous platitude. History, our history has supported that.

You only need to look at some of ARK funds and those of other very new entrants to see 'weeeee....oops'.

Of course past performance is no indication of future returns.

-

I think given the broader market we are doing well and if we ignore what the score board has to say(this month-although it looks fine to me) im the happiest in some time as to the execution of our bigger holdings. And what I mean by that is, how the companies are operating and making progress. I'm not aware of any tech portfolios which are positive in 2026 with the exception of ours.

What would you prefer. The hypothetical, stocks go on a 15% run in 4 weeks when the fundamentals don't support it(too fast, limited basis), or tread water all the while multiples contract and the fundamentals improve. One scenario suggests short term exuberance and the other long term growth. I believe we are squarely in the latter camp.

I don't make predictions generally but 2026 is an inflexion point. The daily/monthly moves don't matter, it's their worth when you get to your destination that matters. And that isn't some frivolous platitude. History, our history has supported that.

You only need to look at some of ARK funds and those of other very new entrants to see 'weeeee....oops'.

Of course past performance is no indication of future returns.

-

Think about this fact.

If markets were perfectly and instantly accurate about the future, it would be nearly impossible to consistently outperform them. But markets are driven by human behaviour, and humans are emotional, biased, impatient, overconfident, and sometimes irrational.

That’s where opportunity comes from.

And using MU as an example, I believe they will earn $150 in the next 21 months(not 24) and even if it's only $100 it is completely illogical that stock holders are willing to sell at $411 today. Emotion at work. That is why taking a myopic view, 'well it's up 300% in 12 months =sell' is completely the wrong move without first determining why imo. The why is they got it completely wrong.

Mutiples do not stay this low for long. We are watching developments closely and yes it's a focus because when management say the company is performing at its best in almost 50 years, opportunities like this warranty the investment in DD because the fly-wheel potential returns are worth it.

-

LAM Research CEO , a direct KLAC competitor quoted as saying yesterday......

Rampant AI demand for memory is fueling a growing chip crisis

“We stand at the cusp of something that is bigger than anything we’ve faced before,” Tim Archer, CEO of chip equipment supplier Lam Research Corp., said at a chip conference in Seoul last week. “What is ahead of us between now and the end of this decade, in terms of demand, is bigger than anything we’ve seen in the past, and, in fact, will overwhelm all other sources of demand.”

-

Palo Alto reported tonight. It's a good business but over valued imo. We sold it in Feb 25 in the 190s for one simple reason. It wasn't generating the growth its multiples suggested, i.e it looked very expensive. You are paying today 45X earnings for a 15% growth rate(act 3!). Why hold PEGs over 2 when there are others at half the price and lower, other things being equal. On this one important metric to put that into perspective. If Nvidia had these multiples it would be trading at over $1,000 and MU would be $2,000+. If fact we used some of the PANW proceeds to buy MU. PANW down 15%, MU up 340% since.

Nvidia moves up after hours as Meta signs a multi year deal to further integrate additional Nvidia systems within its ecosystem. One week tomorrow...earnings and the guide!

-

AMD has agreed to supply up to 6 GW of AI compute to Meta over roughly five years. To secure that commitment, AMD issued a performance-based warrant for up to 160 million shares.

At current prices, that’s roughly $35–$40+ billion of stock, representing about 10–12% dilution if fully vested and exercised.

The shares only vest as shipment milestones are met, but if AMD delivers the full 6 GW, the dilution becomes real.Nvidia’s total AI deployment footprint over the same period is widely expected to be closer to 9–10× larger when you aggregate hyperscalers, sovereign AI projects, enterprise, and cloud providers.

So the contrast is stark:

AMD: 6 GW tied largely to one mega-customer, secured with heavy equity incentives.

Nvidia: materially larger global deployment, dominant software ecosystem, and no need to offer double-digit dilution to win core business.Bluntly, AMD is using meaningful shareholder dilution to force its way into relevance in a market where Nvidia remains an order of magnitude larger in overall scale. Whether that gamble pays off depends entirely on execution.

The deal speaks volumes about the quality of their product and the parties relative bargaining power. The real winner being Meta who could end up getting half the servers for free. I look forward to AMDs first bleeding edge racks being released into the wild. Vera Rubin will be there to say hello.

For context my math suggests Nvidia will deploy 150GW over the same time period.

-

A lesson here on why paying sky high valuations rarely works out. It's a good business but extremely overvalued, even after tanking almost 40% in a matter of months. When you pay these prices there is zero margin of safety and management must execute to perfection. They rarely do. And why we sold PANW which was trading at a multiple of 50, a PEG of almost 3 with growth rates falling.

CrowdStrike shares reached 12‑month highs near $565 before a sharp decline. They now trade around $350–$385, down roughly 35–40% from those highs. Revenue growth remains around 20% year‑on‑year, which is respectable for a large cybersecurity firm but nowhere near the hyper‑growth that once justified its stratospheric valuation. At its peak, the stock was trading on price‑to‑earnings multiples of 150–200, reflecting expectations of perpetual explosive growth.

Even after the fall, it still carries a premium valuation compared with peers, despite only mid‑20s growth.

The launch of Anthropic’s Claude Code Security has sparked concerns that AI could automate parts of cybersecurity, threatening CrowdStrike’s business model. I have no opinion on this and it doesn't matter-the market doesn't like the idea and it's ripping the stock to pieces. The point being, buying stocks like this carried outsized risk where the potential return doesn't justify it.

The combination of an historically obscene valuation, slower growth, and the perception that AI could disrupt the business has weighed heavily on sentiment. The fundamentals are solid, but investor psychology has shifted, leaving the stock far below its highs and the market wary of future risks.