GOOG News

-

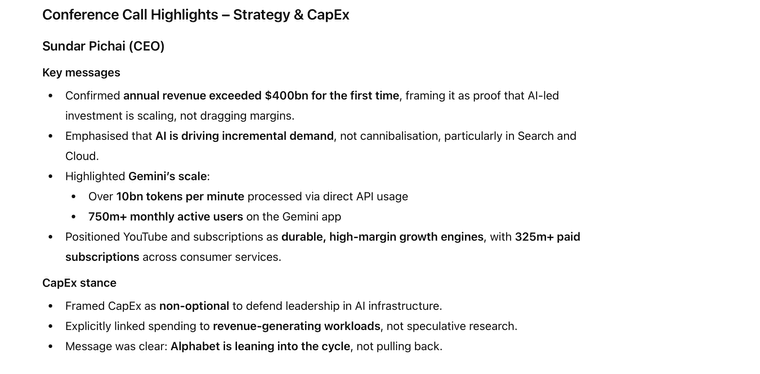

Alphabet report their Q4 earnings tonight after the close. I expect a very strong showing. Close to $115B revenue and around $2.70 eps. All eyes on GCP (Google cloud platform) and YouTube , ad dollars etc. It will be interesting to see if they MTM their Space X holding. I also expect Sundar to talk about how constrained they are and give updates on their TPU/custom Asics solutions plus RPO backlog.

Space X ran a funding round which closed mid Dec, valuing the company at $800B. GOOG last revalued their holding in July at a $420B valuation. We don't know how much they will recognised but it's between $1 and $2 EPS. If you see a headline of $3.50+ you know they revalued their holding.

GOOG purchased 7% of space X for $1B and if the IPO numbers are true, today that holding is worth $105B although they won't recognise that yet(IPO hasnt happened). Nice investment all the same.

Waymo is now worth $120B but as it's a wholly owned subsidiary, there is no MTM as it's operations are simply consolidated the same way every other operation is.

-

Alphabet report their Q4 earnings tonight after the close. I expect a very strong showing. Close to $115B revenue and around $2.70 eps. All eyes on GCP (Google cloud platform) and YouTube , ad dollars etc. It will be interesting to see if they MTM their Space X holding. I also expect Sundar to talk about how constrained they are and give updates on their TPU/custom Asics solutions plus RPO backlog.

Space X ran a funding round which closed mid Dec, valuing the company at $800B. GOOG last revalued their holding in July at a $420B valuation. We don't know how much they will recognised but it's between $1 and $2 EPS. If you see a headline of $3.50+ you know they revalued their holding.

GOOG purchased 7% of space X for $1B and if the IPO numbers are true, today that holding is worth $105B although they won't recognise that yet(IPO hasnt happened). Nice investment all the same.

Waymo is now worth $120B but as it's a wholly owned subsidiary, there is no MTM as it's operations are simply consolidated the same way every other operation is.

-

Mark to Market (revalue)

-

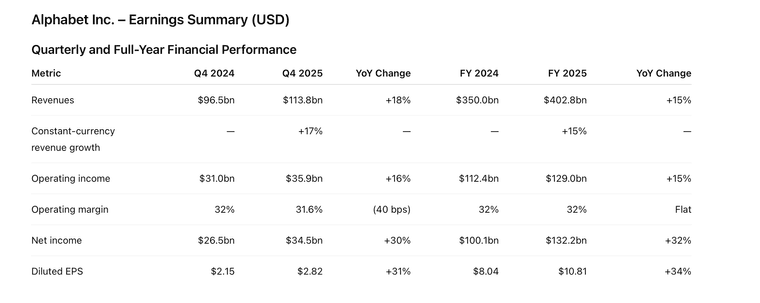

GOOG surpass my earnings 2.83. They didn’t revalue space x. 35 billion net income . Will spend 180b on capex. That’s big. But what we all need to understand, they sold the capacity. Just like msft. It’s an iron clad contractual ‘binding UN resolution’ tropic thunder’ type deal. Good news to reverse the red. Cloud up 48%. More tomorrow but a great result.

-

A brilliant result with +30% earnings from-a company this size can print gains like this. The big take away is tehehuge Capex spending-and where is this money going(who gets most of it?).

I trust the CEOs and Sundar is best placed over Dave on the internet insofar as where's a good place to be investing GOOG cash. Again he said on the call-they are constrained and they are making a lot of money from AI.

What we saw today were the extreme PE stocks, Palantir, APP, AMD get a good kicking and they dragged everything else down with it-and after hours the quality came back hard. And what you find is any stocks that have risen very fast will also fall very fast in these scenarios (Parabolic effect) but quality, as I said comes back. the dross does not!

There is a lot of noise/FUD around capital spending on GPUs etc and I have to say it's more an opportunity than a risk. A lot push/pull going on, media influence and weak hands. As always patience and staying the course.

Chief Financial Officer (CFO)

CapEx guidance (most important takeaway)

2026 capital expenditure expected at $175bn–$185bn, a sharp step-up.

Spend will be heavily front-loaded into:

Data centres

Custom silicon

AI compute and networking infrastructure

Cost discipline & margins

CFO acknowledged CapEx intensity but stressed:

Operating margins remain structurally stable (~32%)

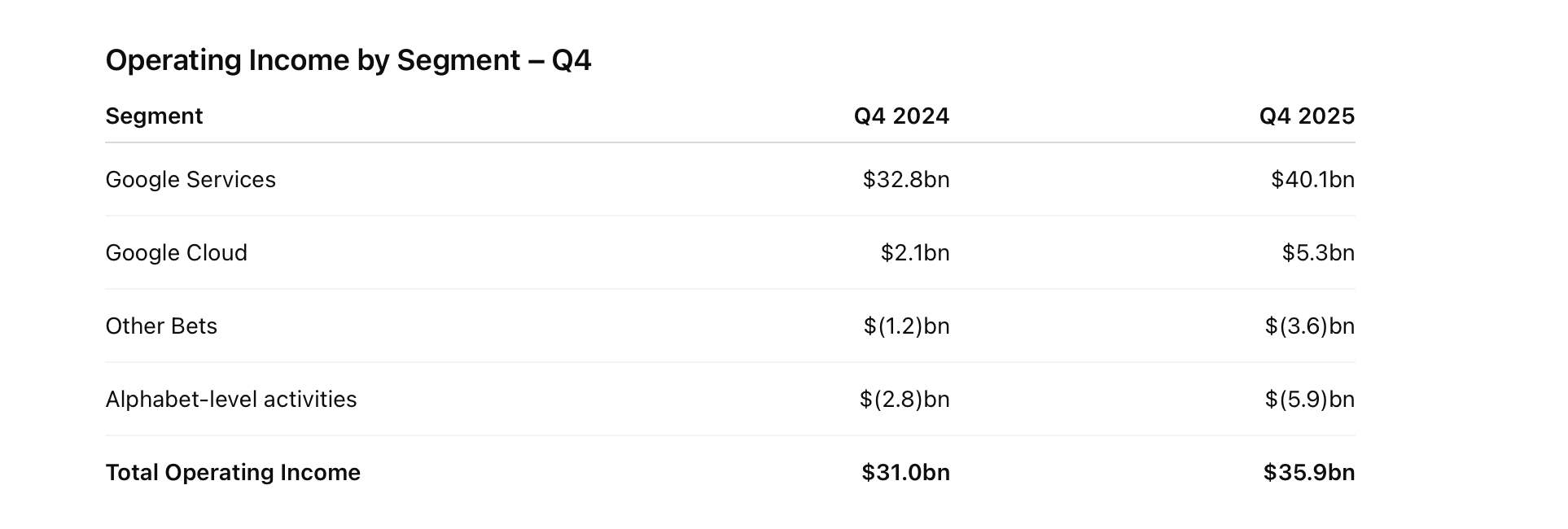

AI infrastructure investments are already driving Cloud profitabilityBalance sheet

Highlighted $24.8bn in net debt issuance in late 2025 as deliberate liquidity positioning ahead of peak investment years.

Dividend maintained at $0.21 per share, signalling confidence despite elevated CapEx.

Bottom Line

Alphabet is spending aggressively, especially on AI infrastructure.

Management is not pretending CapEx will normalise soon — 2026 is a heavy year by design.

The tone from both CEO and CFO was confident, almost blunt:

short-term cash intensity is the price of long-term dominance.

Elevated CapEx

Stable margins

Cloud and AI doing the heavy lifting on incremental returns -

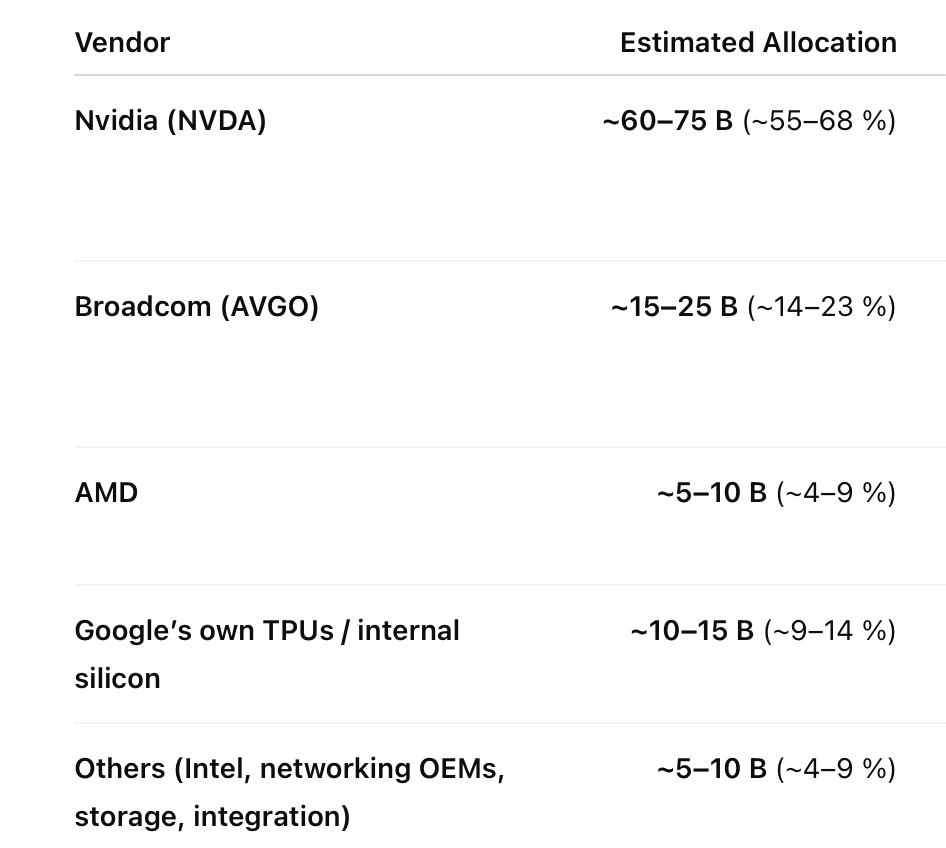

Of the $180B 2026 Capex, $110B will do towards racks scale build out, split roughly 50/50 GooG/GCP. I would estimate the following recipients of this cash pile. The clear winners being NVDA/AVGO

-

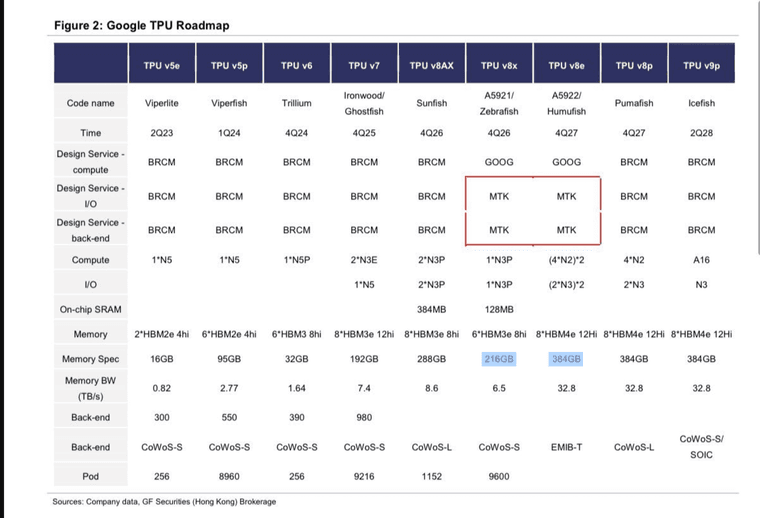

Googles own roadmap, clearly showing MORE memory utilisation in successive TPU designs. Wasn't TurboQuant going to wipe it out

-

CEO Sundar Pichai framed the quarter as AI-led across the portfolio, saying, "It's clear that our AI investments and full stack approach are driving performance across our business," and added that in Search, "AI continues to drive search usage and queries are at an all-time high."

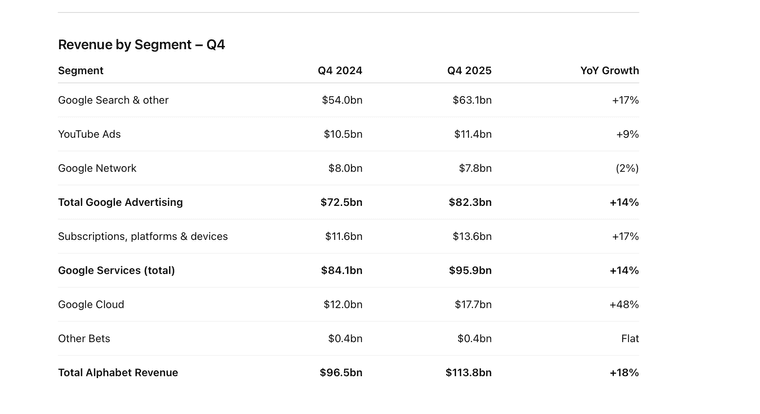

Pichai highlighted cloud demand and commitments, stating, "Cloud accelerated again this quarter due to strong demand for our AI products and infrastructure," including that revenue "grew 63%, exceeding $20 billion for the first time" and that "our backlog nearly doubled quarter-on-quarter to over $460 billion." NB- new business contracts during the quarter +> $230B!

On product and model momentum, Pichai said, "Overall, the number of paid subscriptions has now reached 350 million," and added, "Our first-party models now process more than 16 billion tokens per minute via direct API use by our customers, up from 10 billion last quarter." +60% QoQ growth

Capex raised +$10B to 180-190B in 2026 and 'our 2027 Capex will increase significantly over this.

-

And some say AI isn't being monetised

Anthropic has reportedly agreed to spend around $200 billion over five years on cloud infrastructure and AI chips from Google, highlighting the intensifying race for computing power in the artificial intelligence sector. According to the report, this deal would position Anthropic as one of the largest customers of Google Cloud, potentially representing more than 40% of its revenue backlog.

The scale of this commitment reflects rapidly growing demand for high-performance computing, driven by the expansion of Anthropic’s Claude AI models and increasing enterprise adoption of generative AI tools.

Businesses are relying more heavily on such systems for automation, analytics and customer-facing applications, which in turn requires vast processing capacity.

The agreement, signed in April, also includes access to advanced tensor processing units, with contributions from partners such as Broadcom.Deployment is expected to begin around 2027, signalling long-term strategic investment in AI infrastructure.

-

Reporting tonight. I think it will be a record:

Consensus: ~$117B revenue and ~$2.88 EPS.

I expect: ~$120B revenue and ~$3.10 EPS.

I expect Google Cloud growth of 65–70%.

AI capex. I expect another increase. Something north of $100B annualised, $25B next Q+.

I expect HBM memory to get a shout outNet Income from operations circa $37B +$20B unrealised gain from investments.

NB- The above is operational. In addition they will likely report a circa $20B gain on SpaceX mark to marketThe headline might state $5 ish-if it does that include the revaluation of the SpaceX holding.