Broadcom (AVGO)

-

A solid result from AVGO, beating expectations and guiding higher-ahead of consensus expectations. Asics is growing dramatically with the growth trend continuing through 2026.

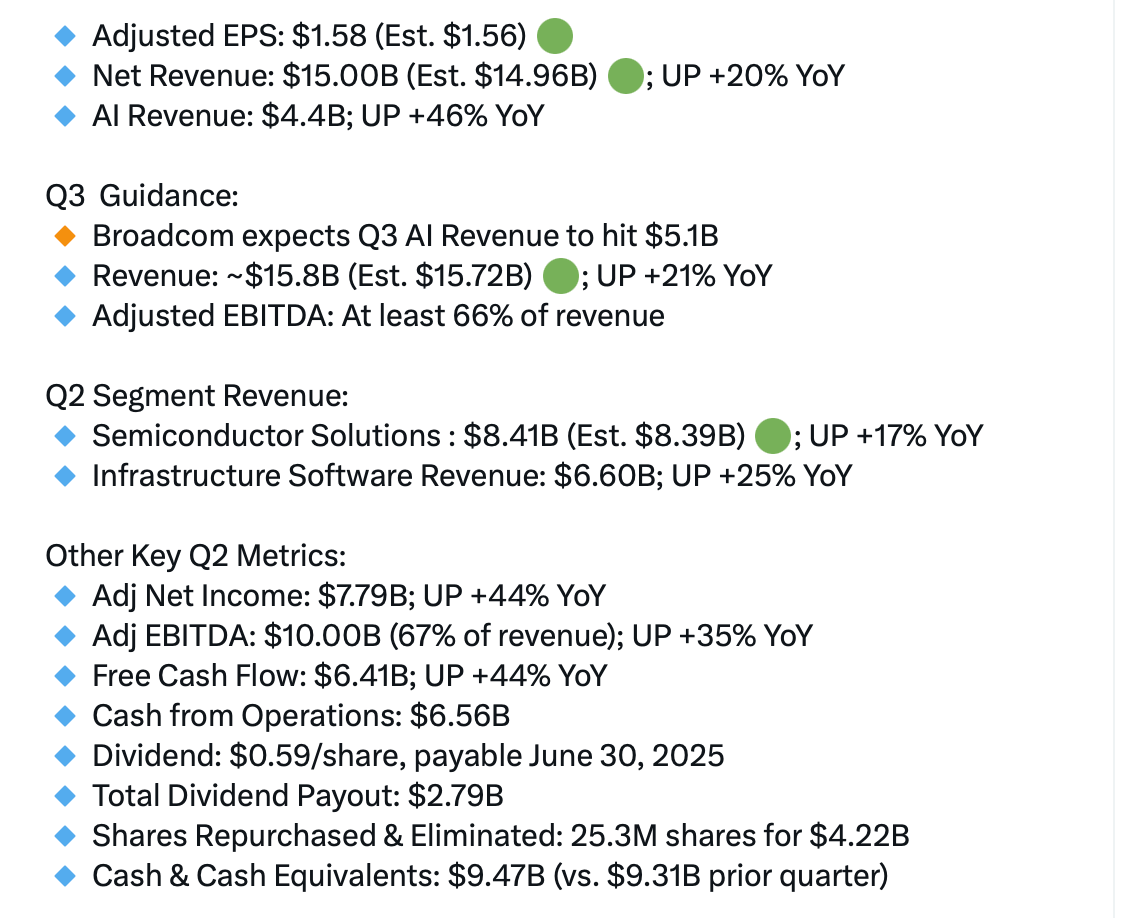

Q2 FY2025 Results:

Revenue: $15.004 billion, up 20% year-on-year, meeting estimates of $14.99 billion.

AI Semiconductor Revenue: $4.4 billion, up 46% year-on-year.

Infrastructure Software Revenue: $6.6 billion, up 25% year-on-year, exceeding guidance of $6.5 billion.

Semiconductor Solutions Revenue: $8.4 billion, up 17% year-on-year.

Adjusted EBITDA: $10.0 billion, up 35% year-on-year (67% of revenue).

Free Cash Flow: $6.4 billion, up 44% year-on-year (43% of revenue).

Capital Allocation: Paid $2.8 billion in dividends and repurchased $4.2 billion in shares.

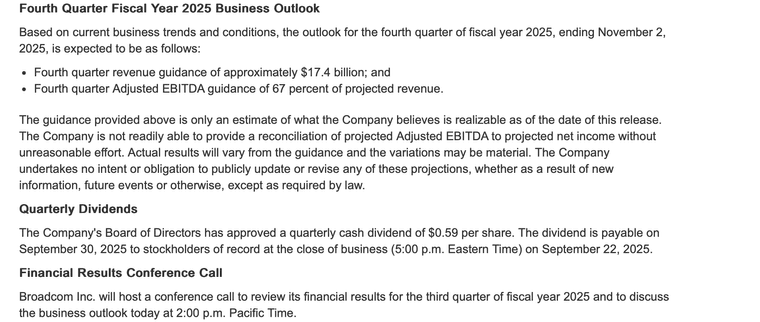

Q3 FY2025 Guidance:

Revenue: $15.8 billion, up 21% year-on-year, slightly above estimates of $15.72–$15.79 billion.

AI Semiconductor Revenue: $5.1 billion, up 60% year-on-year.

Semiconductor Revenue: $9.1 billion, up 25% year-on-year.

Infrastructure Software Revenue: $6.7 billion, up 16% year-on-year.

Adjusted EBITDA: Expected at 66% of revenue.

Management Insights

Hock E. Tan, CEO, highlighted, “Our record Q1 and Q2 revenues of $15.004 billion reflect strong AI demand and VMware momentum.” He noted AI networking (Ethernet-based) contributed 40% of AI revenue and introduced the Tomahawk 6 switch, enabling efficient AI clusters with 102.4 terabits per second capacity. Tan projected “accelerated XPU demand in late 2026 for inference and training.” Kirsten M. Spears, CFO, added, “Gross margins of 79.1% in Q1 and 79.4% in Q2 exceeded forecasts due to a favourable product mix.”

Outlook and 2026 Expectations

Broadcom anticipates continued growth, with Q3 revenue guidance of $15.8 billion and AI semiconductor revenue expected to sustain its FY2025 growth rate into FY2026. Management expressed confidence in organic growth, supported by innovations like Tomahawk 6 and strong VMware Cloud Foundation adoption (over 85% of top 10,000 customers).

Risks and Challenges

Non-AI semiconductor revenue remains sluggish, with slow recovery.

Free cash flow is impacted by VMware acquisition debt interest and higher taxes.The stock is at an all time high so we would expect a bit of churn as recently macro events play out and the stock forms a solid base to spring board to the next level. A fantastic business that has a very bright future.

-

Brilliant result last night with a very strong guide. The stock popped after hours. It’s my anniversary, back Monday :). Full analysis then

-

Come on man!! Priorities!!

-

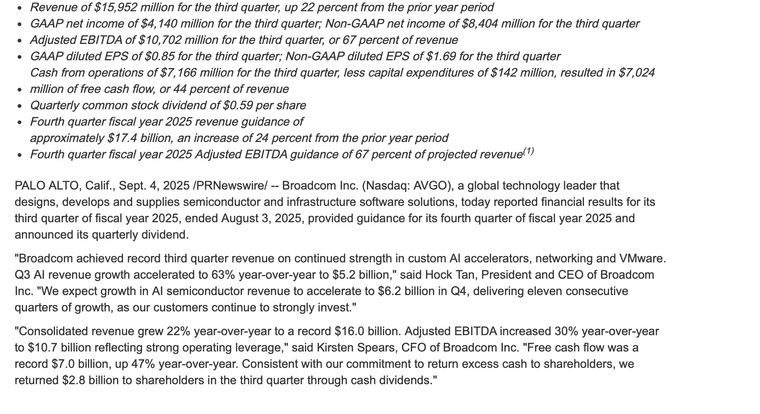

The summary results for AVGO. Everything is a record and the guide is higher still, and no doubt low balling. The backlog is now a staggering $110 billion!

Not much for me to add (hence the cut from their release) apart from Ive also heard they just signed a 10B chip deal with Open AI.

Broadcom is the perfect accompaniment to Nvidia. Will they hurt each other, imo no, because they operate in very distinct markets, save for some networking.

-

Breaking news-more to follow.

OpenAI sign a deal today with AVGO/Broadcomm for the design of a new Aspics accelerator. The size of the deal is circa 10GW which would be at least $150B. AVGO is up about $40

-

AVGO delivered. 30% growth. But guided for 47% growth. Another sub 1 PEG. More tomorrow. Here’s a mature business with record earnings today but guiding for 50% more next quarter. We are holding in tight to this one. Before this print the fwd Pe was sub 30 and it just got better.

-

Looking at their accelerator(AI) revenue-growth of > 100%

"Broadcom (AVGO) achieved record first quarter revenue on continued strength in AI semiconductor solutions. Q1 AI revenue of $8.4 billion grew 106% year-over-year, above our forecast,

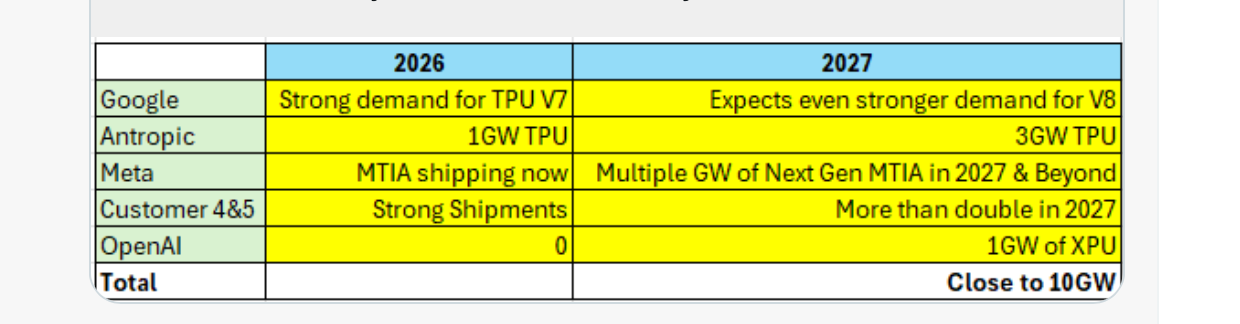

Looking forward to the next 18 months- anticipated 10 GW from 1-2. The cost is $20B/GW roughly. Can they generate 200B from a TTM of 33B? That is some crazy growth.

-

From the earnings call. Broadcom is firing on all cylinders-Growth is accelerating, 30-40% into late 26/27 net and in areas that matter a lot higher

Management view

Q1 2026 revenue reached a record USD 19.3 billion, up 29% year on year, driven by stronger-than-expected AI semiconductor growth.

Adjusted EBITDA was a record USD 13.1 billion (68% margin). Operating income rose 31% to USD 12.8 billion, with operating margin at 66.4%. Gross margin was 77%.

AI semiconductor revenue surged 106% year on year to USD 8.4 billion. For Q2, semiconductor revenue is forecast at USD 14.8 billion (up 76%), with AI revenue of USD 10.7 billion (up 140%).

A sixth custom AI accelerator customer has been added. Visibility into 2027 has improved significantly, with management claiming line of sight to over USD 100 billion in AI chip revenue, (materially conservative because 10GW is closer to $200B) supported by secured supply chain capacity. OpenAI is expected to deploy its first-generation XPU in 2027 at more than one gigawatt of compute capacity.Infrastructure software revenue was USD 6.8 billion, up 1% year on year. VMware Cloud Foundation is positioned as a core data centre software layer supporting generative AI workloads.

Free cash flow was USD 8 billion (41% of revenue)(huge). The company returned USD 3.1 billion in dividends and repurchased USD 7.8 billion of shares, with an additional USD 10 billion buyback authorised through 2026.Outlook

Q2 2026 revenue guidance: approximately USD 22 billion, up 47% year on year.

Infrastructure software expected at USD 7.2 billion (up 9%).

Gross margin expected to remain at 77%; (huge)adjusted EBITDA margin around 68%.

Non-GAAP tax rate projected at approximately 16.5% for Q2 and FY2026.

Financial position

Semiconductor Solutions revenue: USD 12.5 billion, with 68% gross margin and 60% operating margin.

Infrastructure software gross margin was 93%, operating margin 78%.

Cash at quarter-end: USD 14.2 billion. Inventory rose to USD 3 billion, with days of inventory increasing to 68 (from 58 in Q4).Q&A themes

Analysts questioned the sustainability of AI demand, hyperscaler returns, customer-owned tooling risks, networking mix, and potential margin pressure from rack sales.

Management pushed back firmly, highlighting accelerating inference demand, limited near-term competitive threats in customer-owned tooling, rising AI networking contribution (expected 33–40% of AI revenue), and stable gross margins despite product mix changes.Overall take

Management is increasingly confident, pointing to accelerating AI growth, expanding customer relationships, and multi-year visibility supported by secured supply. Analysts remain cautious on durability of demand and margin resilience, but management maintains that scale, technology leadership and supply chain control underpin its target of exceeding USD 100 billion in AI chip revenue by 2027. Conservative!

It's a wrap

") Last time I checked teh stock was up 5% AH

Last time I checked teh stock was up 5% AH -

I keep a close eye on growth (and margin). There is no point investing in companies with falling growth, tempered with the fact as numbers get very large you can't keep growing at the same pace. However PEG is a critical metric for a mature business. I'd never pay over 2. A decade ago the gold standard was 1.0 and today the experts would have you believe anything less than 2 is a good proposition-i strongly disagree.

Palantir has a PEG of 4-5 and it's interesting that their management and many analysts will point to high growth, high margins etc. But Nividia beats it on all those key metrics and yet has a PEG of 0.5. So if anyone wonders how this comes about, I don't blame you because it makes no sense to me either. We don't hold the stock and won't, for precisely this reason. It's a good business but imo its valuation is obscene. As expected it's gone nowhere, in fact those that purchased mid 2025 are flat, which is exactly what happens at extreme valuations. And if management made just one misstep the stock will be cut in half.

I say this purely to articulate that valuation always needs a sense check, never get caught up in FOMO, there are some simple numbers anyone can look at to get a rough guide on relative value. And investing is all about risk and return. A stock with a very frothy valuation can certainly move much higher but when you buy it you are taking on much more risk relative to the gains you might make.

-

Breaking

Broadcom announced agreements with Google and Anthropic, today and are shaping up to be some of the most significant AI infrastructure deals in the industry. The long-term contract with Google runs through 2031 and covers the development and supply of future-generation tensor processing units (TPUs) as well as networking and other components for next-generation AI racks.

While the company has not disclosed financial terms, the scale and strategic nature of the deal suggest it could generate tens of billions of dollars in revenue over the next decade.

In parallel, the agreement with Anthropic gives the AI chatbot company access to approximately 3.5 gigawatts of TPU compute capacity starting in 2027. Industry estimates for the cost of building and operating TPU-scale AI hardware indicate that this portion alone could represent multi-billion to potentially tens of billions USD in infrastructure investment.Combined, the two deals could plausibly exceed $50 billion USD, making them a transformative, multi-year revenue driver for Broadcom and cementing its role in the rapidly expanding AI hardware market.

-

When the 'news'(fake) dropped I was highly sceptical...also the rumour Nvidia was buying DELL-makes no sense at all. DELL is a low margin capital intensive business -the exact opposite environment that Nvidia operates in.

JPM says reports that MRVL won Google TPU business are false, arguing Google is talking to multiple parties while AVGO remains the clear incumbent.

-

News out-a good example of how based on evidence, Broadcom had the wind at its back

Apple (AAPL) has signed a new multi-year agreement with Broadcom (AVGO) worth more than US$30bn, marking its largest commitment under its American Manufacturing Programme.

The deal will see Broadcom produce more than 15bn US-made chips through 2031, expand its Fort Collins, Colorado facility with a US$1.5bn investment, and support hundreds of American jobs. The company will supply custom silicon, including advanced RF components and wireless connectivity technologies for future Apple products.