Micron Technology

-

It’s up 10% after hours. And frankly that’s a joke.

-

Insatiable demand-quote. 16 Long Term supply agreements signed-up from 1 last Q. Typically 5 years term representing a min of 40% and up to 50% of total output through 2030 calendar year.

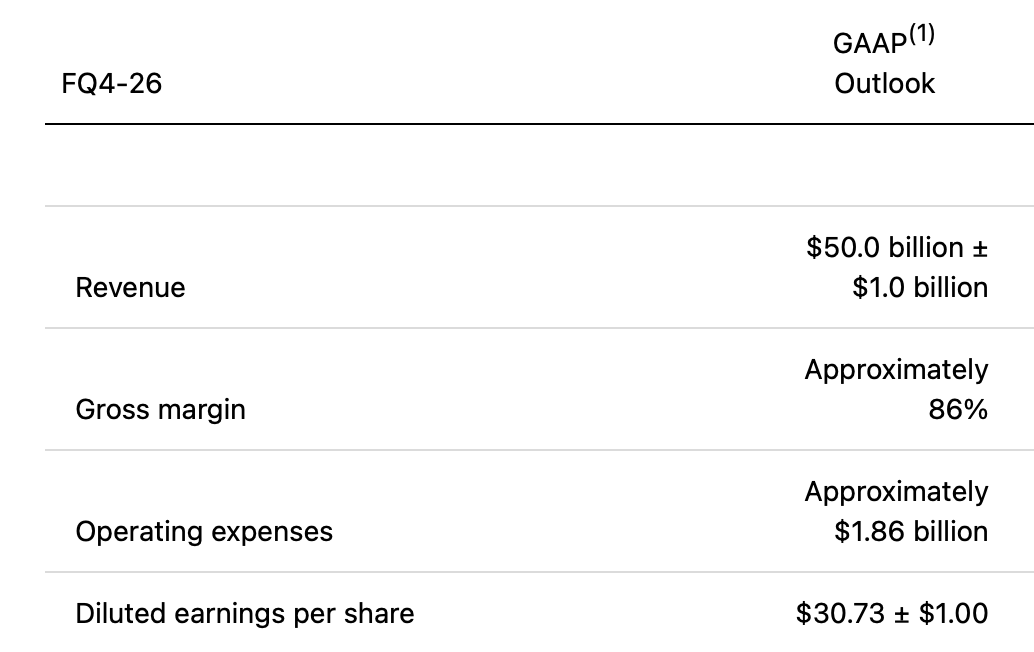

G9 and 1gamma ramping well. Demand is so high management can not see any relief, period. Margins guide 86%.

Multi decade expansion expected due to robotics and autonomous vehicles (check)

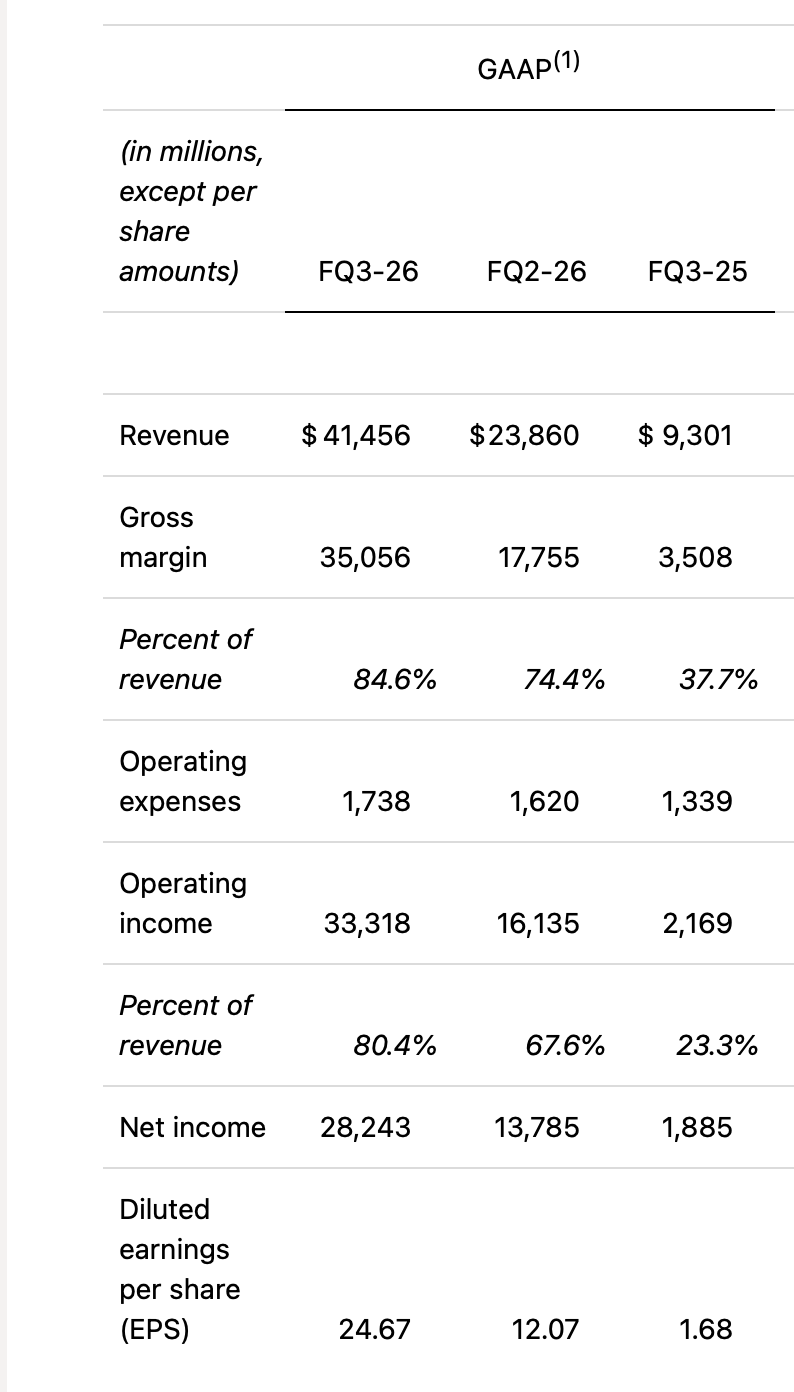

Revenue YoY +345%

Gross margin +4,690 bps

Operating Income +1,436%

Net Income +1,398%PE Fwd sub 10 and likely closer to 7. The company is making MSFT/Apple+ money and growing quickly. Not much else to say, just staggering. No stock split hey ho.

From the end of this year 'we intend to return 100% of our free cash via stock buy backs'The stock is trading at $1,200 after hours.

Outlook/Guide

Margins 86%/revenue $50B and EPS $31comparison

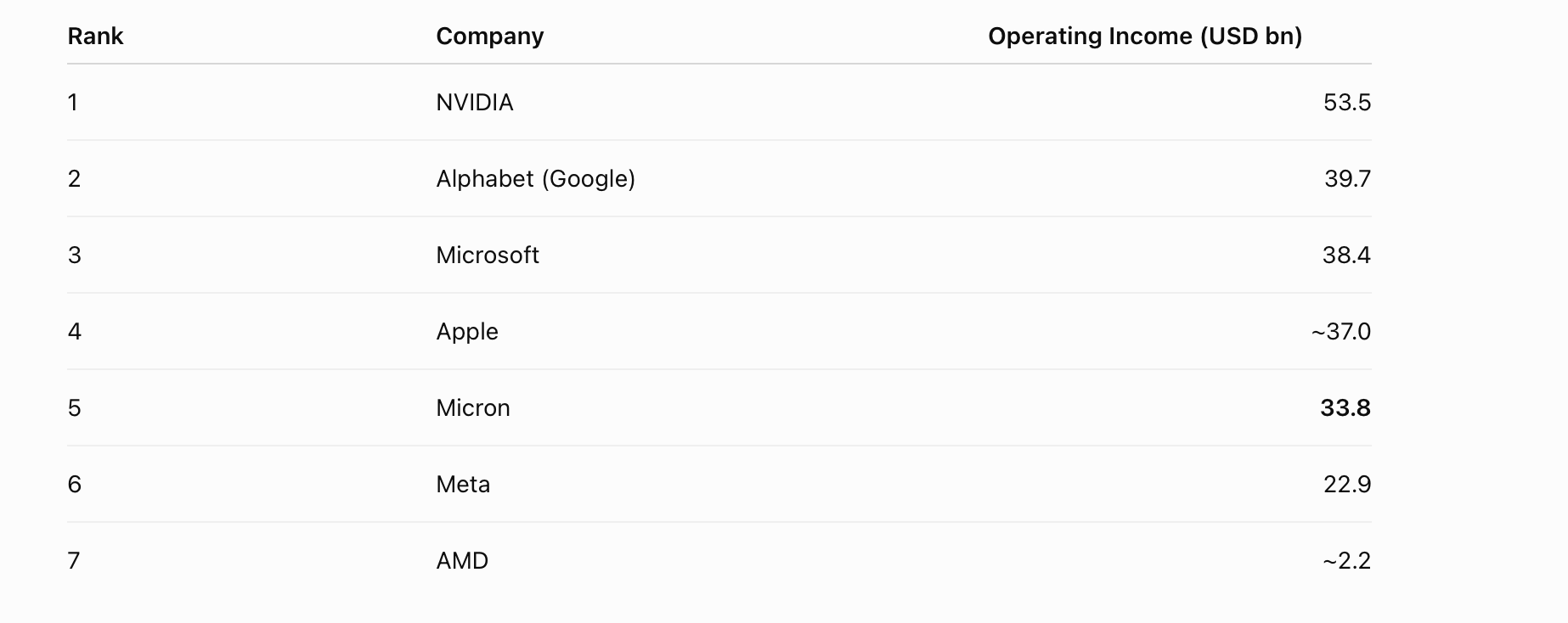

Quarterly Operating Income is growing +7B/Q so I would expect Micron earnings to exceed all companies bar Nvidia within another Q or so.

-

The quote of the earnings call. Is anyone listening? To 'begin' in a couple of years?

“Humanoid robots carry 10 times the amount of memory as an average L2+ vehicle. We expect a sustained substantial multi-decade memory demand cycle to begin in the latter part of this decade.” — Micron CEO Sanjay Mehrotra

-

Three weeks ago we said..... it's nice to be right. It seems the biggest analysts on WS read our pages having received some DMs-pretty cool

-

@Adam-Kay said in Micron Technology:

It’s up 10% after hours. And frankly that’s a joke.

As in it shouldnt be up that much?

-

More i think,maybe 20%

-

I like your Nr better

-

@Adam-Kay said in Micron Technology:

It’s up 10% after hours. And frankly that’s a joke.

As in it shouldnt be up that much?

@Slow-Horses A beat and raise like that imo deserved 50%

-

@Slow-Horses A beat and raise like that imo deserved 50%

@Adam-Kay said in Micron Technology:

@Slow-Horses A beat and raise like that imo deserved 50%

wowsers!

-

just my opinion

")

-

What’s your thoughts on the reports I was seeing yesterday regarding no shortage of memory and potential price fixing

-

post up the link and I'll take a look

-

Surely the timing of such news is opportunistic at best? https://www.pacermonitor.com/public/case/65375103/Garciaguirre_et_al_v_Samsung_Electronics_Co,_Ltd_et_al

-

I think the law suit is a joke-the plaintiffs are a group of retail consumers upset at paying higher prices.

I think they will fail at the first hurdle 'motion to dismiss' because they need evidence and in today's Information Age it's obvious there is a severe shortage. It's not worthy of any more time imo. The lawyer involved is part of a 'firm' with 8 staff.Micron will likely retain Simpson Thacher & Bartlett an elite global firm with a formidable team. Between opposing counsel there will be significant disparity in size, resources, and defense experience. I expect the lawsuit to be tossed.

-

just in....Korea's memory semiconductor industry is understood to be pushing to raise the average selling price (ASP) of commodity DRAM in the third quarter of this year by as much as 20% versus the prior quarter.

With supply shortages persisting across the entire product lineup on the back of AI infrastructure investment, memory makers are interpreted to be extending a strategy of maximizing profitability. The pace of price increases will slow thereafter, but industry sources say an extremely high profitability trend will continue into next year as well.

According to the industry on the 3rd, Samsung Electronics is in negotiations with customers targeting a Q3 DRAM ASP increase of up to around 20% versus the previous quarter.

SK Hynix is also believed to have entered long term contracts with customers but are demanding deposits up to 30% and have removed all price caps.

-

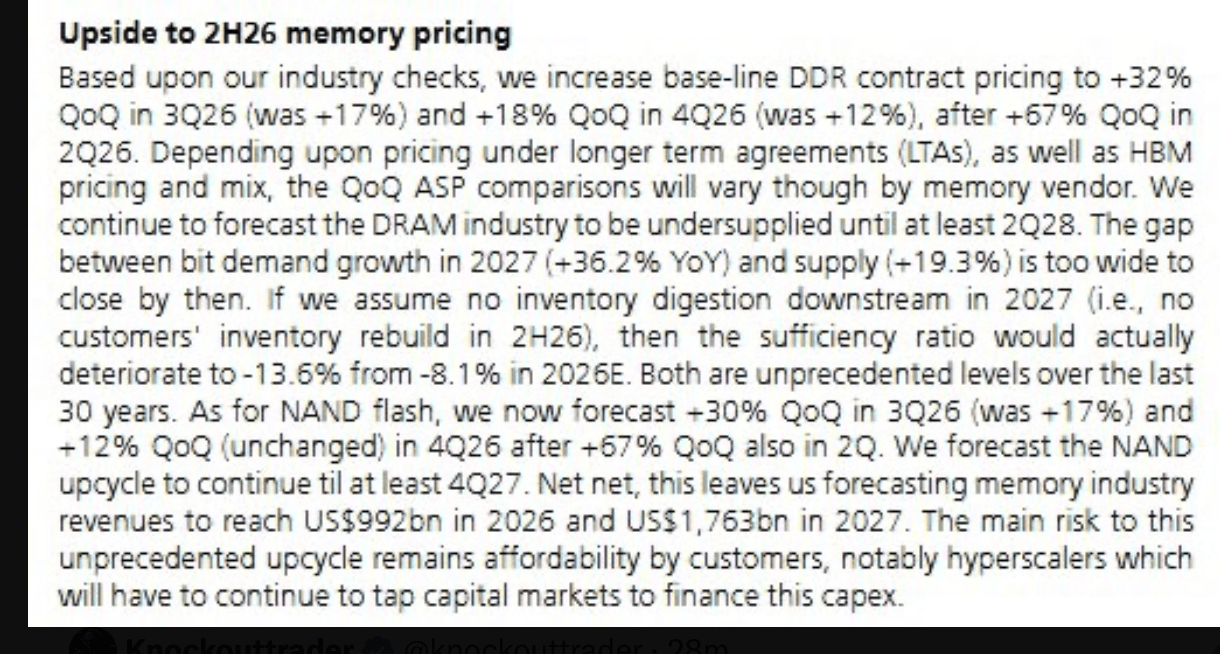

UBS raises its DRAM and NAND price forecasts even more

DRAM prices are now expected to rise 32% QoQ in Q3 and 18% QoQ in Q4.

NAND prices are expected to rise 30% QoQ in Q3 and 12% QoQ in Q4.

Note anticipated supply increase (+19.3%)-this is the industry, however Micron is growing bit supply by at least 25%-30%-minimum 6%+ per Q. Second point +36% demand grow, ergo the gap widens. I think +36% is very low. Imo it's > 50% simply due to rack density and number of racks shipped. Third point 2027 revenue for 'memory' forecast +78%. I also disagree with the forecast that supply catches up with demand in the second half of 2028-the industry and even large customers expect 2030 earliest.