Micron Technology

-

We are rebalancing today, a timely opportunity to trim the surplus weight from Micron having touched $650 earlier

We purchased the holding in Feb 25 for $89.82

NB we are trimming it NOT selling is.

-

Thanks for the heads up, are you buying into any other tech stocks. Thanks

-

Hi Jason,

Tweaks at the last rebalance(yesterday). It's more a case at the moment of looking at some holdings, Meta for example and determining that given its growth the market is discounting it unjustly. If you look at what is happening lately money is flowing into some areas, leaving others out of favour which is fine if that is based on fundamentals however in MSFT/Meta's case I would take the view that growth is up, EPS is up but the stock is down. All we have to do is(if correct) add more weight to these and reduce a bit elsewhere.

I'm always looking at new ideas but it takes time to get comfortable with the business. Often the best opportunity is the one you currently hold- you get to know them very well and sometimes you think 'opportunity'. Stocks are almost always mispriced-some too high, some too low. Look at Micron, from 450 to 319(30 march) and today it's $650. That is an unusual situation however the principles are solid. If the evidence says hold, you do so. Never let a score board (tail) wag the dog(investor). We have been talking about its ridiculously cheap price for 6-9 months- we didn't get lucky. We did the work and it paid off handsomely. Patience is key.

If anyone wants to discuss they are welcome to contact me.

Regards

Adam

-

Thanks Adam for the reply, im always interested in the tech stocks we hold and there progress.

Keep up all the good work the numbers are good.

Kind regards Jason. -

Tbh I struggle with Meta. Yes, it looks cheap in many ways but unlike most other PHT constituents their revenue stream is very narrow and entirely ad driven (as far as I know). There is no product as such. They are completely reliant on increasing user numbers and improving targeted ads etc. Personally I don't consider it at significant discount but I hope to be proven wrong.

-

New eSSD hits the market

The launch of Micron’s 245TB 6600 ION SSD is a significant milestone for the data-centre industry because it pushes flash storage into territory traditionally dominated by hard drives. At 245 terabytes per drive, operators can dramatically reduce rack space, power usage and cooling costs, which matters enormously as AI workloads consume ever more infrastructure capacity.

The drive uses PCIe Gen5 and NVMe, with sequential read speeds of roughly 14GB/s and write speeds around 3–7GB/s depending on configuration. Random performance is also far higher than conventional HDD arrays, while latency is vastly lower. The SSD is built using Micron’s latest QLC NAND technology, prioritising storage density over ultra-high endurance.This could become a major revenue opportunity. Hyperscalers, AI cloud providers and enterprise customers are all racing to expand storage for training data and inference systems. Even at an estimated price likely exceeding US$20,000 per unit initially, the economics can work because one drive can replace large numbers of hard disks and associated infrastructure.

-

My thoughts.....The monetisation case for WhatsApp is potentially one of the largest untapped platform opportunities in global technology history.

Right now, WhatsApp is structurally under-monetised relative to its scale. Meta effectively owns the communication layer for huge parts of the developing world. In countries like India, Brazil, Indonesia, and Mexico, WhatsApp is not just messaging infrastructure — it is social identity, customer support, commerce discovery, and increasingly business infrastructure.I wouldn't be surprised if the company starts producing physical AI products including robots. The data they collect and their analytics of same is the reason they achieve the highest $ (advertising rates) of any platform in the world.

Meta's product is their users-they are very sticky. They aren't going away. Based on fundamentals their growth and earnings power(formidable) would tell me their stock is under valued.

-

Interesting comments about WhatsApp. I've often pondered how they make money for it; you're confirming that they don't.

If their long game is using data for their AI robotics piece then how will they harvest that data, given it's all encrypted and very secure (or so they tell us)?

-

They do in other countries, India, Brazil plus enterprises use it for marketing. I would estimate they generate 1-2 billion from the platform however that's tiny and it could generate a lot more

-

Wow and wow

-

yes new high MU and KLAC

")

-

I can't take all the credit

-

At Computex, yesterday Chey Tae-won, SK Hynix Chair, said 'memory' will be constrained despite aggressive expansion in bit growth, until at least 2030.

It's the end of the Q for Micron (May 29). Earnings are scheduled to be reported Wed June 24th:

I expect Revenue of $40B and net income of $25B (EPS $24)

I expect the Q4 guide to be close to $50B and net income > $30B (EPS $29-$30)

Management seem to consistently play it very safe so +$8B-$10B is likely re the guide. It seems somewhat academic given the market conditions (every wafer sold at very high margins), demand approx 2X supply and getting more favourable for the vendor. Similar to the Nvidia cadence, ever Q is more and will be same for many many quarters. -

Last night SK Hynix fell 12% in Korea and MU is off 8% in sympathy - i.e no valid reason

The Koreans like a bit of gamble and apparently margin trading is getting a bit out of hand, 40B USD in extended broker margin mainly on what they call 'ant'(small) retail investor accounts and in particular older investors which isn't to be encouraged. But what it creates is abnormal momentum behind certain assets. So the regulator stepped in and limited this activity and big surprise the stock fell.

The only relevance is it reminds investors that moves down(sharp) can occur. Anyway MU is back to its price yesterday and will report earnings tomorrow

-

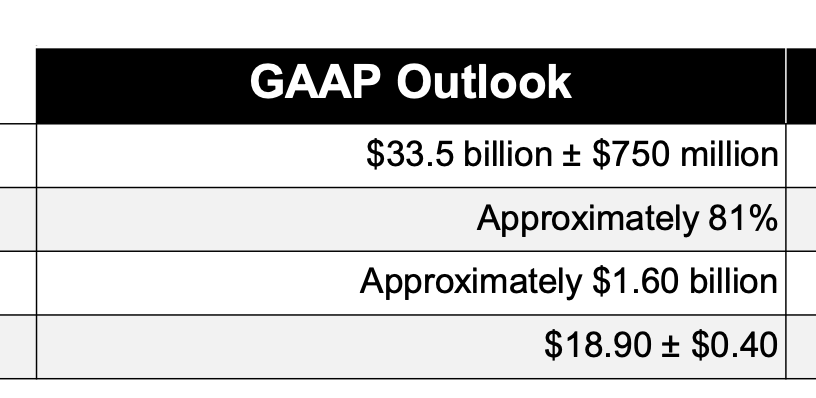

Micron are scheduled to report fiscal Q3 earnings tomorrow after the close

The guide was provided whilst reporting Q2 results of $24B/$12, so guidance was extremely high, +40% QoQ(revenue) and almost 60% on EPS-Quarter to Quarter, not annual.

The higher analyst expectations sitting at $35B and $20.50. I think even this is too low. It's just my opinion but based on what ive observed this quarter I think late 30's, $38-$39B whilst extreme, is possible and around $23-$24 EPS. Margins expected in the 83-84% range.

What I want to hear about is managements long term view on the NAND,DRAM markets, details on additional LTA's, ideally that demand is growing such that the ability to supply is less that the '50% to 2 3rds' quoted previously, that margins are expected to remain elevated.

Updates on HBM4 yield/bit growth and transition to the 1 gamma node being on track or even ahead. Greenfield site updates and roadmap.

Maybe even a stock split-it's something id like to see although technically has no real value based impact, it does improve access and liquidity.

️

️