Micron Technology

-

Some memory stocks have gone up over 20X in the past 12 months and their valuations look modest-still

But you wouldn't even know about it if you weren't an Nvidia HPC believer. And look at Nvidia, lower PE than Coke, Walmart, Mcdonalds. Patience is a virtue-although no complaints here

-

Legacy DRAM shortages in SSDs are becoming severe (think sandisk). The three major DRAM makers(think Micron), which can self-supply legacy DRAM (DDR4) used in SSDs(they can produce their own), will gain a structural advantage in NAND as well(think historically MU has an advantage in DRAM, SNDK in NAND). However eSSD (critical) requires both and SNDK is tapped out-having to buy the memory components it does not produce on the open market. Micron can supply its own! Edge to Micron. We are in some sort of memory utopia

-

Trendforce just revised April DRAM contract price forecasts even higher. They bumped DDR5/DDR4 up by +18% and +23% respectively vs. the March estimates.

The contract prices to be announced at the end of April are expected to hit $37.5 for both DDR5 and DDR4 — that's +27%/+21% MoM gains.

Margins can only keep rising well into the 80s. Nice

-

Taken from the companies prepared remarks. Ignore the currency and focus on the percentages.

SK Hynix posted its highest-ever profitability in Q1, driven by an unprecedented memory supercycle. The operating margin reached 72%, placing the company among the top tier of global manufacturers. SK Hynix is highly likely to deliver record profitability again in Q2, as DRAM and NAND prices continue to climb and shipments expand with a shift toward higher-value products.

According to industry sources on the 23rd, SK Hynix is expected to set a new all-time high operating margin in Q2 on the back of the continuing memory supercycle.

In Q1, SK Hynix reported revenue of KRW 52.5763 trillion and operating profit of KRW 37.6103 trillion. Revenue rose 198% YoY and 60% QoQ, while operating profit jumped 405% YoY and 96% QoQ.

These results mark a record high for the company.

Memory bit growth in Q1 was limited — DRAM was flat QoQ and NAND declined roughly 10% QoQ. However, average selling prices (ASP) for DRAM and NAND rose by the mid-60% and mid-70% range respectively, driving a sharp expansion in profitability.

This was supported by rising demand for high-value server memory tied to AI infrastructure investment. Notably, excluding HBM — where price volatility is limited — commodity DRAM ASP is estimated to have increased by around 100%.

Q2 earnings are expected to expand further, as volume growth and price increases are set to materialise simultaneously.

SK Hynix guided Q2 DRAM bit growth to the high single digits and NAND to the mid-teens, with ASPs expected to continue rising. Current industry estimates place Q2 QoQ ASP increases at roughly 20% for DRAM and 30% for NAND.

A semiconductor industry source said, "Given current conditions, a sharp rise in memory prices through Q2 is all but locked in, and SK Hynix's operating margin is highly likely to set a new record high in Q2."

SK noted that HBM demand will not catch up to supply, at the earliest,- 3 years!

Looking at Micron, which is maintaining bit growth and ASP growth I would expect similar QoQ growth which translates to > $20 EPS for their current Q3 which covers the period March through May (Actually last day of Feb to June 4, although Im modelling 75% QoQ and closer to $23 EPS. Clearly whatever they deliver is expected to be exceeded again in Q4.

-

our model (ultra conservative) intentionally assumes ZERO ASP increases from next Q and would still have EPS grow 25% per annum from a new baseline of >$100 EPS (Likely $115). Where is the growth coming from? Node transition eg 1 gamma. Think of the Wafer as the expensive real estate-

A wafer is a fixed-cost batch of silicon that produces many chips. When process nodes shrink, each chip takes less area, so more dies fit on the same wafer. Smaller dies also tend to have fewer defects per unit, improving yield—the percentage of usable chips. This combination increases the number of sellable chips per wafer and lowers cost per chip. For memory, shrinking also increases bit density, meaning more data capacity per chip.

Micron also benefits from selling 'older' memory which is also in very high demand and with old lines the tooling and R&D is full depreciated which means higher margin! Win-win.

-

During Meta's earnings call. Zuckerberg said. ' “We are increasing our infrastructure CapEx forecast for this year. Most of that is due to higher component costs, particularly memory pricing.” (CEO Zuckerberg)

Good for Micron

-

Sandisk reported last night, beating EPS by $9-expected $15, reported $23 on 78% margins. Consensus guide was $6.5B but they blew that away with $8B at the midpoint and further margin expansion(80%). A guided 50% increase in EPS QoQ-not year. The stock actually came off the boil in AH which seems typical at the moment. The take away, it's a staggering result which bodes very well for the sector.

-

Some industry lingo and implications. 'Samsung strikes LTAs at 0.5

The 0.5 floor refers to Samsung’s minimum guaranteed price (floor) in its long-term agreements (LTAs) for enterprise SSDs (eSSDs), set above $0.50 per GB.LTAs are multi-year supply contracts, typically spanning three to five years, between Samsung and major customers such as cloud providers and hyperscalers. These agreements lock in committed volumes and include pricing protections, often with a floor price to ensure stability for the supplier.

According to recent analyst commentary, Samsung’s LTA floor sits above $0.50/GB. This is higher than expected quarterly pricing — for example, around $0.35/GB in Q2 rising to roughly $0.45/GB in Q3. The elevated LTA floor indicates that long-term contracts are being struck at premium levels compared with shorter-term deals.What this means is that long term contracts are placing a floor ABOVE current elevated spot prices.

NB. Drives like the PM1733a / PM1753 / BM1743 top out at 30.72 TB-that's 30,720 GB or > $15k. I'd estimate the manufacturing cost is somewhere between 2.5-$3k. Nice margins.

-

CEO Sanjay Mehrotra-fireside chat on Friday said......

The shift in AI memory TAM from a projected $100B by 2030 to roughly $100B today highlights how quickly expectations have been overtaken by reality. Sanjay Mehrotra pointed out that demand—especially tied to generative AI—has accelerated far beyond what the industry modeled even a year ago. Training large models was the initial driver, but inference at scale is now compounding the need for high-performance memory, particularly HBM. As a result, Micron Technology and peers are repositioning around a much larger opportunity. Mehrotra’s updated view of a $300B TAM by 2030, with potential to reach $600B longer term, reflects the assumption that AI becomes deeply embedded across cloud, enterprise, and edge environments.

NB-These projections depend on sustained investment but the takeaway is extremely bullish. He is always fwd looking(a long way) based on customer feedback and ordering.

-

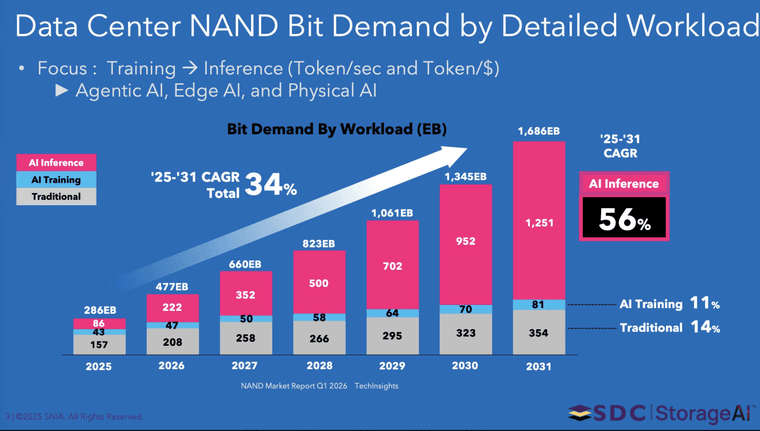

Interesting forecast-NB this not total memory, just NAND- not HBM(DRAM). At today's prices 1686EB would be north of 1 Trillion USD. So adding DRAM we arrive at a forecast of 1.6 $T. Looks like early innings

-

We are rebalancing today, a timely opportunity to trim the surplus weight from Micron having touched $650 earlier

We purchased the holding in Feb 25 for $89.82

NB we are trimming it NOT selling is.

-

Thanks for the heads up, are you buying into any other tech stocks. Thanks

-

Hi Jason,

Tweaks at the last rebalance(yesterday). It's more a case at the moment of looking at some holdings, Meta for example and determining that given its growth the market is discounting it unjustly. If you look at what is happening lately money is flowing into some areas, leaving others out of favour which is fine if that is based on fundamentals however in MSFT/Meta's case I would take the view that growth is up, EPS is up but the stock is down. All we have to do is(if correct) add more weight to these and reduce a bit elsewhere.

I'm always looking at new ideas but it takes time to get comfortable with the business. Often the best opportunity is the one you currently hold- you get to know them very well and sometimes you think 'opportunity'. Stocks are almost always mispriced-some too high, some too low. Look at Micron, from 450 to 319(30 march) and today it's $650. That is an unusual situation however the principles are solid. If the evidence says hold, you do so. Never let a score board (tail) wag the dog(investor). We have been talking about its ridiculously cheap price for 6-9 months- we didn't get lucky. We did the work and it paid off handsomely. Patience is key.

If anyone wants to discuss they are welcome to contact me.

Regards

Adam

-

Thanks Adam for the reply, im always interested in the tech stocks we hold and there progress.

Keep up all the good work the numbers are good.

Kind regards Jason. -

Tbh I struggle with Meta. Yes, it looks cheap in many ways but unlike most other PHT constituents their revenue stream is very narrow and entirely ad driven (as far as I know). There is no product as such. They are completely reliant on increasing user numbers and improving targeted ads etc. Personally I don't consider it at significant discount but I hope to be proven wrong.

-

New eSSD hits the market

The launch of Micron’s 245TB 6600 ION SSD is a significant milestone for the data-centre industry because it pushes flash storage into territory traditionally dominated by hard drives. At 245 terabytes per drive, operators can dramatically reduce rack space, power usage and cooling costs, which matters enormously as AI workloads consume ever more infrastructure capacity.

The drive uses PCIe Gen5 and NVMe, with sequential read speeds of roughly 14GB/s and write speeds around 3–7GB/s depending on configuration. Random performance is also far higher than conventional HDD arrays, while latency is vastly lower. The SSD is built using Micron’s latest QLC NAND technology, prioritising storage density over ultra-high endurance.This could become a major revenue opportunity. Hyperscalers, AI cloud providers and enterprise customers are all racing to expand storage for training data and inference systems. Even at an estimated price likely exceeding US$20,000 per unit initially, the economics can work because one drive can replace large numbers of hard disks and associated infrastructure.

-

My thoughts.....The monetisation case for WhatsApp is potentially one of the largest untapped platform opportunities in global technology history.

Right now, WhatsApp is structurally under-monetised relative to its scale. Meta effectively owns the communication layer for huge parts of the developing world. In countries like India, Brazil, Indonesia, and Mexico, WhatsApp is not just messaging infrastructure — it is social identity, customer support, commerce discovery, and increasingly business infrastructure.I wouldn't be surprised if the company starts producing physical AI products including robots. The data they collect and their analytics of same is the reason they achieve the highest $ (advertising rates) of any platform in the world.

Meta's product is their users-they are very sticky. They aren't going away. Based on fundamentals their growth and earnings power(formidable) would tell me their stock is under valued.

-

Interesting comments about WhatsApp. I've often pondered how they make money for it; you're confirming that they don't.

If their long game is using data for their AI robotics piece then how will they harvest that data, given it's all encrypted and very secure (or so they tell us)?

️

️