Micron Technology

-

So good you said it twice

Thanks for the updates, @Adam-Kay

@2BToo - I like tech to earn it’s cost, but I also like a lot of it…..fairly invested the fruity company, so finally upgraded my 12Pro model for the 17Pro, mostly for the camera (I can find pics of family & friends for any occasion, plus holidays are well documented).

Guess I help keep these tech companies rolling in my own little way. -

Agreed on the usual big draw(for me too) is the camera, otherwise a phone is a phone and I tend to change it when the Apps I use start being unsupported and the battery is worn out. Apple products are a premium, I must put 15 hours a week into the iPad Pro and have done for 8 years and it's still fine. Whilst no longer in use my old iMac lasted for 12 years before I changed it last year. Maybe ive been lucky but reliability, durability has been flawless.

-

This analyst seems even more optimistic...not long to wait now (Wednesday)

Micron (MU) continues to garner positive sentiment ahead of its Q2 earnings next week. Brokerage firm GF Securities just upped its price target on the stock to $571.

In a note to clients, analyst Jeff Pu reasoned “We now forecast DRAM contract prices to rise by 100% in 1Q26, followed by >30% QoQ in 2Q26 with further upside given current asking prices in 50-60% range. For Micron, we forecast FY2Q26 revenue to be $23B with [a] gross margin of 77%. Looking ahead, we expect 3Q26 revenue guidance to be $29B and a margin further [to] grow to 83%.NB. Guidance was $8.40 eps on $18.5B revenue with 68% GM.

-

Things are busy at MU HQ.....

Micron Technology has announced plans to expand its newly acquired Tongluo site in Taiwan with a second chip manufacturing facility focused on DRAM and high-bandwidth memory (HBM). The acquisition of the site from Powerchip Semiconductor Manufacturing Corporation was valued at USD $1.8 billion and includes around 300,000 square feet of existing 300mm cleanroom space.

The expansion will add roughly 270,000 square feet of additional cleanroom capacity, with construction expected to begin by the end September 26. Production from the existing facility is anticipated to begin around fiscal 2028, meaning the expansion will not materially affect near-term DRAM supply. -

Interesting GTC presentation yesterday....

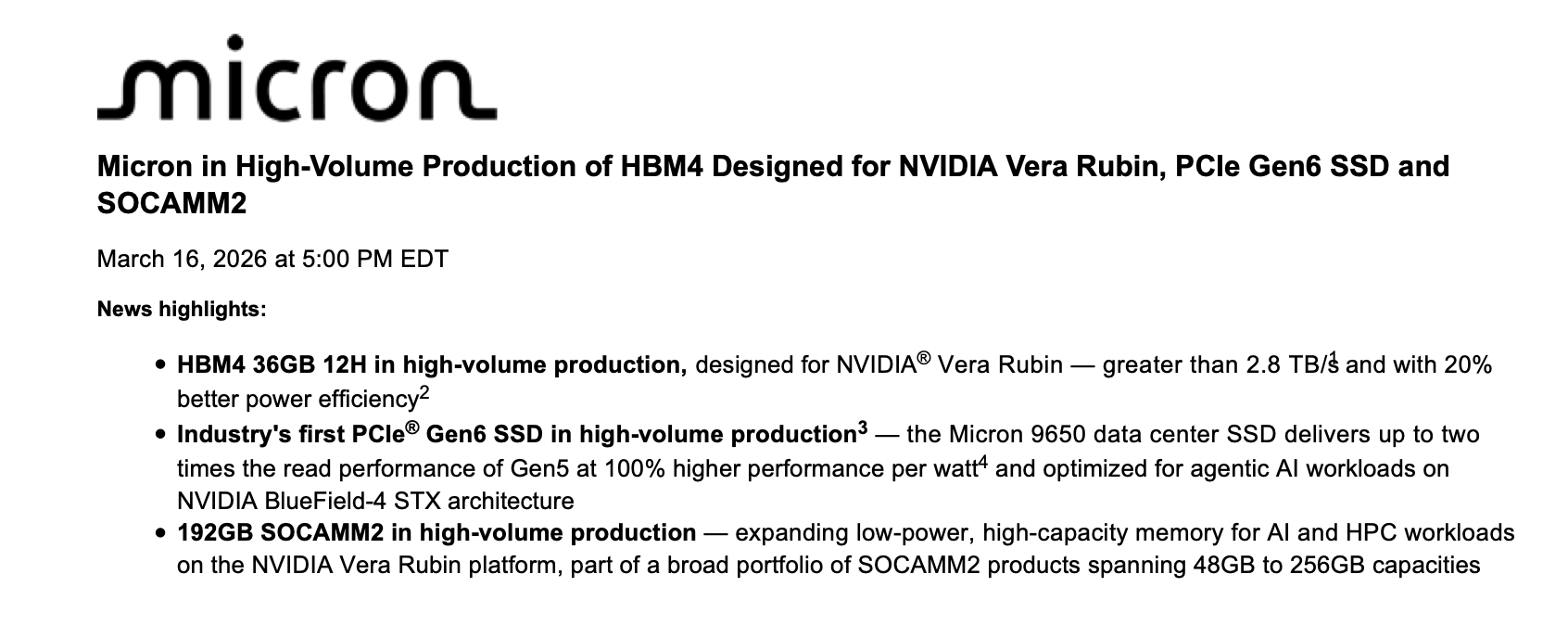

You may recall the rumour mill being promulgated by 'Taiwan'-MU excluded from Nvidia Vera Rubin. We said at the time it was untrue and yesterday the CEO slammed the door and put it to bed.The announcements now confirm that Micron’s HBM4 is indeed in high‑volume production for NVIDIA’s Vera Rubin platform. Micron publicly stated at GTC 2026 that its 36 GB 12‑high HBM4 designed for Vera Rubin is shipping in volume and was already moving into customers’ hands in Q1 2026. That directly contradicts the “Micron is excluded” narrative that surfaced in some Taiwan industry blogs and speculative supply‑chain snippets.

Those Taiwan “news rags” have a long track record of recycling unsubstantiated hearsay, quoting unnamed sources about supply shares, “Micron being sidelined,” or shipment delays — often without follow‑up confirmations. In this case, Micron’s own statements and multiple confirmed wide‑coverage reports show those rumours were just that: rumours, not facts. The market has now moved past speculation and onto actual production and supply confirmation.

Micron îs also sampling 16 high HBM4 ahead of everyone else!

Weak minded investors lost billions, believing these reports-so their plan succeeded-as we have mentioned before, the media has form writing hit pieces at the behest of short sellers.

-

What we have been saying for the past year....happy days

SK Group Chairman Chey Tae-won: “Chip supply shortages will persist through 2030… a price stabilisation plan will be announced soon.”

SK Group Chairman Chey Tae-won said the global memory chip shortage is likely to persist for another four to five years, lasting through 2030.

-

here is the proof-from Microns investor relations portal....

-

Earnings tonight-and they will be spectacular. However the reaction is a function of Options strategy

Micron is a textbook example of how options flow and dealer hedging can dominate short-term price action.

Before earnings, traders aggressively buy call options to bet on upside. Dealers who sell those calls hedge by buying stock (delta hedging), which creates real upward pressure (observed!). As the stock rises, the options’ delta increases, forcing dealers to buy even more shares (gamma effect). This feedback loop is why MU often rallies sharply into earnings.

By the time earnings arrive, positioning is crowded and dealers are heavily long stock as a hedge. The key shift happens after the event: implied volatility collapses, call options lose value, and traders either close positions or let them decay.

Dealers no longer need their hedge.

So they start selling the stock they previously bought.

That creates mechanical selling pressure — regardless of how good the earnings actually are. This is why MU can drop even after strong results: the “hedging bid” disappears.

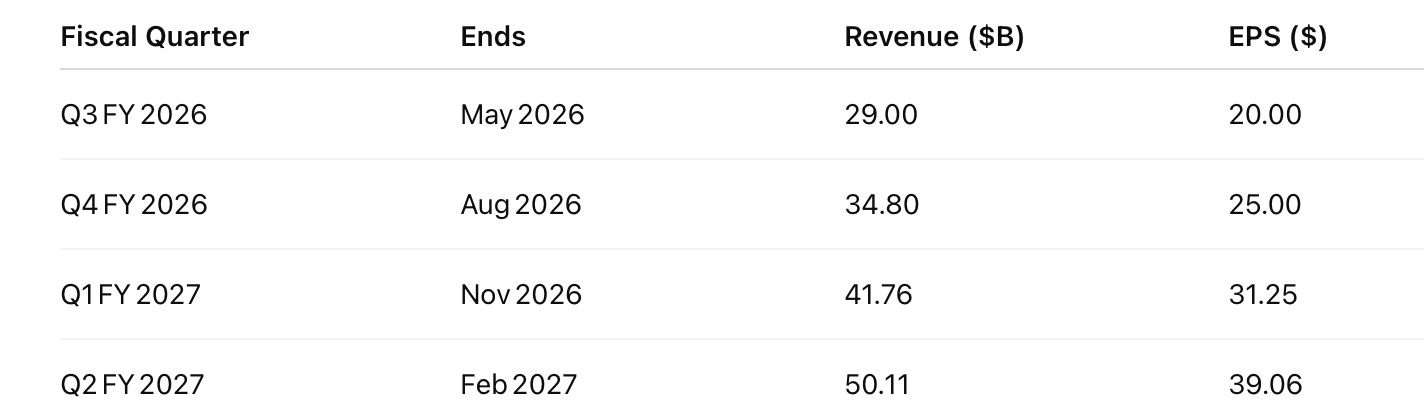

In short, MU’s volatility isn’t just fundamentals — it’s driven by options positioning. Heavy call buying pushes it up pre-earnings, and the unwind of those hedges often pulls it down after.All I care about is the result and the guide (not whether the stock gains or loses 10%)-we will see if they get anywhere close to $11-$12 EPS on $23B and guide $27B and $15. Whatever the guide is it will be low-balled.

NB-the stock entered 2026 at $285 and in PM today it is $475! It was also below $400 only 6 days ago-no one knows what the reaction will be and it is irrelevant because the environment and Microns elite position within it can only mean continued record results as far as they have visibility. It would be nice if management mention contracts locking in 2027 supply-possible.

Imo the company will earn close to $100 over the next 12 months starting next Q and given we paid just under $90 13 months ago it just goes to show you how the market can misprice some assets. I think the actual results for the next year will look something like this:

-

What we want to see tonight is EPS > $10.50. Too hard to say what they will report beyond that. Potential for over $11.

Revenue > $22B

Guide-id be happy with anything +4B over the Q2 actual and an EPS +$3.50 over the Q2 actual. say circa $26B/$14...Their Guide was $18.7B and $8.40 EPS so the above would be a colossal beat.

-

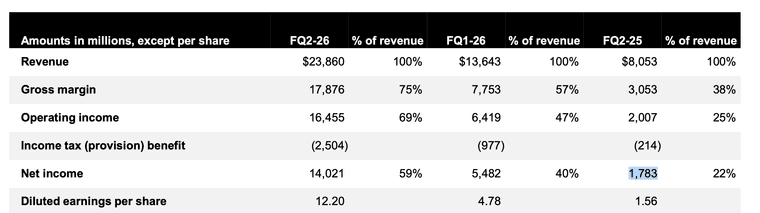

Results are in. 24b and $12 eps. The guide is $33.5b and $19. No other way to describe it but.

-

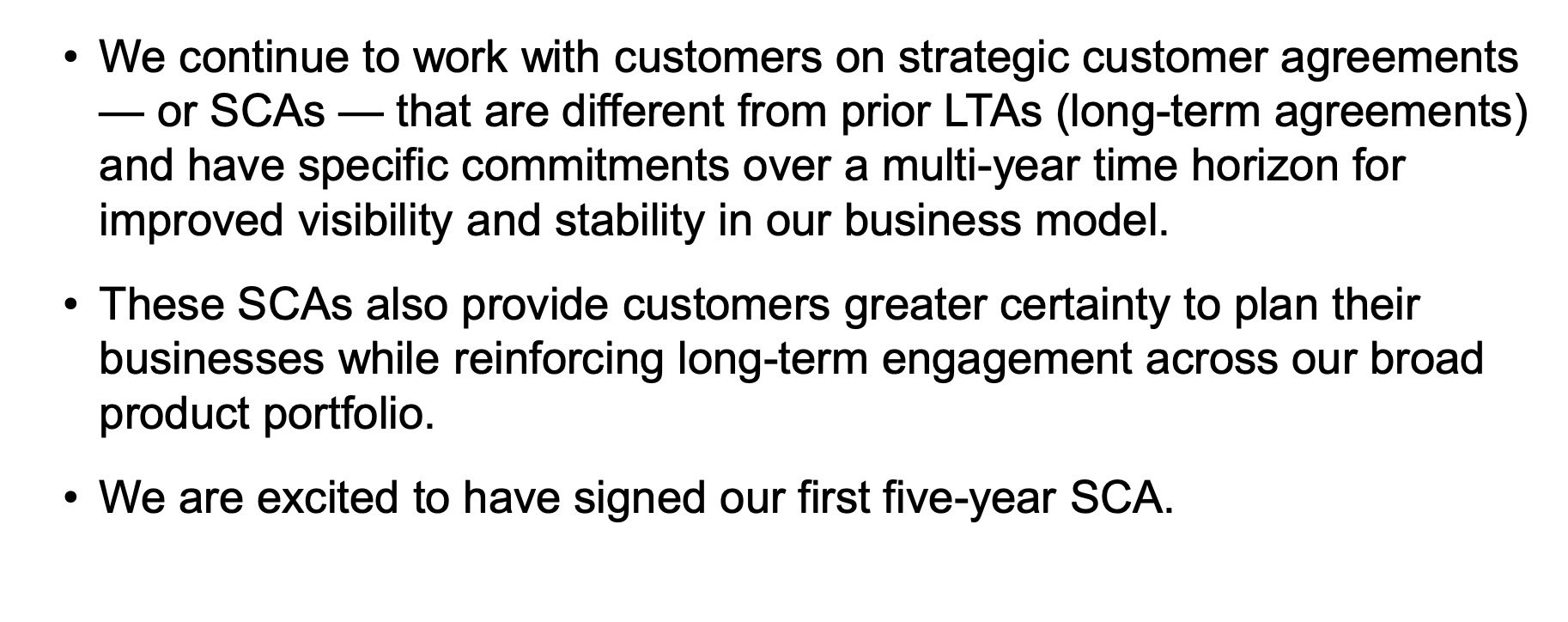

All you have to know really-from prepared remarks .For context, this isn't a 'we are sold out for 2026'. The SCA is a 5 year supply contract. Micron won't say but it points to Nvidia with 'many other SCAs are in progress'. I would speculate that pretty soon it's al going to be sold out for years.

The language used is intentional. One can interpret 'foreseeable future' however they choose depending on bias. My interpretation is 'years'. The fact remains all planned greeenfield sites globally, across all manufacturers will see bit growth in the 25-30% range whilst demand is 100% greater at least on the same annual basis. And this does not take into account level 3 and level 4 autonomous vehicles nor robotics which are coming and will need significant memory (edge devices).

Broadly speaking-if we are in a constrained environment we can expect ASP to continue to move up in the 50% range annually and coupled with bit growth of 20-25% and better yield (lower cost), the result is 70-80% revenue growth, margin growth and operating leverage continuing for the foreseeable future.

Of course if you don't believe spending on data centres will continue, we've peaked.

-

686% growth in net income

195% increase in RevenueFwd PE is around 4!

I agree that Data centre(racks) may not be the biggest long term driver. Edge cases are likely to be larger opportunities

-

Hi Al,

The same market priced the stock at $90 a year ago so it's really all you need to know about how efficient it is at times. The current situation is, and not too dissimilar to nvidia, they think it's peaked and the party is over. I think they are wrong and not slightly wrong either. The SCA 'with a very large customer' is an industry first and changes the landscape by giving certainty to Micron that a customer is contractually locked-in to buy large quantities for 'years'(5 in this case). That is not a trivial development. And let's face it, others will now get worried and also lock in long term deals or face exclusion.Remember two weeks ago when Jensen said 'we have secured our supply chain'

I am highly confident we won't stay at these levels for long. Analysts will certainly update their models this week as well.

The deal would look something like this:

Core Deal Structure

Size & Term: ~$100 -$130 billion over 5 years, covering HBM4e, HBM3e, and potential HBM5 supply for NVIDIA’s Vera Rubin AI and future GPU platforms.

Payment & Guarantees: NVIDIA commits to minimum annual purchase volumes (~$25 billion/year). Payments include base contract pricing plus potential escalators tied to wafer costs or memory market spot-rate increases. Shortfalls in volume may trigger penalties or make-good clauses to protect Micron.

Benefits:

For NVIDIA: Secures long-term HBM supply at hyperscale, ensures priority access, and hedges against extreme spot-market volatility.

For Micron: Guarantees $130 billion revenue over five years, improves production planning, and shares some market risk with a major customer.

Flexibility & Technology Alignment: Volumes and HBM generations may adjust over the contract to match AI demand growth, with co-optimisation of HBM designs for NVIDIA GPUs. -

Hi Al,

The same market priced the stock at $90 a year ago so it's really all you need to know about how efficient it is at times. The current situation is, and not too dissimilar to nvidia, they think it's peaked and the party is over. I think they are wrong and not slightly wrong either. The SCA 'with a very large customer' is an industry first and changes the landscape by giving certainty to Micron that a customer is contractually locked-in to buy large quantities for 'years'(5 in this case). That is not a trivial development. And let's face it, others will now get worried and also lock in long term deals or face exclusion.Remember two weeks ago when Jensen said 'we have secured our supply chain'

I am highly confident we won't stay at these levels for long. Analysts will certainly update their models this week as well.

The deal would look something like this:

Core Deal Structure

Size & Term: ~$100 -$130 billion over 5 years, covering HBM4e, HBM3e, and potential HBM5 supply for NVIDIA’s Vera Rubin AI and future GPU platforms.

Payment & Guarantees: NVIDIA commits to minimum annual purchase volumes (~$25 billion/year). Payments include base contract pricing plus potential escalators tied to wafer costs or memory market spot-rate increases. Shortfalls in volume may trigger penalties or make-good clauses to protect Micron.

Benefits:

For NVIDIA: Secures long-term HBM supply at hyperscale, ensures priority access, and hedges against extreme spot-market volatility.

For Micron: Guarantees $130 billion revenue over five years, improves production planning, and shares some market risk with a major customer.

Flexibility & Technology Alignment: Volumes and HBM generations may adjust over the contract to match AI demand growth, with co-optimisation of HBM designs for NVIDIA GPUs. -

It was a Trig moment, calling Rodders 'AL'

-

Dan Ives(analyst) said today...The increasing demand and tight supply of memory for artificial intelligence infrastructure buildouts will prompt prices of some memory types to surge by more than 100%, according to Wedbush.

"Not surprisingly, pricing for memory continues to lift aggressively, with DRAM and NAND likely to see 1H (means first half 2026) pricing increases well into the triple digits from CQ4'25 levels, with gains for the former likely approaching 130% - 150% and the latter nearly as robust," said Wedbush analysts in a Monday investor report.

This should bode well for memory makers such as Micron Technology (MU), Seagate Technology (STX), and Western Digital (WDC).

"No one should be surprised by an improvement in memory," Wedbush said. "However, the magnitude of the spike highlights how much markets have continued to improve as Q1 has progressed and certainly fits our recent positive checks around memory and MU's robust results and guidance."

"And we believe, given both this backdrop as well as further shortfalls in supply vs. demand, that HDD vendors are looking to price their future contracts more aggressively than they have previously suggested," Wedbush noted.

")