Micron Technology

-

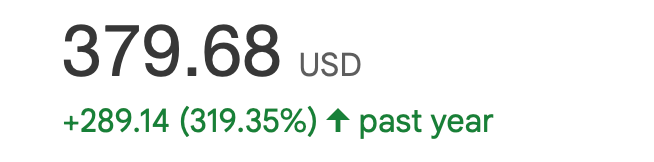

The fact it was $90 a year ago. It's as simple as the parabolic short duration being pre disposed to a bigger than avg move down when investors(I use that term loosely) get nervous. They report 2 weeks tomorrow.

The expectation is about $8.36 EPS. I think they'll deliver $11-earnings not expected for 3 more quarters. Fwd PE of about 7 with growth TTM 100%, at least 50% CAGR 5 years(PEG =0.14) OR you too can buy Crowdstrike with a Fwd PE of 60 and 15% growth (PEG=4). On this metric the stock is over 50X more expensive than Micron.

The expectation is about $8.36 EPS. I think they'll deliver $11-earnings not expected for 3 more quarters. Fwd PE of about 7 with growth TTM 100%, at least 50% CAGR 5 years(PEG =0.14) OR you too can buy Crowdstrike with a Fwd PE of 60 and 15% growth (PEG=4). On this metric the stock is over 50X more expensive than Micron.If you look at Micron it traded sideways from feb through May moved to $120 sold offa. bit (what happened), well it got stronger but people sold, thinking it was done and all stocks encounter selling at new levels because that's what people do. The problem is those same people just look at a price and make a decision. It was only 10 months ago that Nvidia fell from $125 to $89 on nothing but great news and 2 days later it was $115 over 25% in 2 days. We have seen this sort of thing countless times-it's human nature. When stressed some people do foolish things and more rational investors take advantage of the situation.

The only risk for Micron is they fail to execute on their roadmap and 50 years experience suggests that risk is tiny. Demand is growing 70% per annum for their products(lets call it 50%) and is expected to be the same for at least 5 years and probably 7+ (so says people I trust Wei/Huang). Bit growth(supply) can not keep up and will not because you can not magic up a fab in months. It take years, so it is obvious the imbalance will persist for years and prices for memory will keep rising. I say obvious, obvious to me.

The earliest time frame for some sort of balanced supply.demand imo is 2029/30

What you see with a company like Micron, is the old classic 'but it's risen 300% in a year' it cant do it again or it must be time to sell. I would say, tell me why you think that. The price appreciate is influencing ones decision making when in fact it's not of much relevance at all other than some thinking(?) they can cash in and rotate into something else. Good luck with that when the evidence strongly supports continued material undervaluation. Often the best investment is the one you already hold, and personally I like to get overly familiar with my holdings.

All I can say is, in all history companies with 50% annual growth and PEs below 10 don't exist. So on that basis alone I am very happy holding and waiting. And given we paid circa 1X next years earnings, maybe 1.5, we have a comfortable margin of safety.

-

If you believe nvidia will sell more racks next year than this year and Vera Rubin uses much more than blackwell. A top tier blackwell rack uses 192GB of memory, a Vera Rubin rack uses 300GB+ and Feyman will use > 500GB. And more racks will be sold so demand is:

TrendForce's 70% YoY demand growth in 2026; Goldman Sachs' 77% in 2026 and 68% in 2027), demand is indeed "a lot higher" supply-focused estimates—potentially 70-100% YoY bit growth (demand) through 2027, driven by GPUs (NVIDIA/AMD) and ASICs (e.g., Google TPUs, custom chips). Bit growth(supply) is estimated 35% in 26, 50% in 27 and 45% in 28. That is a very big imbalance which can only mean prices go up and there is a fight over who gets the silicon

The racks will get built but someone is going to be left without any supply and it won't be Nvidia imo because they have all the money to advance purchase whatever they need. AMD don't.

I've alluded to it before-HBM is the most critical component and the most scarce. I won't say what I think the stock is worth but I think a PE of 25 is not unreasonable, I also think the market is under estimating the EPS figure materially. Only months ago the experts thought it would earn $17 in 2026 total and it's closer to $50 this year and $75+ (maybe much more in 27).

-

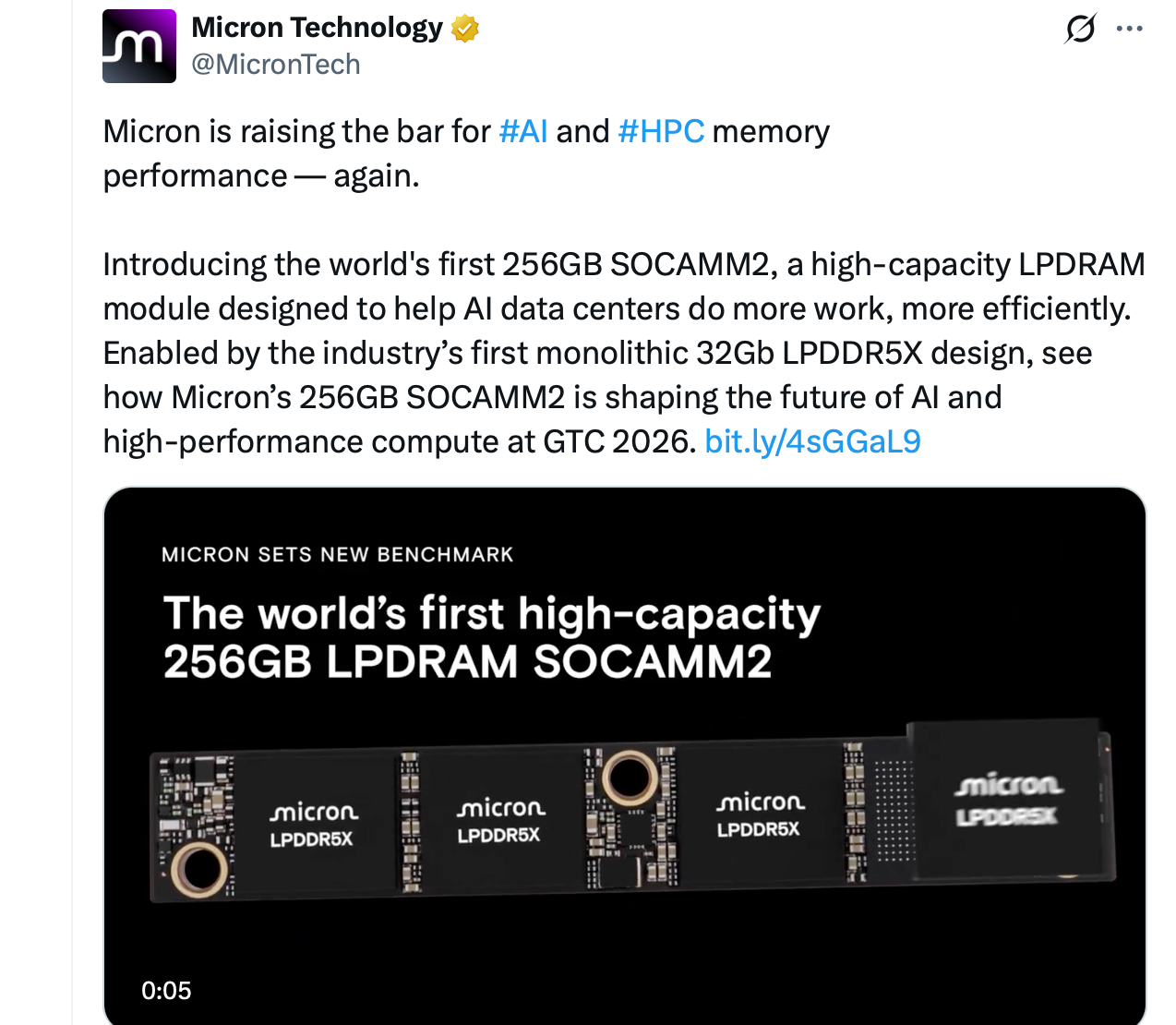

And just in. A new product and worth double digit billions-every one sold

-

What a difference a day makes-almost back. Must have read my post

-

@Adam-Kay said in Micron Technology:

What a difference a day makes-almost back. Must have read my post

I don't think I could ask for a better response to my eMail of yesterday!

Thanks for the explanation, and for tweaking the share price up as you did. (

)

) -

Micron Technology received two bullish analyst updates today, reinforcing positive sentiment around the memory chip cycle.

Citigroup, led by analyst Atif Malik, maintained a Buy rating and raised its price target to $430 from $385. The firm expects continued strength in memory pricing, driven largely by accelerating demand for AI infrastructure.

Meanwhile Susquehanna, through analyst Mehdi Hosseini, reiterated a Positive rating and lifted its price target sharply to $525 from $345 — a significant increase reflecting stronger long-term expectations for memory demand.

Analysts broadly believe the AI boom is tightening supply of advanced memory such as high-bandwidth memory (HBM), which is essential for training and running large AI models. This demand is supporting forecasts for rising DRAM prices over the next year. -

The big price hikes are in the HPC area with some spill over into consumer electronics segments mainly because manufacturers are prioritising HPC leaving undersupply in other consumer areas. However the market is highly competitive and efficient and generally tech gets cheaper.

I think for what it is this is a big deal for Apple and the consumer.

-

Ha! I've never spent as much as £599 on a single piece of tech in my entire life; I doubt the sum total of what I've spent on tech in the last 50 years tops £1200. But then I'm cheap, and I like to make old things last, and I get a perverse kick out of taking old tech out of other people's bins and making it last for another five years ....

Perhaps I'm weird, but spending £600 on a computer seems like a kings ransom!

-

Sir Chomps is a friendly boy, really

-

Applied Materials and Micron Technology have announced a strategic partnership to develop next-generation memory technologies for artificial intelligence. The collaboration focuses on advancing DRAM, High-Bandwidth Memory (HBM), and NAND by jointly working on new chip architectures, materials and semiconductor manufacturing processes.

The partnership will be centred around Applied Materials’ EPIC research centre (cool name), a major semiconductor innovation hub designed to accelerate the transition from research to large-scale manufacturing. Applied Materials is investing around $5 billion in the facility, providing the infrastructure for collaborative semiconductor development. Micron’s contribution will come through engineering teams, joint R&D programmes and its existing memory innovation centres.

By combining Micron’s expertise in memory chip design with Applied Materials’ leadership in semiconductor equipment and fabrication technology, the two companies aim to develop faster, more energy-efficient memory specifically optimised for AI workloads.

The timing is significant because AI systems increasingly face a memory bandwidth bottleneck. Modern AI accelerators from companies such as NVIDIA require extremely high-speed memory like HBM to keep powerful processors supplied with data.

Micron has reacted positively to the news!

-

Just speculating but I model the impact of the price increases. The MU guide factored in 'ASP +bit growth cumulative' of 41% however on avg ASP is 50% above this. Could they....

It's very difficult to have any real handle on numbers because there are so many moving parts and the pricing is changing so rapidly. But they will materially beat and likely guide higher again. My scenario is not priced in. Wallstreet consensus is $18.7/$8.60! Whilst my model is aggressive, Wallstreet is wrong for certain imo.

-

Lots of Micron news flooding in. Impressive stuff...

50% overnight hike in NAND flash prices (as highlighted by Phison and industry trackers) is proving exceptionally positive for Micron Technology.This surge, rooted in acute supply constraints and explosive AI infrastructure demand for enterprise SSDs, directly enhances Micron's profitability.

Margins will expand with earnings, driven by products like G9-based PCIe Gen6 SSDs and massive QLC models (122TB/245TB) qualifying at hyperscalers (those a simply massive solid state drives). And to give you an idea the 50% is a blended 'nand' price price. Cutting edge drives EG 122TB QLC was quoted $12,400 and jumped to $37,000, almost over night. Hard to get your head around that

The pricing power from the shortage lifts average selling prices sharply (NAND ASPs projected to rise ~127% in 2026), boosting gross margins and free cash flow. Micron has pivoted away from lower-margin consumer segments (exiting Crucial brand) to prioritise enterprise/data centre allocations, gaining market share amid tight supply.

Earnings next Wednesday. It will be explosive imo.

-

So good you said it twice

Thanks for the updates, @Adam-Kay

@2BToo - I like tech to earn it’s cost, but I also like a lot of it…..fairly invested the fruity company, so finally upgraded my 12Pro model for the 17Pro, mostly for the camera (I can find pics of family & friends for any occasion, plus holidays are well documented).

Guess I help keep these tech companies rolling in my own little way. -

Agreed on the usual big draw(for me too) is the camera, otherwise a phone is a phone and I tend to change it when the Apps I use start being unsupported and the battery is worn out. Apple products are a premium, I must put 15 hours a week into the iPad Pro and have done for 8 years and it's still fine. Whilst no longer in use my old iMac lasted for 12 years before I changed it last year. Maybe ive been lucky but reliability, durability has been flawless.

-

This analyst seems even more optimistic...not long to wait now (Wednesday)

Micron (MU) continues to garner positive sentiment ahead of its Q2 earnings next week. Brokerage firm GF Securities just upped its price target on the stock to $571.

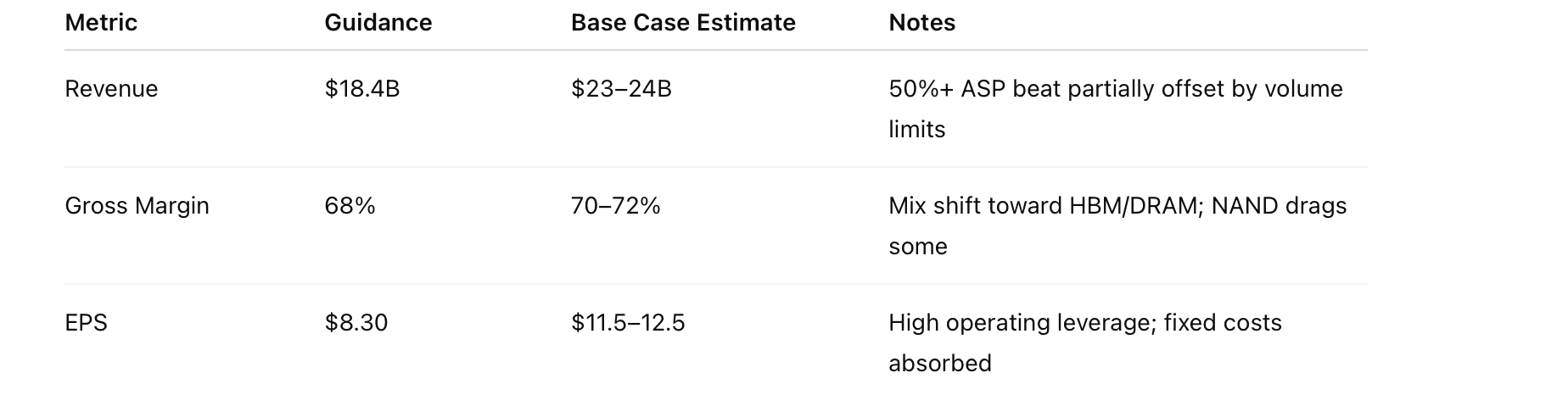

In a note to clients, analyst Jeff Pu reasoned “We now forecast DRAM contract prices to rise by 100% in 1Q26, followed by >30% QoQ in 2Q26 with further upside given current asking prices in 50-60% range. For Micron, we forecast FY2Q26 revenue to be $23B with [a] gross margin of 77%. Looking ahead, we expect 3Q26 revenue guidance to be $29B and a margin further [to] grow to 83%.NB. Guidance was $8.40 eps on $18.5B revenue with 68% GM.

-

Things are busy at MU HQ.....

Micron Technology has announced plans to expand its newly acquired Tongluo site in Taiwan with a second chip manufacturing facility focused on DRAM and high-bandwidth memory (HBM). The acquisition of the site from Powerchip Semiconductor Manufacturing Corporation was valued at USD $1.8 billion and includes around 300,000 square feet of existing 300mm cleanroom space.

The expansion will add roughly 270,000 square feet of additional cleanroom capacity, with construction expected to begin by the end September 26. Production from the existing facility is anticipated to begin around fiscal 2028, meaning the expansion will not materially affect near-term DRAM supply. -

Interesting GTC presentation yesterday....

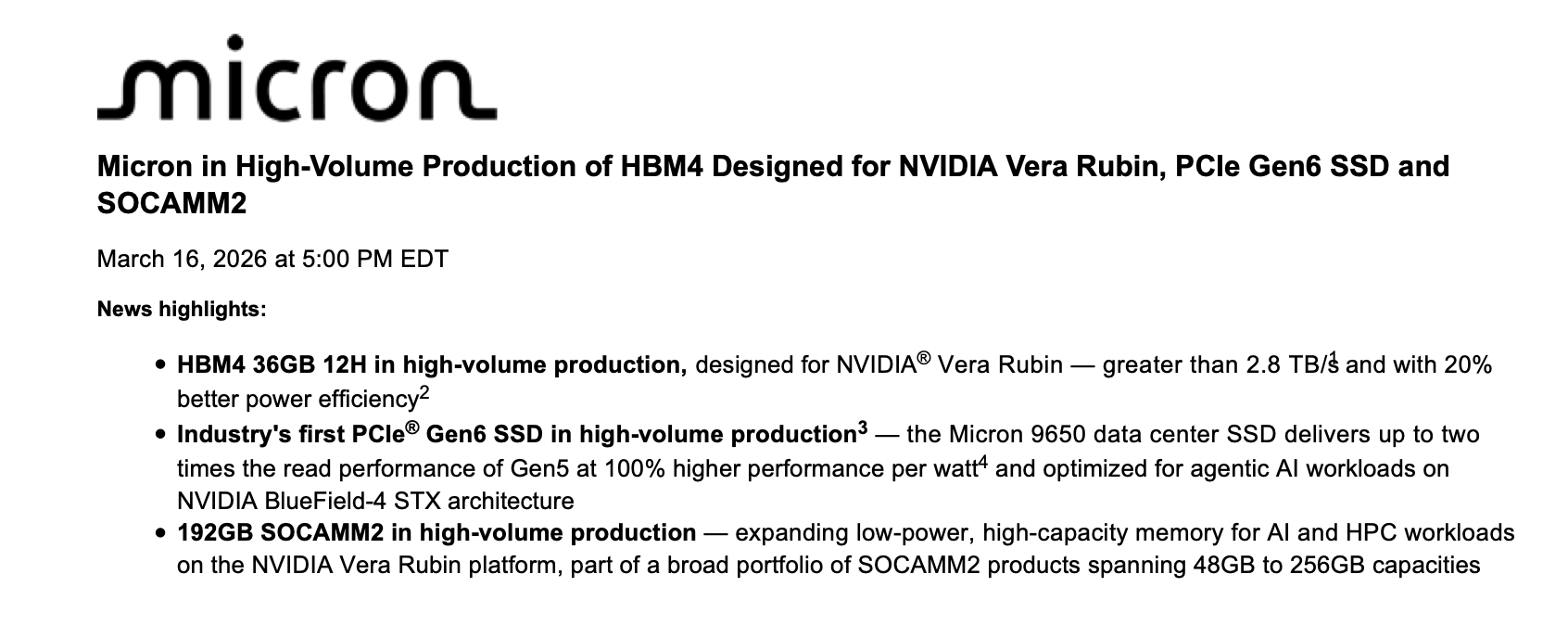

You may recall the rumour mill being promulgated by 'Taiwan'-MU excluded from Nvidia Vera Rubin. We said at the time it was untrue and yesterday the CEO slammed the door and put it to bed.The announcements now confirm that Micron’s HBM4 is indeed in high‑volume production for NVIDIA’s Vera Rubin platform. Micron publicly stated at GTC 2026 that its 36 GB 12‑high HBM4 designed for Vera Rubin is shipping in volume and was already moving into customers’ hands in Q1 2026. That directly contradicts the “Micron is excluded” narrative that surfaced in some Taiwan industry blogs and speculative supply‑chain snippets.

Those Taiwan “news rags” have a long track record of recycling unsubstantiated hearsay, quoting unnamed sources about supply shares, “Micron being sidelined,” or shipment delays — often without follow‑up confirmations. In this case, Micron’s own statements and multiple confirmed wide‑coverage reports show those rumours were just that: rumours, not facts. The market has now moved past speculation and onto actual production and supply confirmation.

Micron îs also sampling 16 high HBM4 ahead of everyone else!

Weak minded investors lost billions, believing these reports-so their plan succeeded-as we have mentioned before, the media has form writing hit pieces at the behest of short sellers.

-

What we have been saying for the past year....happy days

SK Group Chairman Chey Tae-won: “Chip supply shortages will persist through 2030… a price stabilisation plan will be announced soon.”

SK Group Chairman Chey Tae-won said the global memory chip shortage is likely to persist for another four to five years, lasting through 2030.

-

here is the proof-from Microns investor relations portal....