GOOG News

-

An incredible result from GOOG, $28B net income for a 13 week quarter. The stock has done well lately but there is still an overhang from sentiment that the company has anti trust issues and is spending too much on AI. I think these fears are materially overblown.

GOOG reported its second-quarter 2025 earnings on 23 July 2025, showing robust financial performance driven by strong growth in Search, YouTube, and Cloud segments, underpinned by advancements in artificial intelligence (AI). Despite a significant increase in CapEx, the company exceeded analyst expectations, though investor sentiment was mixed due to concerns over rising expenditure (always!)and regulatory challenges.Key Financials (Q2 2025)Revenue: $96.43 billion, up 13.8% year-over-year (YoY), surpassing estimates of $94 billion.

Revenue (ex-TAC-traffic acquisition cost): $81.2 billion, compared to expectations of $79.6 billion.

Earnings Per Share (EPS): $2.31 (adjusted), a 22% YoY increase, beating estimates of $2.18.

Net Income: $28.2 billion, up 19% YoY.

Operating Income: $31.3 billion, up 14% YoY, with an operating margin of 32.4% (flat YoY despite legal settlement costs).

Google Cloud Revenue: $13.62 billion, up 32% YoY, exceeding estimates of $13.11 billion.YouTube Advertising Revenue: $9.8 billion, up 13% YoY, slightly above estimates of $9.56 billion.

Search Revenue: $54.1 billion, up 11% YoY, surpassing expectations of $52.7 billion.

Traffic Acquisition Costs (TAC): $14.71 billion, in line with expectations.

Conference call highlights

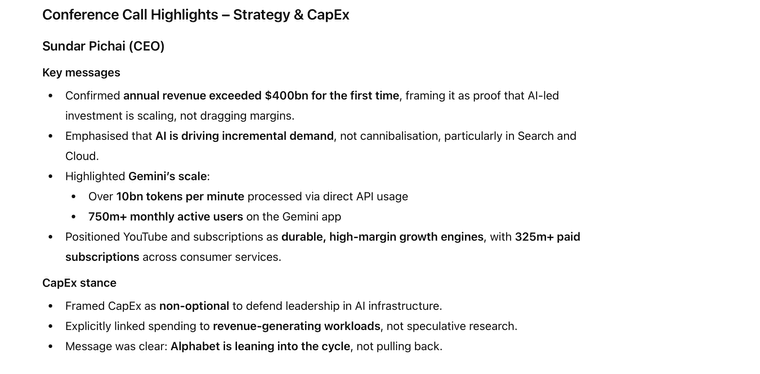

AI-Driven Growth:Pichai emphasised that “AI is positively impacting every part of the business, driving strong momentum.” Search saw double-digit revenue growth, fuelled by AI features like AI Overviews (1.5 billion monthly users) and AI Mode (100 million monthly active users).Google’s Gemini AI model has grown to 450 million monthly users, reinforcing Alphabet’s competitive edge in AI against rivals like ChatGPT.

Google Cloud’s 32% YoY revenue growth was driven by demand for AI infrastructure and generative AI solutions, with an annual revenue run-rate exceeding $50 billion.

Capital Expenditure :Alphabet announced a $10 billion increase in its 2025 CapEx guidance, raising the total to $85 billion from $75 billion, reflecting strong demand for cloud and AI infrastructure.

CFO Anat Ashkenazi noted that Q2 CapEx was $22.4 billion, significantly above estimates of $18.2 billion, primarily for servers and data centres(nice). The increase is driven by a “tight supply environment” for chips needed to train and run AI models.

Ashkenazi highlighted that CapEx is expected to rise further in 2026 due to ongoing demand, but Alphabet is focused on efficient allocation to mitigate profitability concerns. A “highly rigorous process” ensures optimal use of resources.

The increased CapEx raised investor concerns about near-term profitability(we can see profit headwinds NOT), as depreciation costs are expected to accelerate in 2025 due to prior and ongoing infrastructure investments.

Positive Developments:Search: AI Overviews and AI Mode have boosted user engagement, enabling Alphabet to address more complex queries and maintain its dominance despite competition from AI-powered chatbots. Search revenue grew 11% YoY, outperforming expectations.

YouTube: The platform’s ad revenue grew 13% YoY, driven by increased viewership on Connected TV and Shorts monetisation, which now matches or exceeds traditional in-stream ads in key markets. YouTube’s shift to television as its primary consumption medium is eroding traditional network market share.

Google Cloud: The segment’s profitability improved, with an operating margin of 20.7% (up from 17.1% in Q1 2025), reflecting strong demand for AI and core cloud products.

Subscriptions and Other Bets: Subscription platforms (YouTube, Google One) grew 19% YoY to $10.4 billion, with 270 million paid subscribers globally. Waymo, Alphabet’s autonomous vehicle unit, is scaling, serving over 150,000 paid rides weekly.Talent and Innovation: Pichai downplayed concerns about AI talent wars, stating that retention and new talent acquisition metrics remain “healthy.” The company continues to innovate rapidly, with over 1,000 new cloud products and features launched in the past eight months.

After an initial soft after hours reaction, the stock rose a few dollars and futures are up nicely overall.

-

GOOG shares are up circa 6% in PM to an ATH of $293 due to Berkshire Hathaway disclosing a 4-5B investment. Nice to see the stock make gains however it's not particularly rational is it. Berkshire buying the stock is not an exciting event which has much meaning. What do they know. They've ignored the stock for 20 years and now think it's cheap-maybe, but they hardly have a great tech driven record.

-

I was reading about the Space X capital raise at a $800B valuation and they intend to take the company public some time next year at a 1-1.5T valuation based on starlink. Alphabet took a large stake in Space X 10 years ago acquiring somewhere between 7-7.5% equity for only $900M-a little known fact . Todays's valuation puts that at $56B and the IPO could push that to closer to 80-100B. We will see in February when they report just how much unrealised gain they book on the mark to market. Probably 25-30B gain!

-

Musk now talking about putting data centres in space! That would be a game changer.

-

Musk now talking about putting data centres in space! That would be a game changer.

@Coopersale said in GOOG News:

Musk now talking about putting data centres in space! That would be a game changer.

He is obsessed with space.

TBH, more DCs in Iceland would be good enough: low energy cost, simple cooling. Much easier to get the h/w built

-

It's mostly science fiction due to the costs today but it's good to push the boundaries of what is possible-after all, it's how we get there, you have to start somewhere. The next big thing will likely be deployment of humanoid robots at scale within the next 24 months and in terms of usable AI 'autonomous execution' where you set a task and it completes it without additional prompts.

-

Sorry meant to post this with my comment above.

https://x.com/elonmusk/status/2000603814249079165?s=61&t=iHaQYNHaXHYa5fzY9gX_Vw -

Sorry meant to post this with my comment above.

https://x.com/elonmusk/status/2000603814249079165?s=61&t=iHaQYNHaXHYa5fzY9gX_Vw@Coopersale said in GOOG News:

Sorry meant to post this with my comment above.

https://x.com/elonmusk/status/2000603814249079165?s=61&t=iHaQYNHaXHYa5fzY9gX_VwI can see the logic in that. It'll also end the moaning from the MMGW types as it won't release any gases on earth.

-

You have to hand it to Musk-he's a master marketer- it won't be long and he'll set up a real estate agency selling plots for sale on Mars-

-

Interesting analyst comments on Google. You will recall we have been big supporters of the company despite it being unloved for over 2 years prior to Q2 of 2025-the market got it completely wrong by assuming that GOOG was just a search engine at risk of being crushed by anti trust laws(and OpenAI). The reality is, they will likely 'win' the AI race-their decades of investment in moon shots and employing the brightest minds is paying off in spades. They are the most profitable company in the world for now and their valuation is unstretched imo.

Alphabet (GOOG) has become the world’s second most valuable company, overtaking Apple (AAPL) for the first time since 2019, as Google’s parent company strengthens its position at the sharp end of the artificial intelligence race.

Alphabet shares climbed more than 2% on Wednesday, pushing its market capitalisation to USD 3.89 trillion. Apple’s valuation slipped to USD 3.86 trillion after its shares fell 0.8% on the day.

Wall Street analysts say Alphabet’s Gemini model is rapidly narrowing the gap with OpenAI’s ChatGPT, which remains the leading AI platform.

“Looking ahead to 2026, we expect AI to deliver further gains across the consumer business, with Gemini app downloads surpassing ChatGPT and AI Mode and Overviews driving longer user engagement,” Jefferies said.Alphabet stock has surged 64% over the past 12 months. “Supported by robust core businesses, improving cloud momentum and a stronger AI product cycle, we believe GOOGL is well placed to extend its performance,” Jefferies added.

-

Alphabet shares have surged as investor confidence snaps back, driven by clear evidence that Google’s AI strategy is not only defensible, but increasingly lucrative. After months of concern that generative AI would undermine search economics, recent performance suggests the opposite is unfolding.

According to market commentators including Deepwater Asset Management, Google’s core search business has exceeded expectations as AI-driven results prompt users to ask more follow-up questions rather than fewer. That behaviour matters. More queries translate into more advertising opportunities, and Google has moved quickly to place ads both below and within AI-generated responses. Independent testing cited by Deepwater indicates monetisation has improved materially over the past three months, strengthening the outlook for 2026 and beyond.

The company is also pushing aggressively into what it calls agentic commerce. New features allow users to complete checkout directly inside AI Mode, supported by fresh ad formats such as Direct Offers. A partnership with Walmart signals that Google is serious about capturing transaction-level value, not just referral traffic, a shift that could meaningfully lift revenue per user over time.

On the competitive front, Google’s Gemini models have gained traction at speed. Some analysts argue Gemini 3 now rivals, and in certain tasks surpasses, OpenAI’s GPT, a view that has reshaped perceptions of the AI landscape. Momentum was further boosted by reports that Apple has selected Gemini to power upcoming Siri upgrades, displacing rival models.

Alphabet shares are now up roughly 80% over six months, placing the stock among the top performers in the Nasdaq 100. The rally reflects a simple recalibration: Google is no longer seen as an AI casualty, but as a credible AI winner that knows how to monetise at scale.

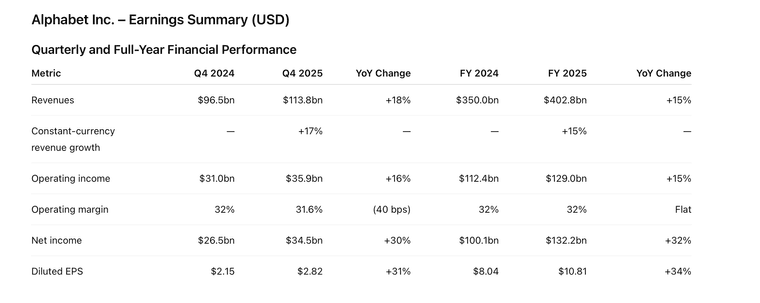

GOOG are expected to report their Q4 and biggest ever earnings on 4 Feb, exceeding $111B revenue (Q) and over $400B annually. A formidable operator with very deep expertise and competence across all things 'tech'. It's quite incredible to think, a company of this scale still growing at high double digit rates.

-

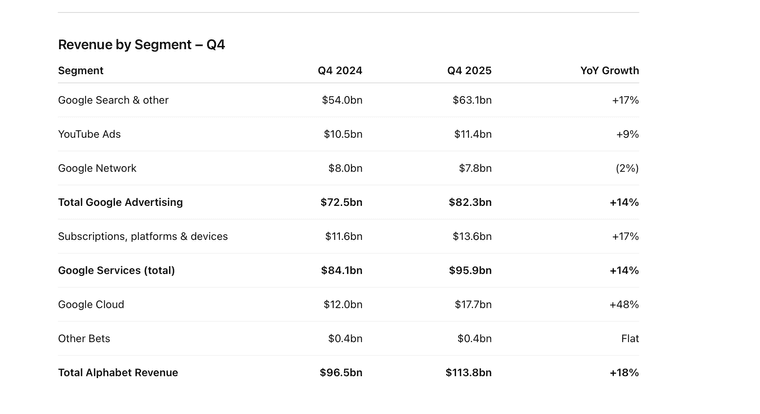

Alphabet report their Q4 earnings tonight after the close. I expect a very strong showing. Close to $115B revenue and around $2.70 eps. All eyes on GCP (Google cloud platform) and YouTube , ad dollars etc. It will be interesting to see if they MTM their Space X holding. I also expect Sundar to talk about how constrained they are and give updates on their TPU/custom Asics solutions plus RPO backlog.

Space X ran a funding round which closed mid Dec, valuing the company at $800B. GOOG last revalued their holding in July at a $420B valuation. We don't know how much they will recognised but it's between $1 and $2 EPS. If you see a headline of $3.50+ you know they revalued their holding.

GOOG purchased 7% of space X for $1B and if the IPO numbers are true, today that holding is worth $105B although they won't recognise that yet(IPO hasnt happened). Nice investment all the same.

Waymo is now worth $120B but as it's a wholly owned subsidiary, there is no MTM as it's operations are simply consolidated the same way every other operation is.

-

Alphabet report their Q4 earnings tonight after the close. I expect a very strong showing. Close to $115B revenue and around $2.70 eps. All eyes on GCP (Google cloud platform) and YouTube , ad dollars etc. It will be interesting to see if they MTM their Space X holding. I also expect Sundar to talk about how constrained they are and give updates on their TPU/custom Asics solutions plus RPO backlog.

Space X ran a funding round which closed mid Dec, valuing the company at $800B. GOOG last revalued their holding in July at a $420B valuation. We don't know how much they will recognised but it's between $1 and $2 EPS. If you see a headline of $3.50+ you know they revalued their holding.

GOOG purchased 7% of space X for $1B and if the IPO numbers are true, today that holding is worth $105B although they won't recognise that yet(IPO hasnt happened). Nice investment all the same.

Waymo is now worth $120B but as it's a wholly owned subsidiary, there is no MTM as it's operations are simply consolidated the same way every other operation is.

-

Mark to Market (revalue)

-

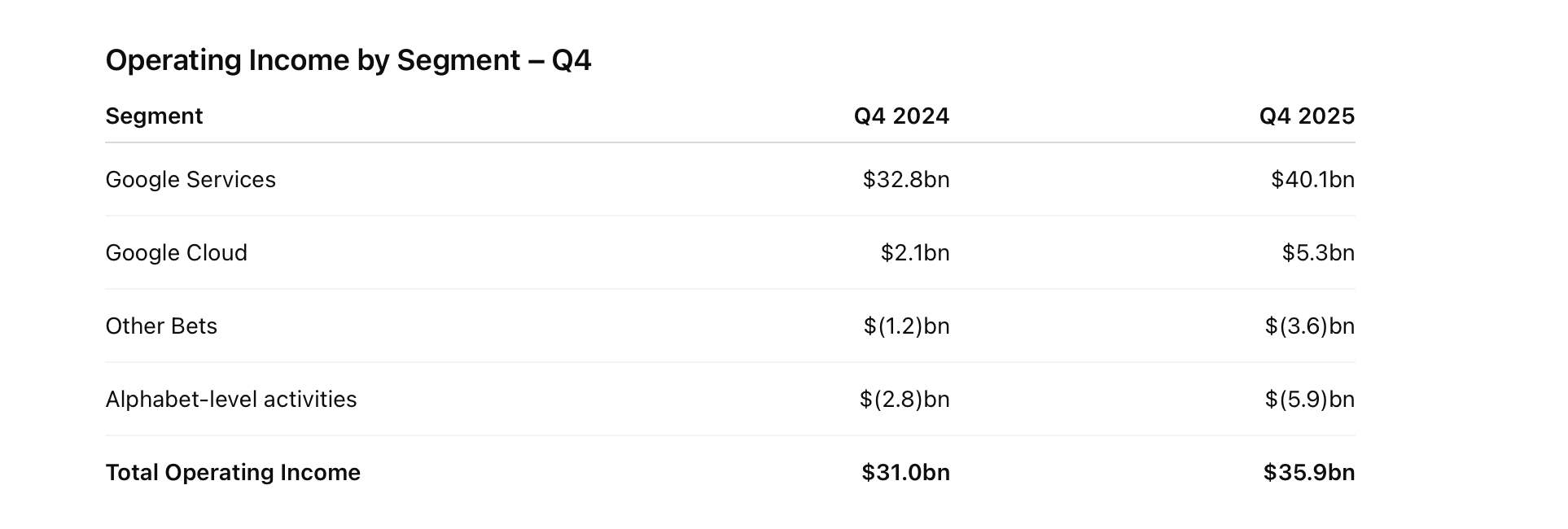

GOOG surpass my earnings 2.83. They didn’t revalue space x. 35 billion net income . Will spend 180b on capex. That’s big. But what we all need to understand, they sold the capacity. Just like msft. It’s an iron clad contractual ‘binding UN resolution’ tropic thunder’ type deal. Good news to reverse the red. Cloud up 48%. More tomorrow but a great result.

-

A brilliant result with +30% earnings from-a company this size can print gains like this. The big take away is tehehuge Capex spending-and where is this money going(who gets most of it?).

I trust the CEOs and Sundar is best placed over Dave on the internet insofar as where's a good place to be investing GOOG cash. Again he said on the call-they are constrained and they are making a lot of money from AI.

What we saw today were the extreme PE stocks, Palantir, APP, AMD get a good kicking and they dragged everything else down with it-and after hours the quality came back hard. And what you find is any stocks that have risen very fast will also fall very fast in these scenarios (Parabolic effect) but quality, as I said comes back. the dross does not!

There is a lot of noise/FUD around capital spending on GPUs etc and I have to say it's more an opportunity than a risk. A lot push/pull going on, media influence and weak hands. As always patience and staying the course.

Chief Financial Officer (CFO)

CapEx guidance (most important takeaway)

2026 capital expenditure expected at $175bn–$185bn, a sharp step-up.

Spend will be heavily front-loaded into:

Data centres

Custom silicon

AI compute and networking infrastructure

Cost discipline & margins

CFO acknowledged CapEx intensity but stressed:

Operating margins remain structurally stable (~32%)

AI infrastructure investments are already driving Cloud profitabilityBalance sheet

Highlighted $24.8bn in net debt issuance in late 2025 as deliberate liquidity positioning ahead of peak investment years.

Dividend maintained at $0.21 per share, signalling confidence despite elevated CapEx.

Bottom Line

Alphabet is spending aggressively, especially on AI infrastructure.

Management is not pretending CapEx will normalise soon — 2026 is a heavy year by design.

The tone from both CEO and CFO was confident, almost blunt:

short-term cash intensity is the price of long-term dominance.

Elevated CapEx

Stable margins

Cloud and AI doing the heavy lifting on incremental returns -

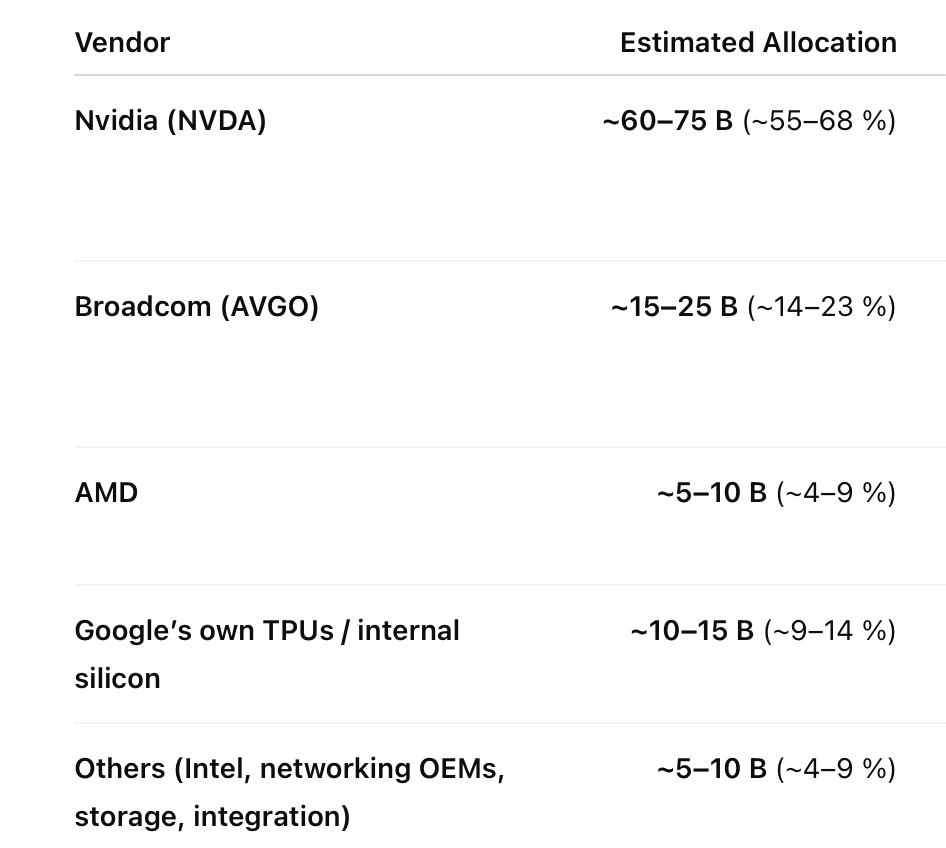

Of the $180B 2026 Capex, $110B will do towards racks scale build out, split roughly 50/50 GooG/GCP. I would estimate the following recipients of this cash pile. The clear winners being NVDA/AVGO