Apple News

-

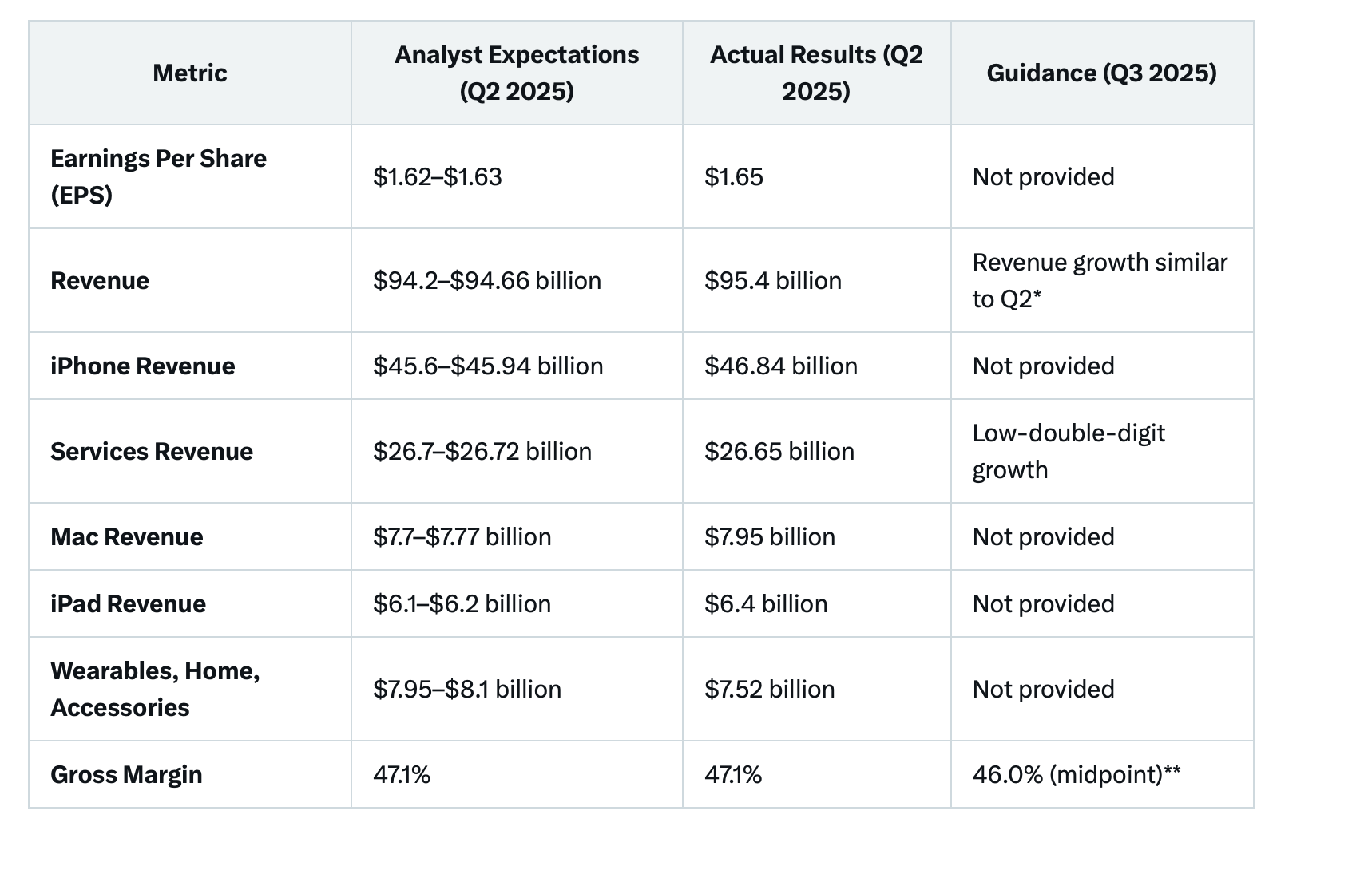

A beat on the top and bottom lines from Apple, delivering a solid quarter

Notes:

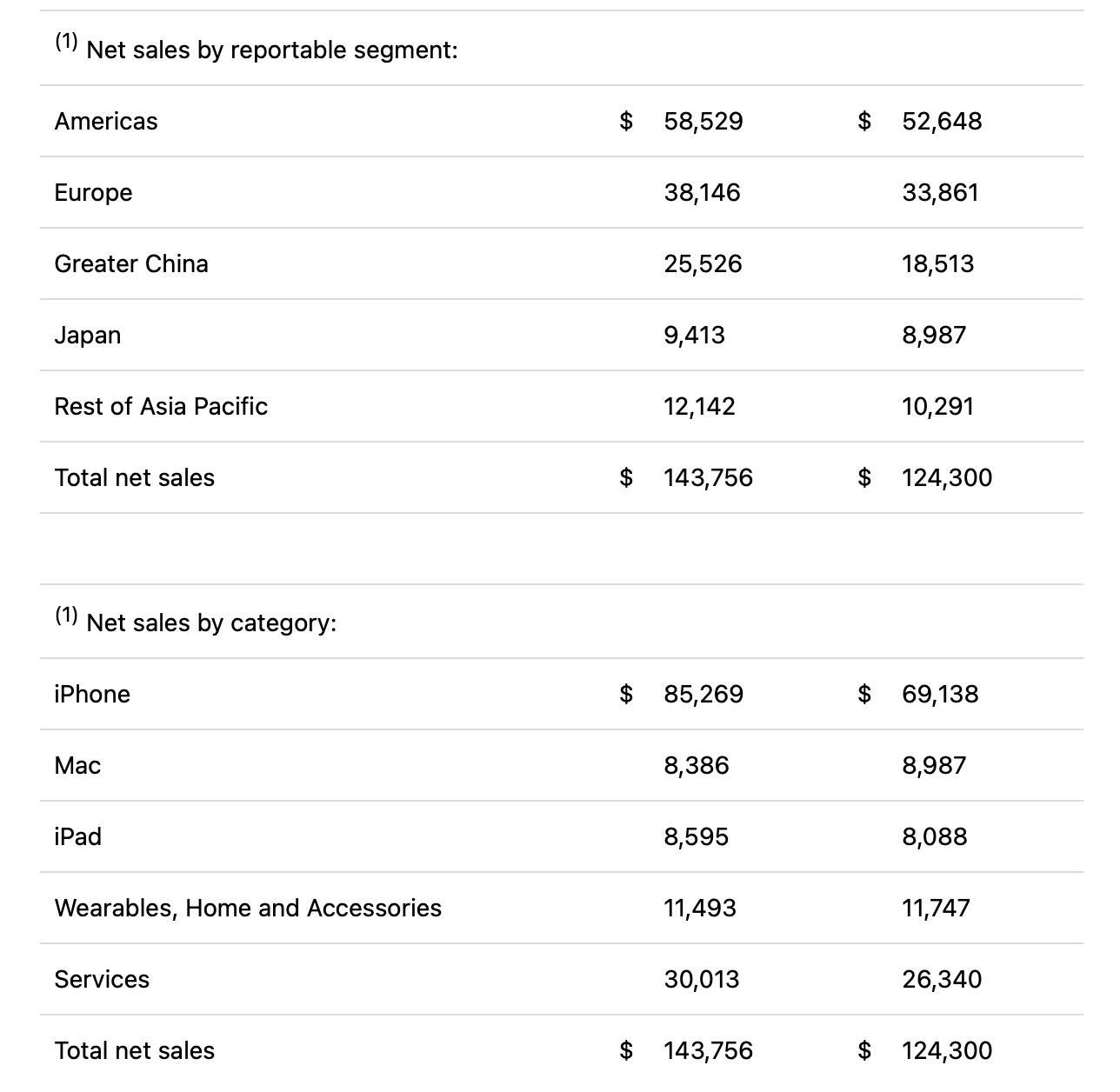

EPS and Revenue: Apple surpassed analyst expectations, reporting an EPS of $1.65 (vs. $1.62–$1.63) and revenue of $95.4 billion (vs. $94.2–$94.66 billion), a 5% year-over-year increase, driven by robust iPhone and hardware sales.iPhone Revenue: Rose 2% to $46.84 billion, exceeding forecasts, despite stable iPhone unit sales, reflecting strong demand for the iPhone 16 series.

Services Revenue: Grew 11.65% to $26.65 billion, slightly below expectations ($26.7 billion), supported by over 1 billion subscriptions across services like the App Store and iCloud.

Mac and iPad Revenue: Mac sales increased 6.6% to $7.95 billion, and iPad sales rose 15% to $6.4 billion, both outperforming estimates, fuelled by new MacBook Air and iPad Air models launched in March.

Wearables, Home, Accessories: Declined 5% to $7.52 billion, missing expectations, due to a challenging comparison with the Vision Pro launch in Q2 2024.

Greater China Revenue: Dropped to $16 billion (vs. $16.8 billion expected), impacted by competition from local brands such as Vivo and Huawei.

Guidance for Q3 2025: Apple anticipates revenue growth “similar to” Q2’s 5% year-over-year growth, despite a 2% foreign exchange headwind. Services revenue is expected to grow in the low-double digits. Gross margin is projected at approximately 46.0% (midpoint), affected by a $900 million tariff cost. Operating expenses are forecasted at $15.6–$15.8 billion, with other income/expense around negative $300 million and a tax rate of about 16%.

AI and CapEx Details from Earnings Call

AI (Apple Intelligence): CEO Tim Cook emphasised Apple Intelligence as a core strategic priority, integrated into iOS 18 and the iPhone 16 lineup. However, delays in generative AI features for Siri, now expected in 2026, raised questions about Apple’s competitive position against Google and Microsoft. Cook highlighted increased research and development (R&D) expenditure, representing 7% of Q2 net sales (approximately $6.7 billion), to advance AI capabilities. Apple Intelligence is set to expand to additional languages in April 2025.CapEx: Apple does not disclose precise CapEx figures. However, Cook noted significant investments in supply chain diversification to counter tariff impacts, including manufacturing iPhones in India for the US market and sourcing other products from Vietnam.

Analysts estimate Apple’s annual CapEx at $10–$12 billion, directed towards AI infrastructure, production facilities, and retail. The $900 million tariff cost projected for Q3 2025 reflects challenges from US tariffs on Chinese imports, prompting Apple to optimise its global supply chain. Cook stated that Apple’s on-device AI approach reduces the need for extensive data centre investments compared to competitors building large-scale AI models.Apple stock in our opinion looks fully priced-not stretched. It is a perhaps the strongest brand in the world and has a credit rating equivalent to government debt, and is trading on a similar basis. Our carrying weight had been trimmed over the past quarters to reflect this.

-

& will never happen.

Trumps latest market manipulation is just dire.

His crazy tariff game enables those in the know to make HUGE gains from the market swings, & shoe-horning crypto fan Atkins in as SEC Chief helps him avoid the glare of investigation (for now).

I am sure things will back up, but it is just appalling how he can get away with stuff. The ambush on Ramaphose with a mixup of totally fake news the other day was awful to watch, like Zelenskyy’s but worse, with the “dim the lights” cr@p. Just reality show nonsense. -

If there is a tariff on phones, Apple will raise global prices to smooth the spikes. It’s not a sustainable model so best to ignore it as yet about pet project of DT. With earnings next week(Nvidia) it’s all eyes elsewhere.

-

Apple is reportedly preparing to initiate development of its first foldable smartphone in the second half of 2025, with contract manufacturing partner Foxconn. I would think, it true, it will spur a super upgrade cycle. I'm keen

")

-

I bet it is mucho bucks. £1,800 maybe, which is ridiculous but it will sell very well. It will look something like this, it's not official (the image)

-

Makes perfect sense given the development costs would surely be 10s of billions- and Apple are late to the party imo

-

Samsung will commence production of OLED screens in Q4, which will be used in Apple's first foldable phone-scheduled for release in H2, 2026. Expect the iPhone foldable to retail for circa £2K!

-

Dan Ives had the following to say in an investors note and raised their PT (price target) to $310 (which hinges on their AI strategy imo. To date it has been none existent :

Entering the iPhone 17 cycle, we anticipated a strong but not exceptional upgrade cycle. However, a significant pent-up consumer demand, with our estimate of 315 million out of 1.5 billion iPhones globally not upgraded in the past four years, combined with notable design enhancements, has driven a robust start, according to Ives and his team.

The analysts suggest that Wall Street’s projection of approximately 230 million iPhone units for fiscal year 2026 may be conservative, with estimates now ranging between 240 million and 250 million units based on current momentum.“Demand in China will be pivotal to the iPhone 17 upgrade cycle, as the negative growth trends of recent years are expected to reverse into positive growth in FY26,” the analysts observed.

Although the iPhone Air faces delays in China due to regulatory approval for its eSIM, the analysts anticipate resolution within the next month, enabling its availability in stores and online. They noted that Apple must intensify efforts to drive growth in China, where domestic competitors like Huawei and Xiaomi present significant challenges.

“The critical issue remains Apple’s understated AI strategy. With a global installed base of 2.4 billion iOS devices and 1.5 billion iPhones, now is the time for Apple to accelerate its AI initiatives through strategic partnerships,” Ives and his team stated.Following the recent victory for Alphabet (GOOG, GOOGL) and Apple in Google’s antitrust case, which restricts “exclusive deals” for search, the analysts believe the groundwork is laid for Apple to maintain its existing agreement.

They expect Apple to deepen its AI collaboration with Google Gemini, integrating it into the iPhone ecosystem (a positive for both).The analysts estimate that AI monetisation could contribute $75 to $100 per share to Apple’s valuation over the coming years.“No ‘AI premium’ is currently reflected in Apple’s stock price, making it an attractive large-cap technology investment heading into year-end and 2026,” they concluded.

I personally think if Apple can offer AI as a service which add utility and they probably will, there will be very wide adoption given their installed base. A true assistant that can navigate across the Apple ecosystem would add considerable value.

-

Apple results-and I have to say they really surprised me. Very strong. Take a moment to think about these numbers.

Just under 144B

$85B just iPhones segment

$30B in services which is almost pure profit

$42B tax paid profit

deep double digit growth and guiding for continued strength

It will take NVDA next Q to beat this sort of earnings with GOOG hot on their heels no doubt.

-

Apple turns 50!

Half a century on, Apple has marked its 50th year — and it’s hard to argue that any other firm has so profoundly reshaped how people live with technology. Not bad for something that began with a couple of university dropouts tinkering away in a suburban garage.

The Apple I was hardly glamorous — essentially just a bare circuit board, with no screen, no keyboard, and certainly no polish. But Steve Jobs and Steve Wozniak were chasing something bigger: a computer ordinary people could actually use, and afford, at home or at work. By 1977, the Apple II arrived — one of the first machines to offer colour graphics and a built-in keyboard straight out of the box. Sales leapt from $7.8 million in 1978 to $117 million just two years later, signalling that something significant was underway.Fast-forward to today, and from the days of the iPod Shuffle to its current line-up, Apple hasn’t really lost its lustre. In fiscal 2025, it pulled in a record $416 billion in revenue — a figure larger than the entire economic output of most countries. Its market value sits around $3.75 trillion, second only to Nvidia (NVDA). Roughly 2.2 billion people — about 27% of the global population — now use Apple devices, giving it an unmatched footprint for a single brand.

The company didn’t let the anniversary pass quietly. Celebrations unfolded worldwide in the lead-up to April 1, with Paul McCartney taking the stage at Apple Park in California for a headline performance.

Chief executive Tim Cook reflected on the journey, pointing to a long line of products and services — from Mac to iPhone, Apple Watch to AirPods, alongside platforms like the App Store and iCloud — all built around the same core idea: putting powerful, intuitive tools into people’s hands.

Not everything has been smooth sailing of late. Apple has faced criticism for appearing cautious in the rush towards artificial intelligence. But that restraint may be deliberate. Its strong stance on user privacy doesn’t sit comfortably with data-hungry AI models, and while rivals pour vast sums into the space, Apple has taken a more measured path.

There’s precedent for that patience paying off. Apple has often entered markets later than competitors, only to refine and dominate them. With its tightly woven ecosystem, it may not need the most advanced AI model — just the smartest way of embedding it across its devices and services.

Even in a crowded smartphone market and a sluggish PC sector, Apple continues to show resilience. iPhone revenue rose 23% in the first quarter of fiscal 2026, and newer releases like the MacBook Neo have drawn in a surge of first-time Mac users. All this against a backdrop of trade tensions, tariffs, and wider global uncertainty.

At 50, Apple feels less like a hardware company and more like a sprawling digital ecosystem — one increasingly shaped by services, software, and intelligent integration. The next chapter may not hinge on a single revolutionary product, but on something subtler: a platform that steadily becomes more useful, more personal, and harder to leave behind.

Cook, characteristically, isn’t dwelling too much on the past. But he did pause to acknowledge the milestone — and the millions of people, from employees to developers to everyday users, who’ve carried Apple from a garage experiment to one of the most influential companies the world has ever seen.

-

Tim Cook resigns as CEO but will stay on as Executive Chairman, effective 1 Sept. No real surprise. Cook is 65 now. I don't think much will change at Apple. Cook has been a fantastic boss and hands over to John Ternus, an Apple veteran with 25 years tenure at the company.

-

Some analysts comments

Apple grabbed attention on Friday after posting better-than-expected results for its fiscal second quarter, with the iPhone 17 range still clearly landing well with customers.

That said, it was the outlook for the next quarter — especially on gross margins — that really caught even the most bullish on Wall Street off guard. In a good way.

Margin worries ease

Morgan Stanley analyst Erik Woodring said Apple’s forecast of 47.5% to 48.5% gross margins for the upcoming quarter — despite “significantly” higher memory costs — came as a nice surprise.

“Revenue and profit strength are holding up, including a standout June quarter margin outlook, which makes us more confident Apple can handle record cost inflation,” he wrote in a note to clients.

He added that the latest results were likely the turning point investors were waiting for, setting the shares up to perform well heading into the September iPhone launch. Woodring kept his Overweight rating and lifted his price target to $330 from $315.For the next quarter, Apple expects total revenue to grow between 14% and 17% year-on-year — well ahead of the 9.3% analysts had pencilled in. Services revenue should come in roughly in line with the March quarter, even after stripping out favourable currency movements.

On rising memory costs, outgoing CEO Tim Cook said on the earnings call that Apple would “look at a range of options” to manage the impact.Product momentum and supply chain edge

While margin concerns seem to have eased for now, J.P. Morgan analyst Samik Chatterjee pointed out that Apple’s product momentum is pretty exceptional at the moment.

“Despite investor concerns, the bigger challenge for Apple looks to be on the supply side — particularly getting hold of advanced processors needed to keep up with stronger-than-expected iPhone demand, and increasingly for Macs too,” he said.

He noted a recent spike in demand for the Mac mini, Mac Studio, and the newly launched MacBook Neo.

Chatterjee also said the upbeat guidance suggests Apple is gaining market share across its product lines, thanks to strong customer demand and better supply chain management — especially when it comes to memory — compared with rivals.

He raised his revenue forecasts, stuck with an Overweight rating, and kept a $325 price target.

Citi analyst Atif Malik said so-called “agentic” AI is boosting demand for Macs, putting Apple in a solid position to benefit from the AI wave. During the earnings call, Apple highlighted strong demand for the Mac mini and Mac Studio tied to AI use cases, while MacBook demand has been “off the charts”.

Given Apple’s sheer scale and buying power, Wells Fargo analyst Aaron Rakers said that’s turning into a real competitive advantage — particularly versus other PC makers.

“We see Apple’s economies of scale as a major plus in the current environment,” he said, pointing to a big jump in long-term purchase commitments, which could signal major supply agreements, including for memory. -

Anyone else go to buy an Apple product in the last couple of days? iPad Pro 13 was £1,199. Now £1,499. ouch. Cheekie rascals

-

Micron told Apple to wind their neck in as Apples tactics caused the under investment years ago. The actual increase for that kind of memory is less than $50-im not complaining just pointing out the disproportionate increase. Im Deep into the Apple ecosystem so no avoiding it

-

yep!

and this will be what, £20K?

")